Journal of Financial Planning: August 2018

Chaiwoo Lee, Ph.D., is a research scientist at the MIT AgeLab. Her research focuses on understanding how people across generations accept and use new technologies and services. Her research interests include user-centered design, user experience, consumer behavior, and older adults’ interactions with technology.

Joseph F. Coughlin, Ph.D., is the founder and director of the MIT AgeLab. His research focuses on how demographic change, technology, social trends, and consumer behavior drive innovations in business and government. He is a regular contributor to The Wall Street Journal, MarketWatch, Slate, and the online Disruptive Demographics on BigThink.com. He was appointed by President George W. Bush to the White House Conference on Aging Advisory Committee and has advised non-profits, governments, and corporations worldwide.

Authors’ disclosure: This research was supported by a grant from AARP.

Executive Summary

- This empirical study was conducted to understand people’s perspectives toward retirement and to describe how views differ between people of various characteristics.

- Verbal and visual representations regarding life after completion of a career were collected online from 990 adults in the U.S. to uncover underlying ideas and map key concepts.

- A small number of words and features were reported in descriptions of retirement, indicating both an ambiguity and limitation in relating their current selves to possible future states.

- Perceptions of retirement were generally positive, and a sense of optimism was evident across different segments.

- Some demographic differences were found in thoughts on life after career. For example, people making less than $25,000 a year used fewer positive words and more negative words; younger adults’ images were more likely to address financial well-being; and older adults and those with higher incomes provided more images related to travel.

- Using the results of this analysis, financial planners can better address clients’ emotional needs, rather than solely focusing on rational financial planning.

More americans are in retirement than ever before and are expected to be in retirement longer than previous generations. The number of people aged 65 or older in the United States is expected to grow from about 43 million (13.7 percent of total population) in 2012 to almost 73 million (20.3 percent) in 2030, and then to 84 million (20.9 percent) by 2050 (Ortman, Velkoff, and Hogan 2014). Life expectancy at age 65 was 16 years for men and 19 years for women in 2000, but increased to 18 years for men and 20.5 years for women in 2014, according to 2015 figures from the Organization for Economic Co-operation and Development.1 Longer lives and retirement pose challenges on individual planning behavior. However, not much is known about how people view life after completion of their career.

The links connecting individual characteristics, experiences, and lifestyles to values, perspectives, and goals—which altogether affect future planning behavior—need to be explored in an integrated manner. Differences in how people of various characteristics and backgrounds view and set goals for retirement, or life after career, remain unanswered.

This paper presents an empirical investigation on the values, perspectives, and goals related to retirement that influence planning decisions and saving behaviors. A large-scale online survey was conducted with American adults to determine how people of different characteristics describe life after completion of career, and how values, expectations, and perspectives are represented in their descriptions. In addition to analyzing verbal responses, images were studied using an adaptation of the Zaltman metaphor elicitation technique, or ZMET (Zaltman 1997) to uncover underlying ideas and map key concepts.

Literature Review

Among American households headed by working-age individuals, only 57 percent had retirement savings. The average amount for all households was $95,776, while the median was about $5,000, indicating a wide distribution and disproportion in future planning (Morrissey 2016). Many factors contribute to the differences. The effects of demographic characteristics have been discussed with related concepts, such as financial literacy, life experiences, and perceived well-being.

Studies have found that financial literacy was positively associated with engagement in retirement planning, and that some demographic groups were more financially literate than others (Almenberg and Säve-Söderbergh 2011; Lusardi and Mitchell 2008). Petkoska and Earl (2009) found women to be better than men in the retirement planning areas of health, leisure, and interpersonal relationships. Collinson (2014) reported that millennials expected to self-fund retirement, while Generation X and baby boomers cited retirement accounts and Social Security, respectively, as expected sources of income during retirement.

