Journal of Financial Planning: April 2012

William Meyer is founder and CEO of Retiree Inc., a registered investment adviser that develops tools for advisers and retail investors focused on tax-efficient withdrawal and distribution planning. (wmeyer@retireeinc.com)

William Reichenstein, Ph.D., CFA, is the Powers Professor of Investments at Baylor University and a principal of Retiree Inc. (Bill_Reichenstein@baylor.edu)

Executive Summary

- This study illustrates how the Social Security claiming decision can affect the longevity of retirees’ financial portfolios.

- The claiming decision or claiming strategy refers to the month in which the single retiree begins Social Security benefits. For a couple, claiming strategy refers to the months in which each partner begins his or her own benefits and, when applicable, spousal benefits.

- Reichenstein and Meyer (2011) illustrate that different claiming strategies can produce significant differences in real cumulative lifetime benefits. As a result, it is common sense that if you select a claiming strategy that garners more real lifetime benefits it will extend the longevity of the retiree’s financial portfolio.

- This is the first study to provide estimates of how much longer the financial portfolio will last if a retiree delays the beginning of Social Security benefits.

In Meyer and Reichenstein (2010) and Reichenstein and Meyer (2011), we explain that two criteria should affect retirees’ claiming strategies. First, which claiming month for singles or claiming strategy for couples will maximize the present value of expected lifetime benefits. Second, which claiming strategy will minimize the longevity risk of the financial portfolio. This paper is the first study to estimate how much longer the financial portfolio will last if a retiree delays the beginning of Social Security benefits. As such, it should help retirees make an informed decision about the trade-off between maximizing expected benefits and minimizing longevity risk. Although we specifically model the impact of delaying Social Security for single individuals, we also explain why these results should prove useful for couples. In addition, we examine how the additional portfolio longevity varies with the size of the financial portfolio, the primary insurance amount, the planning horizon, and the sizes of both nominal and real rates of return. In short, this study provides information necessary for financial planners to help their clients decide when to claim Social Security benefits.

The 4 Percent Rule

We designed our study to fit within the withdrawal rate literature. Financial planners know the 4 percent rule. It says that a new retiree can withdraw 4 percent of his or her initial portfolio in the first year of retirement and an inflation-adjusted equivalent amount each year thereafter, and be reasonably confident that his or her financial portfolio will survive 30 years. Most new retirees do not live 30 years. However, the profession generally recommends that the retiree plan to live for a longer horizon than life expectancy to provide reasonable assurance of not outliving financial resources. The 4 percent rule says a 62-year-old single retiree could withdraw $40,000 the first year from a $1 million retirement portfolio, increase the withdrawal amount with inflation each year, and be reasonably confident the portfolio will survive 30 years.1

The 4 percent rule is a useful guideline. But it has limitations, two of which are that it ignores Social Security and taxes. In this study, we retain the spirit of the 4 percent rule, but we extend the withdrawal rate literature by introducing Social Security and taxes.

Minimizing Longevity Risk

This section presents estimates of how delaying the start of Social Security would affect the longevity of a single retiree’s financial portfolio. To make the analysis manageable and to keep it in the spirit of the withdrawal rate literature, we adopt certain assumptions. We assume the retiree wants to spend a constant after-tax real amount each year in a 30-year retirement period. Consistent with the 4 percent rule, we assume a constant real return of 1.22 percent per year.2 The individual begins retirement at 62. Each year in retirement, he or she determines the level of Social Security benefits, if any, and withdraws whatever amount is necessary from his or her financial portfolio to provide the target after-tax spending amount. The nominal spending target increases each year with inflation, so the real spending level is constant. Unless otherwise stated, all numbers in this study are presented in terms of today’s dollars.

The major goal of this study is to determine how delaying the beginning of Social Security benefits from age 62 to 64, 66, 68, and 70 would affect the projected longevity of a single retiree’s financial portfolio for various levels of wealth. We consider two single retirees. The first has a primary insurance amount (PIA) of $1,500, a 30-year planning horizon, and we vary his level of wealth from $200,000 to $1.5 million. PIA denotes the monthly benefit level in today’s dollars if benefits begin at full retirement age (FRA). We believe the PIA of $1,500 is representative of the PIA for an average financial planning client without a high net worth. For each level of wealth, we first calculate the level of annual real spending that his financial portfolio and Social Security can accommodate if he has a 30-year planning horizon, retires at 62, and starts Social Security benefits at 62. We then calculate the additional longevity of his portfolio if he retires at 62 but delays the start of benefits until 64, 66, 68, and 70. Also, for each level of wealth we calculate the maximum sustainable annual real spending level for a 30-year planning horizon when delaying the start of benefits until 70. In separate analyses, we consider how shortening the planning horizon to 25 years would affect the additional longevity possible from delaying the start of Social Security benefits.

