Journal of Financial Planning: October 2025

NOTE: Please be aware that the audio version, created with Amazon Polly, may contain mispronunciations.

Executive Summary

- Sustainability has increasingly become a core focus for investors around the world, leading to the rapid growth of environmental, social, and governance (ESG) investing as a distinct investment strategy.

- As ESG investing has gained prominence, the traditional definition and expectations of fiduciary responsibility among financial advisers have evolved and become more complex.

- This study investigates how financial advisers are navigating these shifts in their fiduciary roles through a series of semi-structured interviews with practicing advisers.

- A thematic coding analysis of the interviews identified five key findings regarding advisers’ experiences and perspectives:

- Financial advisers consistently go above and beyond the legal requirements of a fiduciary.

- There is little to no demand for ESG investments from individual investors.

- Advisers express significant skepticism about the quality, consistency, and transparency of ESG metrics, citing concerns about greenwashing and data reliability.

- Offering ESG investment options to clients is not perceived as conflicting with fiduciary duty; however, advisers believe that being legally mandated to recommend ESG products would undermine their professional judgment.

- Advisers voiced considerable concern about the pace and direction of regulatory changes, fearing increased compliance burdens and potential constraints on client-centered advising.

Dr. Haley Burton is an assistant professor of finance at Lubbock Christian University, where she teaches courses in corporate finance, investments, and financial analysis. She holds a Ph.D. in business administration (financial management) from National University (CA), an M.S. in finance and economics, and bachelor’s degrees in finance and accounting.

Dr. Josh Sauerwein is a CPA and professor of accounting at Lubbock Christian University. He specializes in teaching intermediate accounting, accounting ethics, and tax research. Josh earned his D.B.A. in accounting through Anderson University (IN), an M.B.A. from Emporia State University (KS) and a bachelor’s in accounting, finance, and management from Tabor College (KS).

NOTE: Click on the images below for PDF versions.

JOIN THE DISCUSSION: Discuss this article with fellow FPA Members through FPA's Knowledge Circles.

FEEDBACK: If you have any questions or comments on this article, please contact the editor HERE.

Environmental, social, and governance (ESG) investing has been a growing source of controversy in the financial advising world. In January 2025, Judge Reed O’Connor of the U.S. District Court for the Northern District of Texas ruled in Spence v. American Airlines, Inc. that the plan administrators breached their fiduciary duty by pursuing “non-financial and non-pecuniary ESG policy goals.”1 More specifically, O’Connor determined that the administrators did breach their duty of loyalty, but not their duty of prudence. In his opinion, he wrote, “simply describing an ESG consideration as a material financial consideration is not enough.”2 Doing so leaves the door open to qualify anything as a financial interest. This ruling provided needed clarity to plan administrators and could have potential impacts on the fiduciary approach of financial planners and advisers.

As investors across the globe have identified sustainability as one of their investing goals, this has spurred the growth of ESG investing. However, with the rise of ESG investing, the definition of a fiduciary has morphed and changed. Further, the role of financial advisers, acting as fiduciaries, has been changed to accommodate investing goals that move beyond mere pecuniary benefits and into goals that attempt to marry a client’s value system with their investing goals. While values-based investing (also known as impact investing and sustainability investing) is not a new concept, ESG investing appears to be much more politically contentious than any prior versions of it. This puts financial advisers in awkward positions as they seek to fulfill their professional responsibilities while still caring for clients and seeking their best interests.

Therefore, this study investigated how financial advisers are navigating their changing roles as fiduciaries due to the rise of ESG investing. Additionally, it seeks to gather information on an adviser’s approach to screening, detecting greenwashing, and making a recommendation for an ESG investment. Finally, it investigates the demand from individual investors for ESG products.

The results of this study have implications for financial planners and advisers. Primarily, it offers a unique view into the life of a financial adviser and how they approach their fiduciary duty in politically divisive times by keeping a keen focus on their clients’ best interests. Second, it highlights the concerns of advisers as they seek to make investment recommendations. Finally, this study reveals further evidence of minimal demand for ESG products among retail clients.

