Journal of Financial Planning: September 2025

NOTE: Please be aware that the audio version, created with Amazon Polly, may contain mispronunciations.

Christine M. Luken, the Financial Dignity Coach, is a Certified Divorce Specialist and a Certified Financial Counselor with almost two decades of coaching experience. She is the author of Financial Dignity After Divorce and the host of the Money is Emotional podcast. Connect with her at www.christineluken.com.

NOTE: Click on the image below for a PDF version.

Understanding the Emotional Landscape of Divorce

Money is emotional because we’re human, and humans are emotional creatures. While we might try to compartmentalize financial decisions as simple math problems, the truth is far messier. When left unexamined, emotions can create financial chaos, particularly during the divorce process. This is why it’s vital for us as financial professionals not to gloss over or dismiss the importance of emotions in money decisions with our divorcing clients. It’s too easy to say, “Just make the logical money decision! If you want to change your financial results, you need to change your actions.”

It’s true that if your clients take better financial actions, they’ll get better results. But there’s a big piece missing in this equation: emotion. Emotion is the trigger for the actions we take. People usually take action for one of two reasons: to increase pleasure (positive emotions) or to decrease pain (negative emotions). Emotions (both positive and negative ones) are a reaction to what is going on around us and inside of us. If your client is angry, it’s because either someone said something they don’t like or they’re thinking about an upsetting situation, like their soon-to-be ex cheating on them. This emotional cascade becomes especially important to recognize when you’re working with divorcing clients. As a financial planner, your role isn’t just to run the numbers, it’s to understand the emotional undercurrents influencing your client’s decisions. Ignoring those emotions isn’t just unwise, it’s counterproductive.

Why Emotions Can’t Be Left at the Door

The advice to “leave emotions out of money decisions” is both outdated and biologically impossible. Neuroscientist Antonio Damasio discovered that humans literally cannot make decisions without engaging the emotional part of the brain (Hardcastle-Geddes 2018). Clients who have suffered strokes in that region might be able to list the pros and cons of a situation, but they can’t make a final choice, not even about what to eat for lunch. Damasio discovered that decision-making occurs in the same part of the brain that processes emotion.

Understanding this gives you an advantage as a financial planner. It allows you to meet your clients with empathy rather than frustration when their behavior seems illogical. What you’re seeing is the result of unprocessed emotions that haven’t yet been acknowledged, let alone healed. The problem is that we can’t often see the emotions or the root cause of them. We simply see the results of emotional money decisions in their bank accounts.

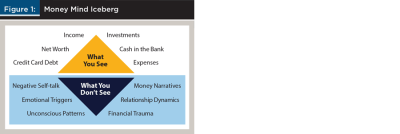

The Iceberg and the Unconscious Mind

Think of the mind like an iceberg when it comes to finances. The unconscious mind, which drives 90 percent to 95 percent of our daily decisions, lies beneath the surface of our awareness. The conscious money mind (the part your client is aware of) is just the tip. It includes things like their income, net worth, credit card debt, and investments. But the unconscious mind is what lies beneath the surface: your clients’ negative self-talk, emotional triggers, relationship dynamics, money narratives, and possibly even financial trauma.

When we were born, we had zero opinions about money, positive or negative. We all began with a blank slate. As each of us progressed through childhood and adulthood, we collected and processed information about money, storing it in our unconscious minds. We gave it meaning based on our experiences. This is true for me, you, and all our clients.

One of the most potent metaphors to share with your clients is the concept of a money blueprint, from T. Harv Eker’s book, Secrets of the Millionaire Mind. Everyone has a money blueprint, shaped by childhood experiences and past relationships. If your client is trying to build a new financial life with an old, dysfunctional blueprint, they’ll struggle no matter how logical the plan appears.

Once the blueprint is revealed and fixed, the outside actions and results come so much easier and faster than you would ever imagine. Money becomes entangled with various types of emotional baggage as we navigate life’s complexities. It’s time to start paying attention to the meaning we’ve given money, good or bad, so we can begin to untangle it.

Helping your client examine and, if necessary, revise that blueprint is just as important as setting up a new budget or asset allocation as they move through divorce. You’re not just guiding them toward better money habits; you’re supporting the creation of a new, empowered identity.

