Journal of Financial Planning: August 2020

Samantha Brady is a research specialist at the MIT AgeLab. Julie Miller, Ph.D. is a research scientist at the MIT AgeLab, and Alexa Balmuth is a technical associate at the MIT AgeLab.

*With additional authors: Adam Felts, Lucas Yoquinto, Lisa A. D’Ambrosio Ph.D., and Joseph F. Coughlin Ph.D., all from MIT AgeLab.

JOIN THE DISCUSSION: Discuss this article with fellow FPA Members through FPA's Knowledge Circles.

The impacts of the COVID-19 crisis are vast, touching multiple areas of people’s lives and finances. During volatile times, it is especially important for financial advisers to actively maintain their client relationships.

While the COVID-19 pandemic is truly unprecedented, there may be lessons from a recent period of volatility, the financial crisis of 2007–2009, that the financial industry can apply to the current situation. During the upheaval of the crisis, many advisers were able to demonstrate their value and retain clients even as they lost wealth as a result of the downturn.1 Some advisers even grew their practices, as people turned to them as trusted authorities to rebuild their wealth and navigate an uncertain period.2

The value of building trust with clients—focusing on the qualitative value of advice in addition to the quantitative—may be especially important for relationships with older clients. Older clients who personally trust their advisers may be more likely to retain their services through stressful life events.3

Right now, people of all ages are looking for trusted sources of advice to help figure out how to navigate the financial upheaval of the pandemic while still working toward their longer-term plans and goals. But even for advisers who recognize the need to demonstrate availability to clients and receptivity to their needs and worries, knowing how and when to reach out in a time of stress may be difficult.

One important component of navigating communication and outreach at this time is understanding that clients’ life stages and responsibilities may shape the concerns and fears they have related to COVID-19. Another is knowing that the preferred communication styles of clients may vary, sometimes in predictable ways.

To understand how clients of different ages interact with their financial professionals and how they would like those interactions to change in light of the COVID-19 crisis, the MIT AgeLab, in partnership with AIG Life & Retirement, surveyed over 1,000 people who reported regularly working with a financial professional in March 2020, which was early in the spread of COVID-19 in the United States. Many clients reported having a close relationship with their financial professional, with over one-third saying they were in touch with their financial professional once a month or more. Less than 10 percent of respondents said they spoke to their financial professional once a year or less. Survey respondents were asked about concerns related to their physical health, the health of friends and family, their financial health, and how they are thinking about the future in light of COVID-19.

To help financial professionals weather the storm of economic uncertainty while maintaining strong relationships with clients, this survey aimed to shed light on three key questions financial professionals may be asking themselves right now: (1) What are my clients most worried about? (2) Do my clients want me to reach out to them? (3) What is the best way to reach out to clients if in-person meetings are currently impossible?

The following discussion provides insight into how financial professionals can engage clients in welcome ways throughout the COVID-19 pandemic.

What Are Clients Most Worried About Right Now?

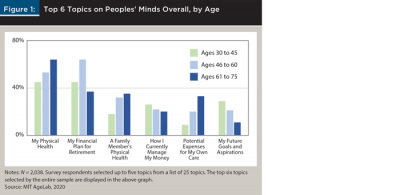

Survey participants were asked what was on their minds the most these days. Figure 1 displays the top six topics that were reported most frequently across the entire sample, broken down by age group.

Physical health was especially on the minds of the oldest age group; almost two-thirds chose this topic as one of their top concerns. This cohort also reported thinking frequently about their financial plan for retirement and a family member’s physical health. Potential expenses for their own care, either current or future, also appeared to weigh heavily on these respondents. They reported more concern about current or future care than respondents in younger age groups.

For the survey’s intermediate age tier (age 46 to 60), personal physical health was also a major concern, but “my financial plan for retirement” was the most-thought-about topic. It was top-of-mind for about two-thirds of this age group. Middle-aged clients also reported thinking about a family member’s physical health and current money management practices.

Finally, although the youngest age group was also concerned with similar topics, their chief concerns were split evenly between their physical health and their financial plan for retirement. While the middle age group reported thinking more about their financial plan for retirement, and the oldest age group thought more about their physical health, the youngest age group appeared to be equally concerned with both.

Understanding the differences among age groups’ responses to topics affected by COVID-19 may help financial professionals address the concerns of particular clients. By understanding these differences, financial professionals may better equip themselves to answer questions that are top-of-mind for their clients, and also bring up important topics that their clients may not be thinking about.

What can you do? Ask your clients what is weighing most on their minds these days. The answer, which may be related both to the client’s responsibilities and stage of life, can help reveal the most effective areas in which you can offer your services, networks, and expertise.

With Everything Going on Right Now, Do Clients Want Me to Reach Out to Them?

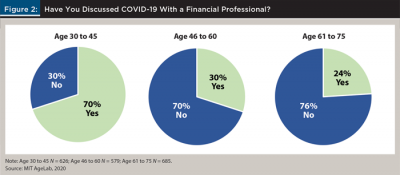

While clients tended to report having a close relationship with their financial professional regardless of age, significant differences appeared among the three age groups when asked if they had spoken to their financial professional about COVID-19 implications (results are displayed in Figure 2). Most respondents in the youngest age group had already discussed COVID-19 with their financial professional, while less than one-third of the 46 to 60 age group, and less than one-quarter of the 61 to 75 age group reported such discussions.

Additionally, the youngest clients who had already had conversations with their financial professionals about COVID-19 were most likely to report having reached out to their professional first, as opposed to their financial professional making the initial overture. In the intermediate age group, about two-thirds reported reaching out to their financial professional first, while only four in 10 respondents did so from the 61 to 75 age group.