The second retiree has a PIA of $2,400, a 30-year planning horizon, and we vary her level of wealth from $500,000 to $3 million. This PIA is near the upper end of the range for a single individual. We perform the same calculations for this second retiree as we did for the first.

PIA of $1,500, 30-Year Horizon

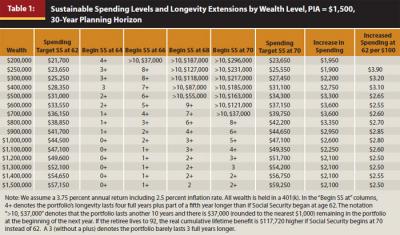

In Table 1, we assume the retiree’s PIA is $1,500, his FRA is 66, and the planning horizon is 30 years. His Social Security real monthly benefits will be $1,125 if he begins benefits at 62, $1,300 at 64, $1,500 at 66, $1,740 at 68, or $1,980 at 70.

To understand this table, consider a single retiree with $700,000 in a 401(k) or other tax-deferred account. If he begins Social Security benefits at 62 in January 2011, then based on the 2011 tax code, he could spend $36,150 the first year, an inflation-adjusted equivalent amount each year thereafter, and his financial portfolio would barely last 30 years.3 We then ask how much longer his portfolio would last if he maintains the same real spending target but delays the start of benefits until 64, 66, 68, and 70. The “Begin SS at 64” column indicates that if he retires at 62 but begins Social Security benefits at 64, his portfolio will last 1+ additional years (one more year plus some funds for a second year). If he begins Social Security benefits at 66 or 68, his portfolio will last 4+ or 7+ additional years compared with a strategy of beginning benefits at 62. If he begins Social Security benefits at 70, his portfolio will last 10+ additional years. At that time, he will be 102. Instead of calculating the additional years beyond age 102 that the portfolio would last, we indicate that the nominal size of his financial portfolio would be $37,000 (rounded to the nearest thousand) at the beginning of that year.4

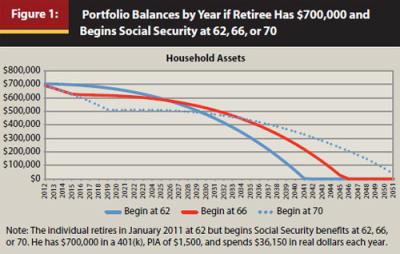

Figure 1 illustrates the additional portfolio longevity for this retiree with $700,000 in financial wealth from delaying Social Security benefits from 62 to 66 and to 70. The begin-at-62 strategy line indicates the beginning balance in the 401(k) by year if he starts Social Security benefits at 62. The begin-at-66 and begin-at-70 strategy lines indicate the beginning balances by year if he starts Social Security benefits at 66 and 70. In the begin-at-62 strategy, he receives $13,500 a year in Social Security real benefits. Therefore, he will have to withdraw a relatively small amount from his financial portfolio in 2011 to meet his spending target. From Figure 1, if he begins benefits at 62, his portfolio will have the highest balance before the beginning of 2026.

In the begin-at-70 strategy, his portfolio has the fewest dollars in 2019 because all funds to meet the annual spending goal for the prior eight years came from his financial portfolio. Beginning at 70, he will receive $23,760 a year in Social Security real benefits. Thenceforth, to meet his real spending target he will need to withdraw the smallest amount from his financial portfolio each year. Consequently, this strategy’s portfolio balance decreases the slowest after 2019. From 2034 and later, the begin-at-70 strategy’s portfolio balance is the highest of these three strategies. From Table 1 and Figure 1, if he delays Social Security benefits until 70, his portfolio will last 10 more years and still have remaining a nominal value of approximately $37,000.

The “Spending Target SS at 70” column indicates how much higher his annual real spending target could be if he retains the 30-year planning horizon but delays the start of benefits until 70. If he retires at 62 with $700,000 in financial wealth but delays Social Security benefits until 70, his portfolio plus Social Security would support a $39,750 annual real spending amount and barely last 30 years. As the next column indicates, this is $3,600 more than the real spending amount his portfolio plus Social Security could support if he began Social Security at 62. For the 30-year planning horizon, this represents about $130,000 more in cumulative real spending. Moreover, if he lives more than 30 years, this $130,000 understates the advantage of delaying Social Security until 70—by doing so his monthly Social Security benefits would be 76 percent higher than if he began benefits at 62.