As trusted guides, we can help clients “lower the waterline” to understand what truly drives their financial behavior. Awareness is the first step in defusing strong emotions. The good news is that it’s possible to harness the power of emotions to achieve financial goals, rather than wrestling against them. The one thing we don’t want our clients to do is repress their emotions. If they do, emotions can spring out at inopportune times, causing money chaos in the process. It’s essential to help clients find productive outlets for their emotions. It begins with being aware of common emotional patterns and pitfalls that frequently arise during the divorce process.

Three Emotional Pitfalls and How to Support Clients Through Them

1. Using Money as a Weapon (The Fight Response)

Anger is a natural stage of grief, and divorce is a grieving process. Unfortunately, that anger can sometimes get tangled with financial decisions. Clients might want to punish their ex by spending extravagantly or sabotaging joint finances. It’s the fight response to stress. If your client is tempted to do this, remind them that anger is a two-edged sword that cuts both ways.

Almost a decade ago, I chatted with a frustrated financial planner who unsuccessfully attempted to talk his client down from the ledge regarding her money decisions. As part of her divorce settlement, this woman received half of her husband’s 401(k) funds. She reasoned that because he cheated on her with her best friend, she deserved to spend $50,000 of “his retirement money” on a red convertible. Every time she drove her “revenge car” to his house to pick up or drop off their kids, it would be a rub in his face. Her financial planner pleaded with her not to withdraw $50,000 from the 401(k) to buy the convertible, but his client, in her anger, wouldn’t listen. By cashing out part of the 401(k) money, she owed taxes and penalties, to the tune of 40 percent, a $20,000 tax bill! This means the car cost her $70,000! The withdrawal also meant she had substantially less money for her retirement. A quick run through an investment calculator showed her that the $50,000 invested at 8 percent over 20 years would be worth $233,000 at retirement. Of course, this woman’s anger is justified, but there are better ways to soothe the emotion that are far less costly.

How can you help your client diffuse the emotion of anger? First, don’t shame the client. This immediately shuts them down, and it will be hard for them to receive your advice. Second, normalize their feelings and offer productive alternatives. It’s not helpful to repress anger or deny it. Emotion is energy in motion, and the best solution is to give that angry energy a positive outlet. Offer suggestions such as talking to a therapist or engaging in a physically demanding form of exercise, like kickboxing, running, weight training, or CrossFit. Encourage them to spend a reasonable amount of money on themselves as a reward for making it through the divorce! Rather than buying a $50,000 convertible, maybe my friend’s client could’ve spent $5,000 on a designer handbag or a yoga retreat in Bali. She would’ve had a sense of satisfaction without significant financial damage. Give your client permission to be angry at their cheating ex, but let it out in a way that doesn’t hurt anyone. Encourage them to take 24 hours to calm down before making any financial decision that’s not easily reversed. No one wins when money is used as a weapon, even if your client is the one wielding it. Revenge clouds their judgment, poisons their emotions, and taints their relationship with money. Remind them that their long-term success with money is truly the best “revenge.”

2. Giving Away the Store (The Flight Response)

Some clients simply want the divorce to be over with. They don’t want to argue. They don’t like drama. They want out. But in their desire to escape, they may relinquish assets or responsibilities that will hurt them later. This is the flight response to stress.

Twenty-five years ago, I left a seven-year relationship with my ex-fiancé, Jeff, and I gave away nearly everything, including my pets and furniture, because I was too emotionally exhausted to fight. In doing so, I ended up costing myself money. If Jeff said he wanted something, I just let him have it. I only took a few things from our apartment besides my clothes, books, and jewelry. All of the debt we accumulated during the relationship was in my name. I didn’t even try to get him to take responsibility for any of it. I also let my ex keep a car that was titled in my name, even though I was legally and financially responsible for it. It seemed mean to take “his car,” and I wasn’t mean, even in the midst of my breakup.

Maybe your client has weak financial boundaries (as I once did) and wants to avoid conflict, even healthy confrontation, at all costs. But there are things worth taking a stand for during their divorce. Women, especially, can struggle with this. As a society, women have been conditioned to cooperate, to get along, to be agreeable. “I wish I’d seen more role models in my culture handle money in an empowered way,” says Cindy Alisha Gunraj, a divorce coach. “Most of the time, men controlled the finances, and women were left out of the money discussions. Men used it as a form of dominance and control. I remember my own mother telling me, ‘Don’t take too much,’ in my own divorce settlement!”

