Journal of Financial Planning: January 2023

Bradley T. Klontz, Psy.D., CFP®, is an associate professor of practice at Creighton University Heider College of Business and a managing principal at Your Mental Wealth Advisors. He has written eight books on the psychology of money, including Psychology of Financial Planning: The Practitioner’s Guide to Money and Behavior.

NOTE: Please click the images below for PDF versions.

JOIN THE DISCUSSION: Discuss this article with fellow FPA Members through FPA's Knowledge Circles.

FEEDBACK: If you have any questions or comments on this article, please contact the editor HERE.

This is an exciting time for the financial planning profession. Everywhere you look you’ll see the profession embracing the psychology of financial planning. In all fairness it may be more accurate to say that everywhere I look that’s what I see. I may be a bit biased though. In fact, I probably suffer from a confirmation bias in this area, where I seek out information to support my belief that the profession is excited about the psychology of financial planning, and I discount or explain away information that might disconfirm or challenge my belief. To be completely honest, I’m probably vulnerable to a sunk cost fallacy in this area too, given how much time and energy I have invested in the area.

You see, for the past 20 years I have dedicated much of my professional life to exploring the connection between psychology and financial planning. This has included studying the relationship between someone’s financial psychology and their financial outcomes including their income, net worth, and their ability to reach their financial goals. My efforts have also included adapting techniques from the field of psychology to help improve the financial health of clients, increase their savings rates or their 401(k) salary deferrals, increase their motivation to achieve their financial goals, and improve their overall life satisfaction. In addition to attempting to better understand the link between psychology and money, I have also worked to equip financial planners with psychology theory and tools to help them better serve their clients. This has included helping advisers better establish rapport with clients, increase client motivation to make changes, and adopt techniques to help clients overcome their resistance to change.

Despite my biases and for reasons discussed below, the psychology of financial planning appears to be a hot topic in the field, and it makes sense why advisers are interested. It doesn’t take long in practice for a financial planner to notice the behavioral aspects of the profession. There often seems to be a disconnect between what is good for a client’s financial health and what they do. Some common behavioral challenges that financial planners encounter with clients include: (a) watching clients engage in financial behaviors that are not in their best interest; (b) clients not following through on their financial plans; (c) clients resisting even the best advice; (d) financial disagreements between couples and family members; (e) clients making terrible investment decisions, such as refusing to diversify from a concentrated position or falling prey to exuberance or fear; (f) clients asking for help in navigating emotionally charged and challenging financial situations (e.g., divorce, diminished capacity, or death of a loved one); (g) clients financially enabling adult children or others to everyone’s detriment; (h) clients struggling to adjust to a major life transition such as an inheritance or retirement; and (i) noticing that a client’s upbringing, background, and beliefs about money are sabotaging their ability to meet their financial goals. The psychological aspects of financial planning are many, and financial planners deal with them daily with their clients. In fact, I have heard from more than one planner that they often feel like they spend more time playing the role of a therapist than they do giving financial advice.

The fact is that money intersects many areas of our lives, and often our challenges go beyond the nuts and bolts of financial planning and the traditional knowledge base and skill set of financial planners. Over the years I have also noticed that some of the most effective financial planners are those who approach their relationships with clients from a holistic perspective. Instead of focusing on just the technical aspects of financial planning, they are concerned about their clients’ values, relationships, and overall quality of life. They go beyond just giving advice and play an important role in their clients’ lives. They are good listeners; create a safe environment for clients to talk about their successes, worries, and failures; help clients challenge limited thinking; help clients navigate financially stressful personal and familial challenges; and help clients overcome self-destructive financial behaviors. Whether by accident or design, these financial planners have developed a skill set that goes beyond what has traditionally been taught in the financial planning educational curriculum. While they are not therapists, they tend to have a deep understanding of their clients’ motivations and are able to help clients navigate a variety of issues that go beyond traditional financial advice.

Recently the financial planning profession has formalized the importance of this type of knowledge base and skill set in financial planning. No longer are such holistically oriented, psychologically informed financial planners the exception. Thanks in large part to recent initiatives by the CFP Board, a psychologically informed approach to financial planning will soon be the rule.