Lessons

There are four lessons from the analysis embedded in Table 1. First, a retiree can extend the longevity of his portfolio by delaying the start of Social Security. The longer he delays Social Security benefits, the longer his portfolio will last. As we have seen, the single retiree with $700,000 in financial wealth can extend the longevity of his portfolio by 1+, 4+, 7+, and 10+ years by delaying Social Security benefits from 62 to 64, 66, 68, and 70.

These results also have implications for couples. Consider that after the death of the first spouse, the surviving spouse generally continues the higher of the two partners’ monthly benefits but loses the lower monthly benefit. Therefore, the higher PIA spouse’s benefits will continue until the second spouse dies. Thus, the relevant life expectancy of the higher PIA spouse is the age he or she would be when the second spouse dies. For example, suppose a husband has the higher PIA but a short life expectancy of 75, and his three-year-younger wife has a life expectancy of 89. To maximize the couple’s joint lifetime benefit, the husband should delay his Social Security benefits until 70 because benefits based on his earnings record are calculated to continue until he would be 92.

The second lesson is that the additional longevity from delaying Social Security decreases as the level of wealth increases. This statement is true no matter what age Social Security begins. For example, if Social Security begins at 64 instead of 62, the portfolio’s longevity is 4+ years longer for retirees with $200,000 but only 3+ years longer for retirees with $250,000. For retirees with wealth levels of $1 million or higher, the additional longevity from delaying Social Security benefits until 64 is less than one year. Therefore, the strongest longevity gains are associated with retirees with lower levels of financial wealth.

It is easy to explain why delaying the start of Social Security benefits extends the portfolio’s longevity. For each year Social Security benefits are delayed from age 62 to 70, the real level of monthly benefits grows by 6.45 to 8.34 percent.5 But each year of delay results in one less year of benefits. Nevertheless, if the retiree lives to age 92 and delays Social Security from 62 to 70, cumulative real benefits are 29.1 percent higher.6 Assuming this 30-year retirement period, cumulative real benefits grow at a 3.85 percent annual rate from delaying benefits from 62 to 64.7 The corresponding real annual growth rates in cumulative benefits are 3.51 percent from delaying benefits from 64 to 66, 3.48 percent from 66 to 68, and 2.13 percent from 68 to 70. So, the benefit of delaying benefits for the long-lived is strongest from age 62 to 64.8

Conceptually, you can think of retirement resources as consisting of two parts: the financial portfolio and Social Security benefits. If a retiree lives a long time (for example, until age 92), the returns from delaying Social Security benefits are strong. So, it pays to delay. This concept also explains why the additional longevity from delaying Social Security benefits decreases as financial wealth increases. For the low-wealth client, Social Security represents a larger portion of retirement resources, so delaying Social Security benefits has a stronger effect on the portfolio’s longevity. This may be the most important conclusion to come from this study.

Most people approach their retirement years with relatively low levels of financial wealth.9 For retirees with average or above-average life expectancies, the ability to defer Social Security benefits, even if only for a few years, may provide their last and best remaining hope of extending the expected longevity of their financial portfolios. Obviously, a retiree with a short life expectancy may not be concerned about the risk of outliving savings, but this is a concern for many retirees.

The third lesson: retirees with more than $200,000 of wealth can increase annual real spending by less than $4 for each additional $100 of pretax funds in the 401(k). The 4 percent rule says a retiree can increase his annual real withdrawal by $4 per year for each additional $100 of financial assets. Unlike withdrawals, spending requires after-tax dollars. Because the 4 percent rule ignores taxes, it is silent on the effect of an additional $100 in financial wealth on spending.

The “Increased Spending at 62 per $100” column indicates the increased real spending level per $100 increase in pretax balances in the 401(k). For example, an increase in wealth from $200,000 to $250,000 allows an increase in spending of $3.90 per $100 increase in wealth ($100 x [($23,650 – $21,700)/($250,000 – $200,000)]). The results indicate that a retiree with a very low net worth can increase his annual real spending by about $4 per $100 of additional wealth. However, at higher levels of wealth the additional annual real spending per $100 of wealth is well below $4.