For people who had not yet discussed COVID-19 with their financial professional, a lack of conversation did not necessarily mean the topic was off-limits. Across all age groups, approximately one-third of respondents said they would like to discuss implications of COVID-19 with their financial professional, while another half said they would be willing to talk about the implications of COVID-19 with their financial professional if it came up in conversation. Less than 20 percent of respondents surveyed said they were not interested in discussing COVID-19’s implications with their financial professional.

These results suggest that there is an opportunity for financial professionals to reach out proactively to clients—especially those in the middle and older age groups who may be less inclined to reach out themselves. Younger clients may be especially proactive in contacting you right now, but clients of all ages can benefit from knowing that their financial professional is available.

What can you do? Financial professionals have license to reach out to talk not only about short-term financial concerns related to COVID-19, but also clients’ physical health, long-term financial goals, and family anxieties. Reach out—your clients probably want to hear from you.

How Should I Reach Out to Clients if In-Person Meetings Are off the Table?

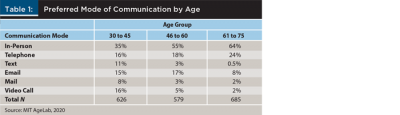

There’s no question that clients prefer in-person meetings. In most areas, however, face-to-face meetings with clients are not feasible due to regulations and recommendations intended to prevent the spread of COVID-19. In the meantime, other modes of communication may offer financial professionals a way to connect and engage with clients. However, it may be important to keep in mind that different age groups may prefer different communication media. Table 1 illustrates preferred communication modes by age group.

For the youngest clients, the preferred mode of communication with financial professionals after an in-person visit was a three-way tie between telephone, email, and video call. The least-preferred mode for this age group was physical mail. Clients in the middle age group also preferred telephone and email. However, they were much less likely than the youngest clients to want to participate in a video call. The least-preferred communication mode for this intermediate age group was text message and physical mail. Like younger clients, respondents in the oldest age group most preferred communication by telephone if in-person communication was not an option. For clients in this age group, all other communication modes ranked well below a telephone call, with text message being the least preferred.

What can you do? With in-person client meetings temporarily suspended, make different communication platforms available to clients so that they can choose how they feel most comfortable communicating with you. When proactively reaching out to clients, consider which mode of communication might be the best fit for their age group.

Tips for Reaching Out to Clients

While deciding how—not if—to reach out to clients during this uncertain time, it is important to personalize the experience. As someone familiar with your clients’ lives, reach out and check in using an appropriate communication platform, then discuss the topics that are most immediately important to them. Keep the following tips in mind when considering how your clients of different ages are faring during the COVID-19 pandemic:

Younger clients. Younger clients may be less experienced than older clients in navigating economic shocks, so they may need extra assurance during a time like this. Your younger clients may also have personal and professional responsibilities that make their near-term and longer-term financial concerns feel overwhelming. This survey revealed that compared with older clients, younger clients were more likely to have reached out to their financial adviser regarding COVID-19, meaning they want to be in touch. When reaching out to reassure and connect with your younger clients, use this opportunity to better understand their larger goals and concerns. Doing so may solidify your working relationship for many years to come.

Middle-aged clients. While younger clients are the most likely to reach out to you, it is also important to ensure that conversations about COVID-19 take place with your middle-aged clients. Reaching out about the financial implications of the pandemic may be especially important for clients in this age group. This survey found that clients from age 46 to 60 are most concerned about their financial plan for retirement. With retirement coming into view, they may feel the effects of market fluctuations acutely. Let your clients know you are here to weather the storm with them.

Older clients. If your clients are like those in this survey, you may not yet have had a conversation about COVID-19 with your older clients. Those with a conservative portfolio may feel less exposed to volatility in financial markets. It is especially important to reach out to them, however, because they may need advice and resources in other domains of their lives. While physical health concerns are top-of-mind for this age group, this survey revealed that these clients are also thinking about their financial plan for retirement, as well as current and future expenses related to their own care. Reaching out to discuss a wide range of topics can help position you as a trusted source of advice now and in the future.

The bottom line—reach out to your clients; they want to hear from you.

Endnotes

- See the 2019 paper, “Factors Associated with Hiring and Firing Financial Advisors During the Great Recession,” by Yuanshan Cheng, Charlene M. Kalenkoski, and Philip Gibson in the Journal of Financial Counseling and Planning, volume 30, issue 2.

- See “Practice Trends: Planners Adjust to Evolving Recession,” by Christina Nelson, in the June 2009 Journal of Financial Planning.

- See the 2014 paper, “Factors Associated with Getting and Dropping Financial Advisors Among Older Adults: Evidence from Longitudinal Data,” by Benjamin F. Cummings and Russell N. James III, in the Journal of Financial Counseling and Planning, volume 25, issue 2.

SIDEBAR: ABOUT THE SURVEY

These findings were taken as part of a broader study MIT AgeLab is conducting in partnership with AIG Life & Retirement to explore the future of the client-adviser relationship.

Methodology

The MIT AgeLab conducted a national survey of 1,215 participants between Tuesday, March 10 and Wednesday, March 18, 2020. The survey asked participants when, where, and how they interacted with financial professionals and what topics they felt most comfortable and interested in discussing. Participants ranged in age from 30 to 75 and reported a yearly household income of $50,000 or more and total savings of $50,000 or more, including savings accounts, checking accounts, and investment or retirement accounts. All participants reported regularly working with a financial adviser.

Sample Characteristics

Survey respondents were distributed relatively evenly across ages (33 percent 30 to 45; 31 percent 46 to 60; 36 percent 61 to 75) and gender (48 percent female; 52 percent male). Additionally, the majority of the sample reported working full-time (58 percent), while the next largest employment group reported being retired (27 percent). Other, smaller employment categories included working part-time, being self-employed, being unemployed, and being a student.