Studies on happiness and well-being have stated that, after middle age, reported happiness generally increases with age (Kahneman, Krueger, Schkade, Schwarz, and Stone 2004; Steptoe, Deaton, and Stone 2015). Kahneman et al. (2004) also reported that happier people were likely more optimistic. These demographic differences may affect how an individual plans for the future.

People’s ideas of themselves in the future, or their possible selves, have also been shown to influence planning behavior. Defined as personalized representations of one’s self in future states, possible selves identify what one could, hope to, or fear to become in the future (Cross and Markus 1991; Markus and Nurius 1986; Raue, D’Ambrosio, Ellis, Brady, and Coughlin 2017).

Studies have explored how possible selves act as motivators for decisions and behaviors (Markus and Nurius 1986; Peetz and Wilson 2008; Urminsky 2017), and used a variety of constructs (e.g., personal, physical, social, emotional, financial, leisure, personality) to characterize them (Cross and Markus 1991; Fouquereau, Fernandez, Fonseca, Paul, and Uotinen 2005; Raue et al. 2017). These constructs closely match various values associated with retirement planning, which Petkoska and Earl (2009) described as financial, health, interpersonal and leisure, and work.

Other contributors to future planning behavior include people’s goal-setting tendencies and how distant they feel to future goals. Hershey, Mowe, and Jacobs-Lawson (2003) found that people provided with goal-setting exercises were more likely to engage in financial planning. The effects of closeness to future goals and the future self have been studied as applications of the construal level theory, which describes that distant events are represented in more schematic and abstract ways while closer events are more concretely described (Trope and Liberman 2010), and that people who feel less connected to the future seek immediate benefits rather than accept later rewards (Urminsky 2017).

Study Design and Data Collection

A questionnaire was designed to collect people’s thoughts and ideas about life after completion of career. The word “retirement” was not used in the questionnaire to avoid possible bias developed from representations in the media and marketing materials as a time of leisure and freedom.

The first part of the questionnaire focused on descriptions of the future self and asked participants to write up to five words describing their life after career. This is similar to how past research asked about future selves (Cross and Markus 1991; Newby-Clark and Ross 2003; Raue et al. 2017), but different as it focused on a life event rather than leaving the time frame open or attaching an age. Participants were also asked to choose any positive or negative words, instead of separating hopes and fears.

The next part of the questionnaire employed the Zaltman metaphor elicitation technique (ZMET), a method that uses images for understanding abstract ideas, personal meanings, and unconscious mental models (Christensen and Olson 2002; Zaltman 1997). In a typical ZMET, a small and coherent sample of participants are given several days to find images related to a topic and are interviewed to talk about the images (Zaltman 1997). Because this study sought to represent demographic variety with a large sample, an adaptation was used. Participants were asked to provide two images—one showing life today and another representing life after career—at their convenience, and were given spaces to write descriptions. The adaptation enabled efficient data collection from a large and geographically diverse sample.

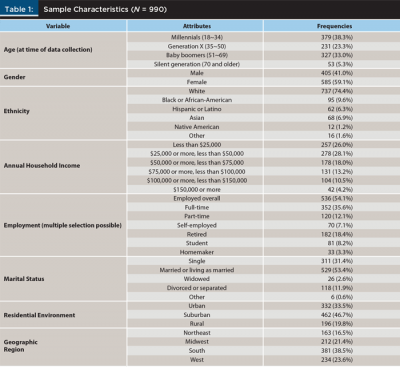

Questions on demographics were asked to understand sample characteristics and enable comparisons between different consumer segments. Data collection was completed online with Qualtrics Panel Management (qualtrics.com) to gather responses from a broad national sample. The dataset included a demographically balanced sample of 990 adults in the U.S. (see Table 1).

Findings from Verbal Descriptions

A limited view of life after career. A total of 4,759 words from 979 people, or valid cases, were used for analysis after removing 11 cases with no readable words. Only 921 different words were found, as many were entered by multiple respondents. The 27 most frequent words accounted for a cumulative frequency of 2,386, representing more than 50 percent of all words. Only 47 words were sufficient for a cumulative frequency of 2,867 (60.2 percent). The 10 most popular words—relax, happy, travel, retirement, family, fun, success, freedom, money, and fulfilled—showed a cumulative count of 1,544 (32.4 percent).