The pattern of numbers in this column is partly attributable to the taxation of Social Security benefits.10 As the wealth level rises from $200,000 to $900,000, the percent of Social Security benefits subject to taxes rises from 2.1 percent to 83.0 percent for the 30-year horizon. They go from being essentially tax free to 85 percent taxable, with the latter being the maximum taxable portion of benefits. Most of the rise in the taxable portion of Social Security benefits occurs between $200,000 and $600,000. In this range, each dollar withdrawn from the 401(k) usually causes either an additional $0.50 or $0.85 of Social Security benefits to be taxable. Thus, the retiree’s marginal tax rate is usually either 50 percent or 85 percent higher than his tax bracket. For example, if the tax bracket is 15 percent, an additional $100 withdrawn from the 401(k) may cause taxable income to rise by $185, which would cause taxes to increase by $27.75 (15 percent of $185). Because $27.75/$100 is 27.75 percent, the marginal tax rate is 85 percent higher than the tax bracket.

This hump in the marginal tax-rate curve is sometimes called the tax torpedo. It accounts for the pattern in the “Increased Spending at 62 per $100” column. As wealth rises from $200,000 to $600,000, the portion of Social Security benefits taxable over the 30-year retirement period increases sharply. So the increased spending amount falls. By the time financial wealth reaches $600,000, most of the damage from the taxation of Social Security benefits has already been done. So, as wealth increases from $600,000 to $900,000, the increased spending amount rises.

The fourth lesson is that by delaying the start of Social Security benefits, the retiree can increase his real spending level and still have the portfolio last 30 years. The “Spending Target SS at 70” column presents the real spending target the financial portfolio could sustain for 30 years if the retiree quits working at 62 but delays Social Security benefits until 70. For the retiree with $700,000 in wealth, the begin-at-70 strategy would support $39,750 in real spending per year for 30 years. The “Increase in Spending” column indicates that this is $3,600 higher than the $36,150 target the begin-at-62 strategy would support. As wealth levels increase beyond $700,000, the amount in this column decreases. For example, it falls to $2,600 and $2,100 for retirees with $1 million and $1.5 million of financial wealth, respectively.

We now turn to an explanation of the increasing amounts in this column as wealth increases from $250,000 to $600,000. This increase results from the taxation of Social Security benefits. Consider a 62-year-old retiree deciding whether to begin Social Security benefits at 62 or 70. If she begins Social Security benefits at 62, when she is 70 or older she will receive a relatively low amount of Social Security benefits and need to withdraw a relatively high amount from her 401(k) compared with the amount if she begins benefits at 70. Because of the tax code, she will pay taxes on fewer dollars of Social Security benefits if she begins these benefits at 70. This is explained next.

The taxable portion of Social Security depends on the level of provisional income (PI, also known as combined income). A review of the rules affecting the taxation of Social Security benefits reveals why delaying Social Security can reduce the taxable portion of benefits. In equation form, PI = modified adjusted gross income + 0.5 x Social Security benefits + tax-exempt interest. For this retiree, PI is the sum of the 401(k) withdrawal and half of Social Security benefits. By delaying Social Security from age 62 to 70, the retiree gets an additional $10,260 per year in Social Security benefits in today’s dollars. So she can withdraw about $10,260 less per year from the 401(k). Because only half of Social Security benefits go into PI, the combination of $10,260 more in Social Security benefits and $10,260 less in 401(k) withdrawals results in a PI about $5,130 lower.11 The lesson, especially for retirees in the $250,000 to $600,000 wealth range, is that one benefit of delaying Social Security is that less of those benefits will be taxable.12

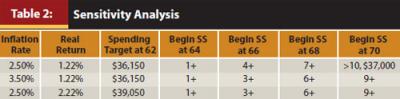

Table 2 examines the sensitivities of the additional longevity estimates to assumed investment rates of return. We assumed a real return of 1.22 percent and inflation rate of 2.5 percent for a constant nominal investment return of 3.75 percent [(1.0122)(1.025) – 1], where 1.22 percent is the constant real rate that corresponds to the 4 percent rule. For a retiree with a wealth level of $700,000, if we assume a 1 percent higher inflation rate, the retiree who begins Social Security benefits at 62 can still spend $36,150 in real dollars each year for 30 years. The additional longevities if benefits begin at 64, 66, 68, and 70 are 1+, 3+, 6+, and 9+ years longer, respectively, than if benefits begin at 62. These additional longevity estimates show little sensitivity to the assumed inflation rate because Social Security benefits, nominal investment returns, and nominal annual spending rise with inflation as well as marginal tax brackets, standard deduction, and personal exemption deduction. However, Social Security taxes increase with inflation because the threshold amounts are not adjusted for inflation.