Fortunately, this dynamic is beginning to change, and we should encourage our clients, regardless of gender, to maintain healthy boundaries in relationships. Our clients need to be respectfully assertive to receive their fair share of both the money and personal belongings. Remind clients that divorce agreements can be complex and challenging to revise later, so it’s essential to get what they deserve the first time around. We can be vital advocates for our clients, alongside their divorce attorney.

What’s the best response for someone who wants to flee the marriage and give up assets or income they’ll regret later? Help clients recognize the long-term cost of short-term relief. Run the numbers so they can see in black and white what they’re forfeiting. Encourage them to establish healthy boundaries and be assertive. If they struggle with advocating for themselves, invite them to consider a higher cause, such as their children or charitable giving, as a way to anchor their decisions in purpose rather than avoiding discomfort. Even the kindest, gentlest woman turns into a grizzly momma bear if you mess with her kids. Every dollar she doesn’t get is money she can’t spend on taking care of her kids. What if your client doesn’t have kids? Identify their higher cause, which might be the local homeless shelter or the ASPCA. If your client ends up struggling financially because they haven’t stood up for themselves during divorce, that’s less money they have to donate to their favorite charity.

3. Deer in the Headlights (The Freeze Response)

You’re driving down a country road, rounding a curve, and your headlights land on a deer. It’s standing in the middle of the road, staring straight at you. Your adrenaline spikes as you slam on your brakes and the horn simultaneously. After a long second, the deer finally bolts out of the way, narrowly missing your car. Is your client reacting to the process of divorce like a deer in the headlights? Frozen in fear, afraid to move? This happens when your client feels paralyzed and unable to take productive action. This is known as the freeze response to stress and can be worse than fight (using money as a weapon) or flight (giving away the store). Most clients who experience the freeze response did not initiate the divorce, and might be in a state of shock or denial. But refusing to make decisions is a decision. Delaying action can force your client into an unfavorable course of action by default.

Interestingly, the “deer in the headlights” response has two potential causes: overwhelm and confusion. The problem is that both can manifest as fear. Holistic divorce coach Olga Nadal says, “Combining fear and money makes the divorce process longer and more painful!” How can you tell which one your client is experiencing? Ask them this question: “If I give you more information and direction, will that feel helpful or overwhelming?”

If more information will help your client move forward in the divorce process, then they’re probably confused about the right action to take. If more information feels like it would make the problem worse, they’re experiencing overwhelm. If confusion is the cause of your client’s inaction, determine exactly what they need to know and point them to the right source of information or expert to help them. Remind your client not to feel ashamed or embarrassed to reach out to you with their questions.

If your client is overwhelmed, give them baby steps. A mile-long financial to-do list can stress them out and cause them to procrastinate. Give them one or two tasks at a time. If your client hasn’t managed their own personal finances before the divorce, they might benefit from hiring a financial coach or even a daily money manager to hold their hand through this transition. If their overwhelm is growing into larger issues like anxiety or panic attacks, refer them to a mental health professional. You are not expected to carry your client’s emotional weight alone, nor should you.

What Financial Dignity During Divorce Looks Like in Practice

Financial dignity is the integration of wise money management and emotional intelligence. It’s about helping clients make decisions that serve their future without sacrificing their humanity. It’s a calm, centered approach to planning that respects both the numbers and the nerves.

Here’s what it looks like in practice:

- You validate the client’s emotional experience without judgment.

- You offer structure and logic as tools for empowerment, not control.

- You provide suggestions for healthy and constructive emotional processing.

- You model calm, confident leadership so your client can anchor to your steadiness.

- You collaborate with therapists, coaches, and attorneys to create a holistic support team.

As financial professionals, we are being called into a new paradigm, one where emotional intelligence is just as valuable as financial advice. In the chaos of divorce, your client doesn’t just need graphs and spreadsheets; they need a safe harbor. They need someone who can hold space for their pain without getting swept into it, and who can help them chart a steady course toward a new beginning.

Financial dignity is not a luxury. It’s a necessity. Let’s lead the profession forward, one empowered client at a time.

Reference

Hardcastle-Geddes, Kimberly. 2018, November 6. “When It Come to Decision-Making, Logic Isn’t the Most Powerful Motivator.” PCMA. www.pcma.org/come-decision-making-logic-isnt-powerful-motivator/.