Literature Review

Investor Demand

There appears to be a strong investor demand for ESG initiatives and ESG-related products, as an increasing number of shareholders are urging companies to adopt policies that promote ESG goals (Tucker III and Jones 2020). In response, companies have been voluntarily including ESG metrics in their annual reports for over a decade. As of 2022, 80 percent of the 100 largest companies across 52 countries provided metrics on sustainability (Garst, Maas, and Suijs 2022). However, until recently, companies could pick and choose which metrics to measure and report. In response, the SEC issued rules to “enhance and standardize climate-related disclosures” for large public companies (Securities and Exchange Commission 2024).

This demand appears to be consistent across both institutional and retail investors. The Forum for Sustainable and Responsible Investing reported in its 2022 Report on U.S. Sustainable Investing Trends that $7.6 trillion of U.S.-domiciled assets were placed in investments meeting ESG criteria, with climate change and carbon emissions ranking as top concerns among institutional investors (Sustainable Investment Forum 2022). While this accounts for a sizable amount of invested funds, it is a decrease from the $11.6 trillion invested in ESG criteria in 2018.

In a 2022 study of 545 institutional investors, The Capital Group found that 26 percent considered ESG central to their investing approach. When including investors who either accept ESG principles or view them as meeting compliance goals, a total of 89 percent use an ESG approach to investing (Capital Group 2022). While there is clear demand from institutional investors, it does appear that demand has softened over the last two to three years.

Individual investors also appear to have become more socially conscious regarding their investment alternatives. In an effort to merge their personal values and investing strategies, demand for ESG-related products has increased. In a 2021 survey, Boston Private found that high-net-worth investors exhibited increased demand for investments that prioritized issues related to ESG, like climate change and sustainability (Boston Private 2021). Some have found that demand for ESG among Gen Z and millennials is especially pronounced (Hopkins and Limón 2022). While demand for ESG across all investor types has increased in the last decade, more is known about institutional investors than individual investors. Further, research conducted among individual investors has surveyed the investors themselves, which may increase social desirability bias. This study investigates demand among individual investors as experienced by financial advisers. Therefore, this study asked the following questions of financial advisers:

A. How many of your clients have asked for ESG products?

B. Have you experienced an increasing demand for ESG products from your clients?

C. How many of your clients have asked to not be a part of ESG products?

Changing Nature of Fiduciary

Financial advisers must adhere to the legal requirements of a fiduciary for many, if not all, of their clients. These requirements come from a broad array of regulators that include the Securities and Exchange Commission (SEC), the Department of Labor (DOL), and Financial Industry Regulatory Authority (FINRA). There are three pillars to the fiduciary duty: the duty of loyalty, the duty of prudence, and the duty of care. However, over the last five years, the definition of all three pillars has shifted. Many of these shifts have come as a result of the rise of ESG investing.

In 2021, the DOL passed the ESG rule that relaxed the duty of prudence and loyalty in the common definition of fiduciary to allow fund managers to consider ESG issues for investments and shareholder rights decisions (Kerber 2023). While fiduciaries are not required to consider ESG factors, they are allowed to make this part of a prudent decision. The U.S. Congress immediately responded by passing a resolution to contest this rule.

In 2020, the SEC passed Regulation Best Interest (BI), which applies to all financial advisers making investment recommendations to retail investors. Prior to this regulation, in many scenarios, advisers only needed to meet a suitability standard for their recommendations. Many suggested the suitability standard was insufficient to protect investors, and advisers should always act in the best interest of their clients (Rubin 2015). Therefore, this regulation broadened the definition of what is considered a recommendation and raised the bar on the duty of care an adviser must practice.