Widespread optimism and focus on emotional values. All respondents were coded in terms of the overall tone and values shown in the words that they provided. Attributes of the overall tone included positive, negative, and neutral. Values included physical, financial, emotional, and social well-being. This is similar to the categorization used in Raue et al. (2017). According to this coding scheme, for example, a person who entered “relax,” “happy,” “content,” “unhealthy,” and “fulfilled” was coded as both positive (for relax, happy, content, and fulfilled) and negative (for unhealthy), and also as physical (for unhealthy) and emotional (for relax, happy, content, and fulfilled).

Coding was done regarding the meaning of words themselves, rather than assuming possible underlying contexts. For example, while “unhealthy” could describe a positive context where the respondent envisions working as long as he or she was healthy, it was coded as negative per its definition.

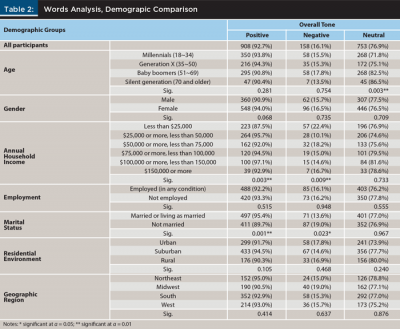

Results of coding, as shown in Table 2, showed that perceptions of life after career were generally positive and optimistic. Among the 979 valid cases, 908 included one or more positive words, while only 158 included one or more negative words. Words addressing emotional values were the most prevalent. These were found in the majority of cases (86.5 percent), while physical (46.6 percent), financial (42.6 percent), and social (38.1 percent) values were represented in fewer cases.

This sense of optimism was evident across demographic segments. More than 90 percent of participants in all age groups and both genders provided one or more positive words. Differences were found for income and marital status, where people in the lowest income bracket and unmarried participants entered significantly fewer positive words compared to higher income segments and married participants. However, even in these groups, positive words remained the majority. A focus on emotional well-being was also universal, with more than 80 percent of people in all specified segments providing words related to emotional values.

Focus on physical and financial values differed between some segments. The focus on physical values increased with age and was more emphasized among men than women. Other characteristics associated with heavier emphasis on physical values included being married or living as married, and living in suburban or rural areas. Employed participants were more likely to focus on financial values compared to unemployed respondents, and those in suburban or rural areas entered more words related to financial values compared to those in urban areas.

Perceptual Mapping

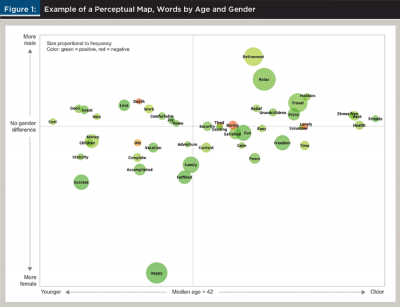

The top 47 words were analyzed to further illustrate how different ideas were associated with key demographic characteristics. The following information was recorded: overall frequency, prevalence in each gender, and average age and household income among people who entered each word. A positivity score was calculated for each word with a separate survey, where a convenience sample of 39 English-speaking adults rated the positivity/negativity of each word using a five-point scale, ranging from 1 for very negative to 5 for very positive. For example, “relax” was entered by 28.9 percent of males and 24.8 percent of females with an average age of 47.6, an average household income level of 2.86 (where 2 = $25,000~$50,000, and 3 = $50,000~$75,000), and had an average positivity score of 4.46.

Perceptual maps were created to illustrate the recorded information. In these maps, each word is shown in a circle, with its size proportional to the frequency (i.e., words with higher frequencies are encased in larger circles). The color represents positivity, where red corresponds to an average score of 1 (very negative), green represents an average score of 5 (very positive), and yellow stands for 3 (neutral). Figure 1 shows an example of perceptual map.