If the real rate rises by 1 percent, this retiree can begin Social Security benefits at 62 and spend $39,050 in real dollars each year, and the portfolio will last 30 years. This spending level is substantially higher. However, the additional portfolio longevities if benefits begin at 64, 66, 68, and 70 are 1+, 3+, 6+, and 9+ years longer, respectively, than if benefits begin at 62. These additional longevity estimates show little sensitivity to the assumed real rate of return.

In short, the level of annual real spending the portfolio and Social Security can support is positively related to the assumed real rate of return. However, the additional portfolio longevity estimates from delaying Social Security benefits show little sensitivity to either the assumed inflation rate or real return. Thus, the estimates of additional portfolio longevity from delaying Social Security benefits should prove useful across a range of inflation-rate and real-rate-of-return assumptions.

PIA of $1,500, 25-Year Horizon

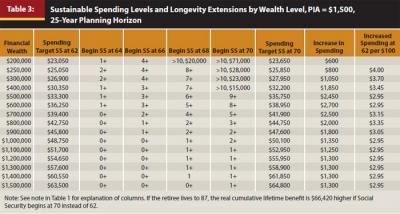

Table 3 provides the corresponding information as in Table 1, except it assumes the planning horizon is 25 years. The results are qualitatively similar to the results in Table 1, except the additional longevities tend to be shorter. For example, with $700,000 of financial wealth, the additional longevity from delaying Social Security from 62 to 64, 66, 68, and 70 is 0+, 2+, 4+, and 5+ years, respectively, whereas the corresponding numbers were 1+, 4+, 7+, and 10+ years with a 30-year horizon.

Although not shown, if the planning horizon were 22 years and the real return were 3 percent per year, the decision about when to begin Social Security benefits would have little effect on the portfolio’s longevity. This reflects the fact that the Social Security actuaries set the reductions in benefits for starting Social Security before FRA and the delayed retirement credits for delaying benefits until after FRA to be approximately actuarially fair for a single retiree with average life expectancy of 84, assuming a 3 percent real rate of return.

PIA of $2,400, 30-Year Horizon

Table 4 provides the corresponding information as in Table 1, except it assumes the single retiree has a PIA of $2,400 and a 30-year planning horizon. It considers wealth levels of $500,000 to $3 million in increments of $250,000. The lessons are the same for retirees with PIAs of $1,500 or $2,400.

Limitation of Study

One limitation of this study is the absence of simulated returns such as in Monte Carlo analysis. Instead of using simulated returns, we assume a 1.22 percent real return, which is below historical averages and thus a “bad” return series. Similarly, sequence-of-returns risk refers to a “bad” series of returns, especially in the first few retirement years. By intent, the 4 percent rule should reflect a bad return series such that the portfolio will last the planning horizon all or almost all the time despite the bad returns. As noted, the 1.22 percent real return is the bad return series consistent with the 4 percent rule. Ideally, we would have included a simulation analysis, but our model does not accommodate this method.

Behavioral Deterrents

Lastly, in private conversations, we have heard people say they want to begin Social Security early because: (1) they cannot afford to delay, (2) they want to get whatever benefits they can before Social Security goes broke, and (3) they want to preserve their financial portfolio for as long as possible. The first argument has no merit because we have held the annual real spending level constant in these analyses. We next address the other two arguments.

There is no doubt Social Security rules affecting benefits will change. However, we join others who predict that these changes are not likely to materially impact anyone over the age of about 55. For example, a Congressional Budget Office report says, “Proposals to change Social Security ... would not reduce benefits for people older than 55.” Similarly, in a project for the Center for Financial Literacy at Boston College, Sass, Munnell, and Eschtruth (2009a) wrote in The Social Security Claiming Guide, “Don’t start [benefits] early because Social Security has money problems.... You won’t get more if you do.” The Social Security Fix-It Book by Sass, Munnell, and Eschtruth (2009b) discusses potential changes to the Social Security system. They include raising the FRA, linking benefits for earnings in years before age 60 to inflation instead of the average wage level, raising payroll taxes, earmarking estate-tax revenue for Social Security, and diversifying the Social Security trust fund to include stocks. None of the changes would protect someone who begins benefits earlier rather than later.