A New Paradigm

Traditionally, financial planners seeking to become CFP® professionals have been required to receive education and demonstrate proficiency in traditional financial planning knowledge topics such as investment planning, estate planning, risk management and insurance planning, educational planning, retirement planning, tax planning, and professional ethics. But in 2021 a new topic was added to the CFP® exam curriculum. Based on the CFP Board’s 2021 Practice Analysis Study (CFP Board 2022), which included a large-scale survey asking CFP® professional educators and practitioners what is important to them in their work with clients, a new knowledge topic was added: the psychology of financial planning.

As identified by the CFP Board, this knowledge topic includes the following broad categories: (a) client and planner attitudes, values, biases; (b) behavioral finance; (c) sources of money conflict; (d) principles of counseling; (e) general principals of effective communication; and (f) crisis events with severe consequences. In other words, in 2021 the CFP Board formalized what many skilled advisers have known for years—that an understanding of a client’s financial psychology is key to being an effective financial planner.

Behavioral Finance

While the inclusion of psychology as a fundamental knowledge area for financial planning is new, the application of one branch of psychology to financial planning has been integrated into the profession for some time now: behavioral finance. While this has been identified in the past as the application of psychology to finance, a closer look at the field of behavioral finance reveals that it is better described as the application of just one area of psychology to financial planning: cognitive psychology (Klontz, Kahler, and Klontz 2016). According to the American Psychological Association, cognitive psychology is a branch of psychology that studies “mental processes related to perceiving, attending, thinking, language, and memory, mainly through inferences from behavior.” Cognitive psychology is the study of how human beings are naturally wired to interact with the world. As such, research in behavioral finance has focused on common cognitive biases to help us explain and predict, for example, common investing mistakes. Behavioral finance focuses on the study of universal human tendencies, biases, and heuristics. Some classic examples of behavioral finance’s contributions to our understanding of investor behavior include biases such as confirmation bias and sunk cost fallacy I admitted falling prey to at the beginning of this article, as well as our tendency to treat money differently based on our associations with it (e.g., mental accounting), our tendency to seek pride by selling winning stocks and avoid pain by holding on to losing stocks (e.g., the disposition effect), and our tendency to avoid taking action even when doing so might be in our best interests (e.g., status quo bias).

The field of behavioral finance has helped us understand and describe what appears to be a universal human tendency to make bad financial decisions. It helps normalize our instincts around investment decisions, many of which appear to go against our long-term benefit. It also helps us mitigate the damage done by these biases, primarily through instituting macroeconomic interventions, such as harnessing the status quo bias by encouraging automation and requiring people to opt out of participating in their 401(k)s versus requiring them to opt in. But behavioral finance is just part of the story. While it does a great job of identifying universal cognitive biases, it ignores an individual’s specific experiences, family patterns, relationships, and idiosyncratic beliefs and behaviors (Klontz, Chaffin, and Klontz 2023).

Much of the research in behavioral finance has been conducted by economists and finance professors, not financial planners who meet with actual clients. This is one factor that has contributed to the ongoing disconnect between research and practice (Klontz and Horwitz 2017). Aside from helping us understand common investing pitfalls, behavioral finance offers little in terms of equipping financial planners with the tools they need to help understand their clients’ unique financial psychology, let alone how to apply this knowledge to help shift a client’s beliefs or behaviors.

To illustrate the disconnect between a helpful theory and being helpful with a client, I will often give my financial planning and financial psychology students at Creighton University a thought experiment to help illustrate how useless a knowledge of cognitive biases can be in a conversation with someone who may be exhibiting one. I ask them to close their eyes and imagine a scenario in which their significant other is unfairly complaining about them. Their task is to simply help their partner by pointing out the the cognitive bias their partner is displaying. For example, imagine that your partner is passionately lodging a complaint about a minor mistake you made today. Clearly, they are overreacting, and you help them by explaining to them that they are suffering from a recency bias because they are ignoring all the good things you have done in the past and are giving too much weight to the mistake you made today. My students inevitably laugh at how ludicrous such an intervention is, which is likely to be both ineffective and insulting. The same is true for a client who is exhibiting a cognitive bias around investing. Not only is pointing out such a bias in real time likely to not be helpful, but it’s also very likely to damage the relationship and decrease the chances that the planner will be able to exert a positive influence on the client’s behavior. While we can utilize an understanding of cognitive biases to encourage clients to institute good financial habits, such as harnessing the status quo bias by encouraging automation, a much more comprehensive understanding of all that psychology has to offer is important if we want to truly understand and help them.