Figure 1 illustrates age and gender differences in how people describe life after career. Older respondents were more likely to address social interactions (e.g., “friends” and “lonely”) and describe actions (e.g., “travel,” “hobbies,” and “volunteer.”) In contrast, younger participants provided very vague words (e.g., “good,” “great,” “nice,” and “cool.”).

Men talked about freedom from responsibilities (e.g., “retirement” and “relax”), and more women gave words describing achievement (e.g., “accomplished,” “fulfilled,” “success,” and “complete.”)

Additional maps looked at associations with income. They showed that negative words such as “old,” “lonely,” and “death” were associated with lower income, while positive words including “volunteer,” “exciting,” “stress-free,” “good,” “independent,” and “relief” came from higher-income individuals. “Death” was mostly mentioned by younger males with lower income, and “hobbies” and “travel” were popular among older males with higher income.

Findings from Visual Representations

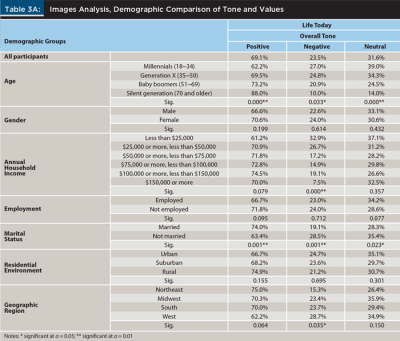

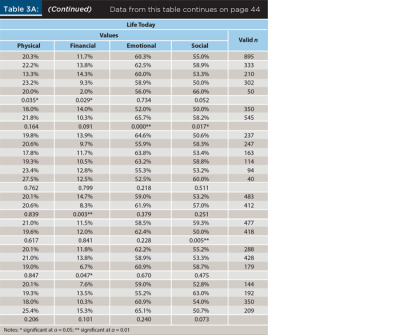

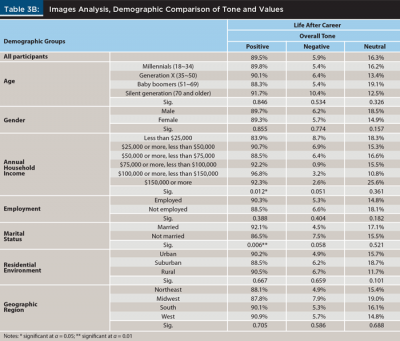

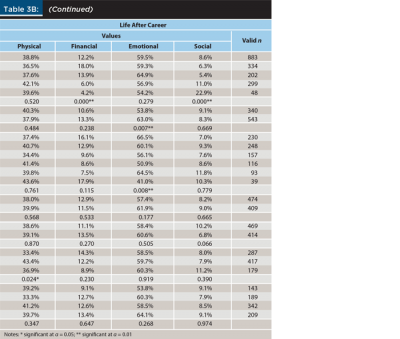

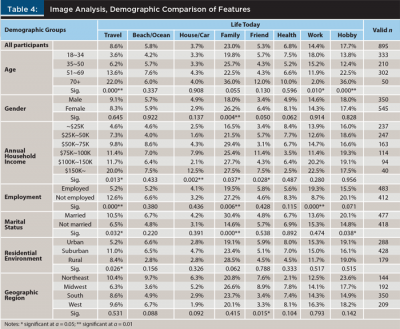

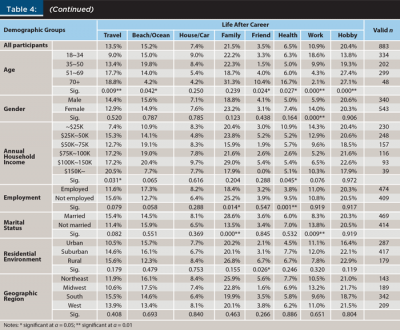

A total of 895 pictures describing life today and 883 pictures representing life after career were used for analysis. Similar to the words, all images were coded in terms of the overall tone—positive, negative, and neutral—and related values—physical, financial, emotional, and social (see Table 3). Also, features shown in the images were identified and recorded (see Table 4). Descriptions provided by the participants were referenced during the coding process.