The third argument retirees might have is that they want to preserve their financial portfolio for as long as possible. If Social Security benefits are delayed, retirees will need to make larger withdrawals from their financial portfolio before benefits begin than they would if they begin benefits earlier. From our experience, some retirees express reluctance to this early-years reduction in the size of their financial portfolios. As previously noted, they should view their retirement resources as consisting of their financial portfolios plus Social Security benefits. Helping clients with this proper framework may help overcome this behavioral bias.

Summary

The major goal of this study is to estimate the additional longevity of the financial portfolio from delaying the beginning of Social Security. This is the first study to extend the withdrawal rate literature to include Social Security and taxes. We use a sophisticated model that integrates the Social Security claiming decision with many features of the U.S. tax system including progressive tax rates, standard deduction, personal exemptions, deduction amount for being 65 or older, and the taxation of Social Security benefits.

In Meyer and Reichenstein (2010) and Reichenstein and Meyer (2011), we argue that retirees should consider two criteria when selecting a Social Security claiming strategy. First, what claiming strategy would maximize cumulative lifetime benefits if the single individual lives to his or her precise life expectancy or each partner in a couple lives to his or her life expectancy? Second, what claiming strategy would minimize the longevity risk of the financial portfolio? The best strategy for a specific individual or couple depends on the trade-off the specific individual or couple places on these two criteria. However, in order to assess this trade-off, it is important for retirees to know how their starting date for Social Security benefits would likely affect their portfolio’s longevity. Some retirees may strongly suspect that they will live a short life, in which case they may not be concerned with portfolio longevity. But for many retirees, longevity risk is a major concern. The estimates in this study are designed for such retirees.

This study provides estimates of how delaying Social Security benefits would affect the longevity of a single individual’s portfolio. Intuitively, if a retiree selects a Social Security claiming strategy that provides more real lifetime benefits, his or her financial portfolio will last longer. Initially, we assume a retiree has a PIA of $1,500, a 30-year planning horizon, and earns a constant annual real return of 1.22 percent, the real return consistent with the 4 percent rule. We then estimate how delaying the beginning of Social Security benefits from age 62 to 64, 66, 68, and 70 would affect the longevity of the retiree’s financial portfolio for various levels of wealth. We vary his or her level of financial wealth from $200,000 to $1.5 million. We then repeat the analysis using a 25-year planning horizon. Separately, we consider a highly paid retiree with a PIA of $2,400 with financial wealth levels of $500,000 to $3 million. In addition, we examine the sensitivities of the estimates of additional portfolio longevity to the assumed inflation rate and real return.

We show that in some cases, delaying benefits can add more than 10 years of longevity. Assuming the retiree has a long life expectancy, the retiree could extend the longevity of his or her financial portfolio by delaying the starting date of Social Security benefits. Furthermore, the additional longevity from delaying Social Security decreases as the wealth level increases. So, less-wealthy clients concerned with longevity risk should be especially interested in delaying Social Security benefits. In addition, by delaying the start of Social Security benefits, the single retiree can increase his or her real spending level and still have the portfolio last 30 years. We also explain that one benefit of delaying Social Security benefits is that it can reduce the taxable portion of those benefits.

Endnotes

- For recent reviews of this literature, see Cooley, Hubbard, and Walz (2011); Jennings, Horan, and Reichenstein (2010); and Jennings et al. (2011).

- Consistent with the 4 percent rule, if the real rate is 1.22 percent, someone with $100 could withdraw $4 the first year and an inflation-adjusted equivalent amount each year, and the portfolio will be exhausted after 30 years. In Excel, =PMT(1.22 percent, 30, –100) = $4.

- To be precise, the $36,150 is the highest annual real spending level in $50 increments that would provide funds for 30 full years. This portfolio would have minimal funds remaining after 30 years, at the beginning of 2041.

- The model assumes the 2011 tax structure will remain for the next 30 years. Although this is obviously a questionable assumption, it allows us to consider the effect of delaying Social Security benefits while holding everything else constant. The model assumes inflation is 2.5 percent per year. Federal tax brackets, standard deduction amount, personal exemption deduction, and deduction amount for being 65 or older are indexed for inflation. The taxpayer was born December 2, 1948, and is assumed to live in an income-tax-free state. The model considers the taxation of Social Security benefits and assumes the threshold provisional income levels of $25,000 and $34,000 do not increase with inflation. It also considers required minimum distributions. The retiree takes the standard deduction. All wealth is held in a 401(k) or similar tax-deferred account. Withdrawals from the financial portfolio occur at the end of the year. The investments earn 3.75 percent per year, as explained in the text. The results are based on a proprietary model developed by Retiree Income Inc.