The Psychology of Financial Planning

While behavioral finance helps us make sense of human cognition and biases and how they impact financial behaviors, the broader field of financial psychology integrates other bodies of knowledge to help financial planners understand their clients’ unique psychology around money and equip them with tools to help clients improve their financial health. This comprehensive approach integrates other fields of psychology, including but not limited to: multicultural psychology, developmental psychology, evolutionary psychology, social psychology, personality psychology, behavioral psychology, marriage and family psychology, and neuropsychology (Klontz, Chaffin, and Klontz 2023), as well as conflict resolution, communication techniques, counseling techniques, and crisis intervention. In other words, the psychology of financial planning covers much more than just cognitive psychology. It seeks to understand a client’s entire psychology of money including their upbringing, past experiences, learning style, psychological risk profile, money beliefs, financial behaviors, cultural identity, values, motivation, relationship and family dynamics around money, sources of intrapersonal and interpersonal conflicts around money, and more. Perhaps most importantly, it seeks to equip financial planners with the knowledge and tools they need to help their clients reach their financial potential, encourage them to take action when they are stuck, and help them successfully navigate their personal and interpersonal financial challenges.

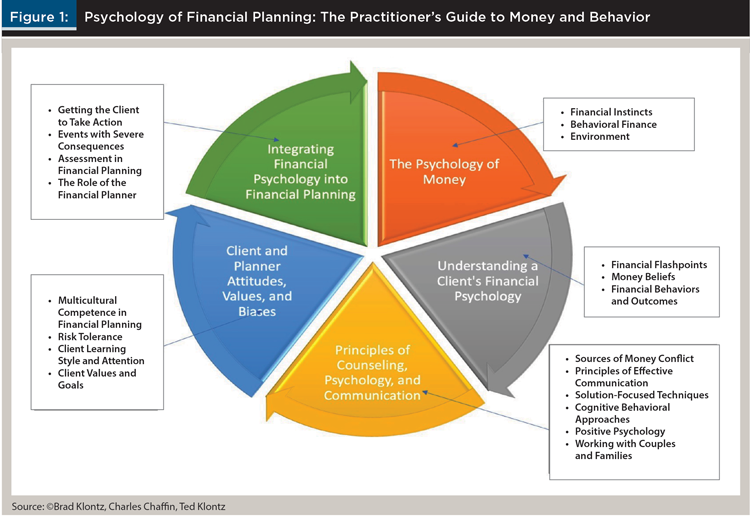

The psychology of financial planning attempts to take a comprehensive look at the behavioral aspects of financial planning and equip financial planners with the tools they need to maximize their effectiveness. In Klontz, Chaffin, and Klontz (2023), behavioral finance represents just one of 20 areas of financial psychology that are important to understand when working with clients, as illustrated in Figure 1.

Conclusion

The integration of the psychology of financial planning into the financial planning knowledge base offers an opportunity to better understand and serve clients. A financial planner’s work is much more than just giving a client financial advice and managing a client’s investments. Financial planners are uniquely positioned to help clients with what has been consistently identified as one of the top sources of stress in the lives of Americans—money (American Psychological Association 2022). Embracing the psychological aspects of financial planning will help a financial planner acquire, service, and retain clients, but can do so much more. The psychology of financial planning will equip our profession with the theory and tools we need to help clients reach their financial goals, improve their relationships, increase their financial and life satisfaction, and help improve the financial health of society at large.

References

American Psychological Association. s.v. “Cognitive Psychology.” https://dictionary.apa.org/cognitive-psychology.

American Psychological Association. 2022. “Stress in America 2022: Concerned for the Future, Beset by Inflation.” www.apa.org/news/press/releases/stress/2022/concerned-future-inflation.

CFP Board. n.d. “2021 Practice Analysis.” www.cfp.net/get-certified/certification-process/2021-practice-analysis.

Klontz, B., C. Chaffin, and T. Klontz. 2023. Psychology of Financial Planning: The Practitioner’s Guide to Money and Behavior. John Wiley & Sons: Hoboken, NJ.

Klontz, B., R. Kahler, and T. Klontz. 2016. Facilitating Financial Health: Tools for Financial Planners, Coaches, and Therapist. The National Underwriter Company: Erlanger, KY.

Klontz B. T., and E. J. Horwitz. 2017. “Behavioral Finance 2.0: Financial Psychology.” Journal of Financial Planning 30 (5): 28–29.