Journal of Financial Planning: June 2015

The Next Generation of Asset Allocation

ETF managed portfolios exploded in popularity in recent years, boasting more than $90 billion of assets at the end of 2014. The category, as defined by Morningstar, includes nearly 700 strategies managed by 150 ETF strategist firms. Morningstar divides the ETF managed portfolio universe into three distinct sub-categories based on investment approach: strategic asset allocators that establish a long-term asset allocation and allow for limited deviation from that asset allocation; tactical asset allocators that rotate asset classes more frequently and to a larger degree; and hybrid asset allocators that combine strategic and tactical elements.

Tactical Asset Allocators

The focus of this article is on tactical asset allocators, as they have had the most success gathering assets but have also had some high-profile cautionary tales. The leading tactical asset allocators market a compelling but controversial value proposition, offering the potential for upside participation while protecting against downside risk, undeniably tempting for advisers and retail investors scarred by two brutal bear markets since 2000.

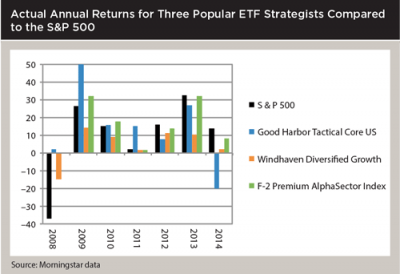

The three market leaders at the beginning of 2014 each faced challenges during the year. F-Squared Investments experienced the largest fall from grace in the aftermath of SEC sanctions and the departure of its embattled CEO. F-Squared saw its assets decline by more than $3 billion in the fourth quarter of 2014, and recently cut 25 percent of its staff. Schwab’s Windhaven Investments continues to be a major success story, though it also lost assets in the second half of 2014 after the departure of founder Steve Cucchiaro. Good Harbor Financial also faced challenges, with its flagship product delivering a return of negative 20 percent the year in which the S&P 500 was up nearly 14 percent.

Despite the challenges faced by the market leaders, a growing roster of innovative firms provide ETF managed portfolios that meet a wide range of investor needs. ETF strategists, like robo-advisers, are drawing some of the brightest financial and quantitative minds to their efforts and offering a compelling career alternative to professionals who previously would be drawn to traditional jobs with large asset managers and hedge funds.

Quantitative techniques are at the core of the investment process for most tactical asset allocators, driving decisions to rotate between different investments, and in many cases, into or out of the market. As is so often the case, the most successful firms have gathered assets by delivering strong returns during a critical period for the markets. Windhaven delivered outstanding relative returns by preserving capital in the aftermath of the tech bubble in 2002, as well as during the heart of the financial crisis in 2008. Good Harbor also made its reputation in weathering the market downturn, providing significant outperformance in 2008, then calling the market turnaround correctly in 2009. F-Squared has a slightly different story, demonstrating strong simulated performance in marketing materials before making major changes in response to the SEC investigation and subsequent sanctions.

Selecting an ETF Strategist

We encourage advisers to go beyond flashy short-term performance results when thinking about investing with an ETF strategist that offers a tactical asset allocation strategy. Critical questions should be asked before investing:

- What role will the strategy play in your client’s portfolio? Will it be used for return enhancement, diversification, or risk management? Some advisers use tactical asset allocators to supplement a core portfolio, while others use them as a core holding. Having a clear purpose simplifies the decision-making process and informs the evaluation process post-purchase.

- What is the strategist’s investment “edge” and is that edge sustainable? The most successful ETF strategists make extensive use of quantitative metrics, leveraging technology in their investment process. Windhaven’s approach relies on a proprietary model of key economic, fundamental, and behavioral relationships; Good Harbor focuses on momentum, economic data, and yield curve analysis; and F-Squared has a sector-centric focus driven by volatility and trends in total returns. The strategist should be able to articulate their advantage and explain why that advantage is sustainable over time.

- How does the firm use the technical inputs? Does the strategist follow the model inputs without intervention, or is there a judgmental overlay applied by an individual or committee? If there is a judgmental overlay, under what circumstances does judgment apply and how successful has the judgmental component of the process been relative to the quantitative component?

- How is the strategy implemented? What investment instruments are used, and how much does the portfolio change over time? For example, can the portfolio go from being fully invested to all cash, or are moves more measured in approach? Portfolio turnover is also an important strategy question, particularly for taxable investors. One of the strategies we examined had turnover of more than 400 percent, potentially an unpleasant surprise for the taxable investor.

- How did the strategist perform in different market environments? Looking beyond three- or five-year performance numbers is a must. Some asset allocators built their track record on the basis of one or two great years of performance around the financial crisis, but have delivered less inspiring returns since (see the bar graph above). Also, size is often the enemy of investment performance, and many stellar track records were built on a small asset base. We think that it’s tougher to sustain success when assets under management grow rapidly. We also caution advisers about the use of simulated, back-tested performance results. Although back-tested results can provide useful insight into how a strategy will work over long periods of time, there is a big difference between simulated and actual results.

Closing Thoughts

History is filled with investors who became famous on the basis of one or two high-profile market calls that went right. Far fewer investors have been able to sustain that kind of success over a long period of time. Michael Mauboussin, in his book The Success Equation, discusses the role of luck in success. Mauboussin cites the tendency of people to derive more meaning from small samples than is warranted by the data. Assuming that a manager who performed well during the last financial crisis will also perform well during the next crisis may not be justified by the data. Investors expecting asset allocators to anticipate all market downturns may have been disappointed during last year’s “taper tantrum,” as most of the leading strategies followed the market downward during that brief but painful correction. So it’s important to do the homework to distinguish whether a tactical asset allocator is a one-hit wonder or has the right stuff necessary to sustain success over time.

As Mauboussin also points out, the markets are a marvelously adaptive environment with market participants adjusting their behavior in response to market activity and other trends. The adaptive environment can include traders that try to trade ahead in anticipation of repositioning by large asset allocators, or “copycats” who crowd into positions held by the large asset allocators.

The “quant quake” of 2007 illustrated how too much of a good thing can end up being a bad thing. Many bright quantitative investors used similar models drawing upon similar investment factors to crowd into many of the same stocks. When the models indicated that it might be time to sell, the resulting deluge of selling reversed several years of excellent performance by quantitatively oriented strategies. So even the best of asset allocators may have their advantage eroded by such adaptive markets.

Daniel Kern, CFA, is president and CIO of Advisor Partners. He is the former managing director and portfolio manager for Charles Schwab Investment Management. He managed asset allocation funds, including target funds, from October 2008 to July 2011.