The duty of loyalty demands that the adviser be solely directed by the interest of the client, even if it conflicts with their own personal views or those of a third party. With rising global pressure on investors to pursue ESG goals, financial advisers are increasingly expected to discern their clients’ priorities while assessing the influence of outside parties. The duty of prudence demands that advisers pursue investments with superior returns regardless of negative externalities. Some have contended that ESG investing with collateral benefits (not strictly financial benefits) conflicts with this duty, putting advisers in an awkward position (Schazenbach and Sitkoff 2020). Not only that, but it also exposes fiduciaries to greater legal risks if investors or beneficiaries find evidence that returns on ESG investments are not maximized.

The arguments over fiduciary duty have largely played out over political lines. Since the passage of the DOL resolution, at least 20 states have proposed or passed anti-ESG resolutions regarding their public employee retirement plans. In contrast, at least 15 states have proposed or issued resolutions further clearing the path for fiduciaries of public employee retirement plans to invest in ESG (Malone, Holland, and Houston 2024). In 2023, attorneys general of 21 states published an open letter giving a strong warning to asset managers who pursued ESG investments, claiming their cozy relationships with climate-related organizations and investment time horizons conflicted with their fiduciary duties (Kerber 2023). Financial advisers are thus left in a tenuous state as they seek to help their clients. Therefore, this study asked the following questions of financial advisers:

A. Do you owe a fiduciary duty to all your clients?

B. How has your role as a fiduciary changed in the last five years?

C. Do you think recommending ESG products conflicts with your fiduciary duty?

ESG Recommendations

With increasing investor demand, evolving definitions of fiduciary duty, and deep political divides over ESG, advisers’ recommendations may be fraught with ambiguity and risk. Advisers who manage ERISA plans must meet a fiduciary standard in their recommendations, which historically has meant they need to maximize returns for a given level of risk. Conversely, advisers who make recommendations to retail clients can be paid either by commission or may charge a set fee over a length of time to manage a client’s portfolio. Client accounts that are strictly commission-based do not require an adviser to adhere to the legal definition of a fiduciary, like with fee-based accounts, but rather meet a suitability standard. The suitability standard is less stringent than the requirements of a fiduciary but still requires an adviser to have a reasonable basis for an investment recommendation suitable for the client’s needs. Thus, whether an adviser is a fiduciary over a plan that falls under ERISA or making recommendations to a retail client, they must carefully navigate their professional responsibilities.

As stated above, part of the fiduciary duty is the duty of prudence. Applying prudence in a recommendation requires the adviser to evaluate how an investment has performed in the past, the fees being charged, and the alternatives that may provide superior returns. Even though the DOL broadened the definition of fiduciary to include ESG investments, it still states that “a fiduciary may not . . . accept expected reduced returns or greater risks” for collateral benefits (U.S. Department of Labor 2021). Therefore, an adviser must find evidence that ESG provides commensurate returns with other alternatives.

Because ESG investing is still relatively new, it is often difficult to observe long-term trends and performance through different market cycles. Further, it is difficult to determine if returns are the result of ESG strategies or part of a broader economic trend. As some have suggested, it is “hard to know whether a particular stock would have done well, better, or worse in a given year if it had used electricity from coal as opposed to using electricity from wind” (Cyr 2023, 13). Regarding returns, some have found that companies who provide greater ESG disclosures have a wider dispersion of ESG ratings (provided by third-party rating agencies), which can lead to greater confusion for advisers as they interpret ESG information. Further, they found that greater disagreement on ESG ratings was correlated with higher return volatility and price movements, which may run counter to the duty of prudence (Christensen, Serafeim, and Sikochi 2022). Others have compared ESG portfolios to non-ESG portfolios and found that ESG portfolios, while they may have similar returns, have more volatility making them less efficient alternatives (Makridis and Simaan 2023). The lack of long-term data, unknown causal effects of ESG strategies on profitability, and increased volatility of ESG investments again puts financial advisers in shaky positions when making ESG recommendations.