Hopes for the Future

As shown in Table 3, the majority (69.1 percent) of images describing life today were positive, while fewer images were negative (23.5 percent) or neutral (31.6 percent), with some showing mixed tones. Descriptions varied across segments. For instance, older participants were more likely to describe life today with positive images compared to younger respondents. Participants who were married or living with a partner uploaded more positive images about life today than those who were single. The frequency of negative images decreased significantly with income.

The sense of optimism and positivity was even greater for the future, and demographic differences diminished in images showing life after career. The vast majority of images for the future was positive (89.5 percent), while only a small portion showed negative (5.9 percent) or neutral tones (16.3 percent). Of the 618 people who provided positive images for describing today, 536 also provided positive images for describing life after career. Furthermore, while 210 people gave negative images for life today, 170 of them provided positive images to show views of life after career.

Changes in Values

The majority of images describing life today was related to emotional (60.3 percent) and social well-being (55 percent). Fewer images were associated with physical (20.3 percent) and financial values (11.7 percent), as shown in Table 3. Images describing life after career were also heavily focused on emotional values (59.5 percent), but much less on social values (8.6 percent). Also, compared to life today, a larger number of images for life after career were associated with physical values (38.8 percent). Most of these images were positive (305 positive images among 343 showing physical values), with many showing exercising and traveling.

As shown in Table 3, younger participants were more likely to provide images addressing financial values for both life today and after career. For life today, these images described financial hardships. In contrast, their images describing life after career showed wealth and financial stability. Generational differences were observed for social values as well. For life after career, older adults were more likely to provide images showing social values.

Family was featured in 23 percent of images representing life today, making it the most prominent feature. Other popular features for life today included hobby and work, as shown in Table 4. Similarly, many images showing life after career displayed family, hobby, and work. The biggest differences between life today and after career were observed for travel-related images. For example, beaches or oceans were found in 15.2 percent of images describing life after career, which was more than double the frequency among images showing life today. This strong representation of travel-related features is consistent with findings from the verbal portion of this study, where “travel,” “relax,” and “vacation” were frequently entered.

For both life today and after career, older participants provided more images showing travel and hobbies than younger generations, and younger participants provided more images related to work than older participants. Travel-related images were also provided more by those with higher incomes. Images showing family were provided more by unemployed participants and females compared to their counterparts, as shown in Table 4.

Discussion and Implications

This study explored how people of various characteristics describe and imagine retirement, or life after completion of career. Based on words and images collected from 990 adults in the U.S., this study sought to understand the values, expectations, and perspectives regarding retirement, and to describe how those compare between people of different demographic characteristics.

Frequency analysis revealed that only a handful of vocabulary was used to describe life after career. The 10 most frequent words accounted for almost one-third of all responses, and only 27 words were sufficient to make up half of collected data. Considering that an average American is estimated to have a vocabulary size larger than 40,000 (Brysbaert, Stevens, Mandera, and Keuleers 2016), a tiny fraction is being used to describe a significantly lengthy period.

The ambiguity and limited vocabulary associated with retirement might be explained with the construal level theory, which describes that distant future is represented in schematic and abstract ways due to temporal and psychological distance (Peetz and Wilson 2008; Trope and Liberman 2010). Because participants were asked to think about an intangible future state, their answers may have been bounded to a small, abstract, and coherent set of words. The observation that younger respondents used more vague and abstract words, while older respondents used more specific words, further supports this explanation.

The finding can also be explained with portrayals of retirement in public media. Ekerdt and Clark (2001) observed that the majority of retirement advertisements did not depict visual images, and the small portion that did focused on leisure and freedom. Such limitation in consumers’ exposure to related concepts may have impacted the results, where “relax” and “travel” were among the most frequent.