- This assumes an FRA of 66. If Social Security benefits begin at ages 62 through 70, benefit levels when expressed as a percentage of PIA are 75 percent, 80 percent, 86.67 percent, 93.33 percent, 100 percent, 108 percent, 116 percent, 124 percent, and 132 percent, respectively. The lowest percentage increase is 6.45 percent between ages 69 and 70, and the 8.34 percent increase occurs between ages 63 and 64.

- For someone with a PIA of $1,500 who lives to age 92, cumulative real benefits total $405,000 if benefits begin at age 62 ($1,125 per month x 12 months x 30 years), and $522,720 if benefits begin at 70 ($1,980 per month x 12 months x 22 years). And ($522,720/$405,000) – 1 = 0.291.

- For someone with a PIA of $1,500 who lives to age 92, cumulative real benefits total $405,000 if benefits begin at age 62 ($1,125 per month x 12 months x 30 year) and $436,800 if benefits begin at 64 ($1,300 per month x 12 months x 28 year). And ($436,800/$405,000)½ – 1 = 0.0385.

- These real rates of return are usually higher than the 3 percent embedded in the SSA’s reductions in benefits for beginning benefits before FRA and delayed retirement credits for delaying benefits until after FRA, because we assume a 30-year planning horizon, whereas SSA assumes an average life expectancy of about 84.

- A study by VanDerhei and Copeland (2010) for the Employee Benefit Research Institute concludes that almost half of Americans will not be able to cover their basic needs in retirement. Ernst & Young (2008) concludes that three in five retirees will outlive their financial assets if they maintain their current standard of living.

- This study assumes the retiree has all his financial wealth in a 401(k) or other tax-deferred account. Because many investors hold most of their financial assets in tax-deferred accounts, this assumption fits many retirees. However, the results would vary if the retiree had substantial funds in other savings vehicles such as a Roth IRA or taxable account. In particular, withdrawals in retirement from a Roth IRA do not affect taxable income, and withdrawals from taxable accounts may not affect taxable income.

- This approximation is not precise because Social Security benefits rise with inflation, and it ignores the retiree’s income taxes.

- Another advantage of delaying Social Security benefits is it tends to increase withdrawals from tax-deferred accounts before age 65 and thus decrease taxable income at age 65 and older. This may reduce the size of Medicare Part B premiums.

References

Congressional Budget Office. 2010. Social Security Policy Options (July). 28.

Cooley, Philip L., Carl M. Hubbard, and Daniel T. Walz. 2011. “Portfolio Success Rates: Where to Draw the Line.” Journal of Financial Planning 24, 4 (April).

Ernst & Young LLP. 2008. Retirement Vulnerability of New Retirees: The Likelihood of Outliving Their Assets. Americans for Secure Retirement (July).

Jennings, William W., Stephen M. Horan, and William Reichenstein. 2010. “Private Wealth Management: A Review.” Research Foundation of CFA Institute (Summer). www.cfapubs.org/doi/pdf/10.2470/rflr.v5.n1.1.

Jennings, William W., Stephen M. Horan, William Reichenstein, and Jean L.P. Brunel. 2011. “Perspectives from the Literature of Private Wealth Management.” Journal of Wealth Management 14, 1 (Summer): 8–40.

Meyer, William, and William Reichenstein. 2010. “Social Security: When to Start Benefits and How to Minimize Longevity Risk.” Journal of Financial Planning 23, 3: 49–59.

Reichenstein, William, and William Meyer. 2011. Social Security Strategies. Self-published.

Sass, Stephen A., Alicia H. Munnell, and Andrew Eschtruth. 2009a. The Social Security Claiming Guide. Center for Retirement Research, Boston College.

Sass, Stephen A., Alicia H. Munnell, and Andrew Eschtruth. 2009b. The Social Security Fix-It Book. Center for Retirement Research, Boston College.

VanDerhei, Jack, and Craig Copeland. 2010. “The EBRI Retirement Readiness Rating: Retirement Income Preparation and Future Prospects.” Issue Brief, Employee Benefit Research Institute (July).