People were generally optimistic about life after completion of career. Most of the words were positive, and images showing life after career were generally more positive compared to images representing today. A possible explanation can come from the positivity bias, or the Pollyanna Hypothesis, which describes that people universally tend to use positive words more frequently and diversely than negative words (Boucher and Osgood 1969; Dodds et al. 2015). It is also aligned with past research that found people to be more optimistic about the distant future compared to the imminent future (Peetz and Wilson 2008).

The majority of such positive words and images addressed emotional values, suggesting a higher emphasis on pursuing emotional fulfillment in retirement. This may be due to related media that mostly convey positive contents around leisure, freedom, personal pursuit, and financial security (Ekerdt and Clark 2001).

Results showed some differences in how different segments view life after career. For example, older participants, suburban and rural residents, married people, and men provided more words addressing physical values compared to their counterparts. A perceptual mapping approach further revealed how some segments may be more or less likely to use certain words. In the images, the positivity gap between the present and the future were greater among younger participants. However, while images from the younger participants showed wealth, family, and accomplishments with a positive lens, their descriptions lacked in how they plan to reach the ideal future state.

These findings have practical implications for the evolving roles of financial planners as curators, educators, and co-creators of retirement. The limited vocabulary and imagery imply that clients may not have a clear, or realistic, vision of retirement. Results suggest that planners may have a new role as curators of possible lifestyles for clients to consider and plan for.

Respondents reflected inordinately high positivity about their future retired selves. Financial planners may not want to dissuade clients of looking optimistically, but they may find an important role as educators in tempering popular images of beach walks and green fairways with candid discussions of possible futures that may be costly and less positive.

As co-creators of their clients’ retirement vision, planners may need to be more cognizant of the language they use and the topics they emphasize by the characteristics of clients for a successful collaboration. For example, focusing on the implications of physical health may be more effective in engaging older men, while middle-aged women may be more attuned to seeing retirement as a personal new start after a lifetime of giving time to others.

The results can be used to guide planning practitioners as they choose images, words, and concepts to create relatable communication materials and improve ways of direct consumer engagement.

To compensate for possible limitations of this work, future research should expand our understanding of the public’s retirement vocabulary and emotional biases in financial planning. For example, a larger sample would provide additional insight into the positivity bias revealed in the current research, which showed greater optimism than existing research that explored the divergence between objective and subjective retirement preparedness (Kim and Hanna 2015). In addition, in-depth interviews or focus groups may provide deeper insights.

Endnote

- See “Life Expectancy at 65” at data.oecd.org/healthstat/life-expectancy-at-65.htm.

References

Almenberg, Johan, and Jenny Säve-Söderbergh. 2011. “Financial Literacy and Retirement Planning in Sweden.” Journal of Pension Economics and Finance 10 (4): 585–598.

Boucher, Jerry, and Charles E. Osgood. 1969. “The Pollyanna Hypothesis.” Journal of Verbal Learning and Verbal Behavior 8 (1): 1–8.

Brysbaert, Marc, Michaël Stevens, Paweł Mandera, and Emmanuel Keuleers. 2016. “How Many Words Do We Know? Practical Estimates of Vocabulary Size Dependent on Word Definition, the Degree of Language Input, and the Participant’s Age.” Frontiers in Psychology 7: 1,116.

Christensen, Glenn L., and Jerry C. Olson. 2002. “Mapping Consumers’ Mental Models with ZMET.” Psychology and Marketing 19 (6): 477–502.

Collinson, Catherine. 2014. “The Retirement Readiness of Three Unique Generations: Baby Boomers, Generation X, and Millennials.” Transamerica Center for Retirement Studies. Available at transamericacenter.org/docs/default-source/resources/center-research/tcrs2014_sr_three_unique_generations.pdf.

Cross, Susan, and Hazel Markus. 1991. “Possible Selves across the Life Span.” Human Development 34 (4): 230–255.

Dodds, Peter S., Eric M. Clark, Suma Desu, Morgan R. Frank, Andrew J. Reagan, Jake R. Williams, Lewis Mitchell et al. 2015. “Human Language Reveals a Universal Positivity Bias.” Proceedings of the National Academy of Sciences of the United States of America 112 (8): 2,389–2,394.

Ekerdt, David J., and Evelyn Clark. 2001. “Selling Retirement in Financial Planning Advertisements.” Journal of Aging Studies 15 (1): 55–68.

Fouquereau, Evelyne, Anne Fernandez, Antonio M. Fonseca, Maria C. Paul, and Virpi Uotinen. 2005. “Perceptions of and Satisfaction with Retirement: A Comparison of Six European Union Countries.” Psychology and Aging 20 (3): 524–528.

Hershey, Douglas A., John C. Mowe, and Joy M. Jacobs-Lawson. 2003. “An Experimental Comparison of Retirement Planning Intervention Seminars.” Educational Gerontology 29 (4): 339–359.

Kahneman, Daniel, Alan B. Krueger, David Schkade, Norbert Schwarz, and Arthur Stone. 2004. “Toward National Well-Being Accounts.” The American Economic Review 94 (2): 429–434.

Kim, Kyoung Tae, and Sherman D. Hanna. 2015. “Do U.S. Households Perceive Their Retirement Preparedness Realistically?” Financial Services Review 24: 139–155.

Lusardi, Annamaria, and Olivia S. Mitchell. 2008. “Planning and Financial Literacy: How Do Women Fare?” American Economic Review 98 (2): 413–417.

Markus, Hazel, and Paula Nurius. 1986. “Possible Selves.” American Psychologist 41 (9): 954–969.

Morrissey, Monique. 2016. “The State of American Retirement: How 401(k)s Have Failed Most American Workers.” Economic Policy Institute’s Retirement Inequality Chartbook. Available at epi.org/files/2016/state-of-american-retirement-final.pdf.

Newby-Clark, Ian R., and Michael Ross. 2003. “Conceiving the Past and Future.” Personality and Social Psychology Bulletin 29 (7): 807–818.

Ortman, Jennifer M., Victoria A. Velkoff, and Howard Hogan. 2014. “An Aging Nation: The Older Population in the United States.” United States Census Bureau Current Population Reports. Available at census.gov/prod/2014pubs/p25-1140.pdf.

Peetz, Johanna, and Anne E. Wilson. 2008. “The Temporally Extended Self: The Relation of Past and Future Selves to Current Identity, Motivation, and Goal Pursuit.” Social and Personality Psychology Compass 2 (6): 2,090–2,106.

Petkoska, Jasmina, and Joanne K. Earl. 2009. “Understanding the Influence of Demographic and Psychological Variables on Retirement Planning.” Psychology and Aging 24 (1): 245–251.

Raue, Martina, Lisa A. D’Ambrosio, Dana Ellis, Samantha Brady, and Joseph F. Coughlin. 2017. “Imagine Being 70: Future Possible Selves and Preparedness for Old Age.” Poster presented at the Annual Meeting of the Society for Personality and Social Psychology, San Antonio, Texas, January 2017.

Steptoe, Andrew, Angus Deaton, and Arthur Stone. 2015. “Subjective Wellbeing, Health, and Ageing.” Lancet 385 (9968): 640–648.

Trope, Yaacov, and Nira Liberman. 2010. “Construal-Level Theory of Psychological Distance.” Psychological Review 117 (2): 440–463.

Urminsky, Oleg. 2017. “The Role of Psychological Connectedness to the Future Self in Decisions Over Time.” Current Directions in Psychological Science 26 (1): 34–39.

Zaltman, Gerald. 1997. “Rethinking Market Research: Putting People Back In.” Journal of Marketing Research 34 (4): 424–437.

Citation

Lee, Chaiwoo, and Joseph Coughlin. 2018. “Describing Life After Career: Demographic Differences in the Language and Imagery of Retirement.” Journal of Financial Planning 31

(8): 36–47.