Not only must advisers determine if the returns of ESG investments are adequate, they must filter through a variety of ESG scores and information that is still largely provided voluntarily by companies. Some have noted that the mass proliferation of ESG rating agencies, an ever-increasing number of global organizations who want to weigh in on measurement standards, and a lack of conclusive frameworks for ESG reporting by regulators has only served to frustrate and confuse investors (Kraten 2023). Only recently has the SEC given guidance on ESG reporting, asking large filers to provide information on their Scope 1 and 2 greenhouse gas emissions (Securities and Exchange Commission 2024). Given the limited frameworks for reporting ESG data, companies provide very different metrics, which makes comparison difficult. In a random sample of 50 large companies from the Fortune 500 list, researchers collected metrics on employee health and safety (part of the Social category) and found more than 20 different metrics with distinct terminologies (Kotsantonis and Serafeim 2019). Trying to read and interpret ESG metrics and scores could be a confusing task, even for the most seasoned of financial advisers.

Finally, adding more complexity to the recommendation process, advisers must not only understand the client’s goals regarding ESG investments, but also assess their knowledge of the ESG landscape. Part of the duty of care is understanding the client’s financial objectives and circumstances. When clients request ESG investments, advisers cannot simply take their request at face value. They must understand why the clients are asking for this, the specific parts of ESG they want to pursue, and their time horizon. Further, they must understand if they are exclusionary investors who would refuse to hold investments that conflict with their values or investors who would be more neutral in their approach. In a study of average retail investors, researchers found that sustainable investors gave up financial wealth to experience positive emotions and would pay a premium for perceived impact rather than real impact (Heeb et al. 2023). Other studies have shown that the behavior of retail investors who prioritize ESG products is very similar to the behavior of misinformed investors (Fama and French 2007). Therefore, while financial advisers play a significant role in screening potential ESG investments, they may also play a significant role in helping clients understand their own investing goals and how ESG may or may not be consistent with those goals.

Given all of these complex factors, the recommendation process for clients pursuing ESG goals can be complicated. Therefore, this study asked the following questions of financial advisers:

A. How are you screening for potential ESG

investments?

B. How do you interpret ESG scores?

C. How do you filter through a client’s request

for ESG?

Greenwashing

Knowing that investor demand for ESG is high, ESG investments might sell for premiums, and retail investors may lack the information or sophistication to determine if investments are living up to their ESG claims—companies might be incentivized to overstate their ESG impact. Further, due to the lack of regulatory guidance and confusion surrounding what to measure and how to measure items in the ESG space, some firms may be engaging in various forms of greenwashing. These efforts can occur through blatant deception, obfuscation, or diversion.

In a study of ESG-branded exchange-traded funds (ETFs), researchers found that over 25 percent of the ETFs they investigated had a significant proportion of their total assets invested in stocks with high or severe ESG ratings, potentially indicating their ESG brand was disingenuous (Rompotis 2023). In a study of the 100 Financial Times Stock Exchange (FTSE), researchers found a majority of companies reporting ESG measurements in their annual investor reports were either disingenuous regarding the level of audit assurance obtained on such measurements, cryptic about which measurements were actually audited, or intentionally vague about how the ESG information was collected or audited (Carmichael et al. 2023). Finally, in a study of European investment funds that claimed sustainability strategies, researchers found that over 50 percent made explicit claims of environmental impact that were completely unsubstantiated (Heeb et al. 2023). As financial advisers provide recommendations of ESG products, they should have mechanisms for detecting greenwashing. Therefore, this study asked the following questions of financial advisers:

A. How concerned are you with greenwashing?

B. What mechanisms do you have in place to detect greenwashing?

Methodology

Participants

This study answered the aforementioned questions by conducting semi-structured interviews with financial advisers. The sample of advisers was a purposive sample. A total of nine advisers accepted the invitation for an interview and two declined. The advisers resided in states that represented differing approaches to ESG investing. There were six advisers from anti-ESG states (Texas, Kansas, South Carolina, and Indiana) and three advisers from pro-ESG states (Oregon, Colorado, and Virginia).

All the advisers were fiduciaries to their clients, were in a position to accept and reject clientele, and had significant interaction with their clients. Seven were males and two were females. They had an average of 25 years of experience in financial advising, with all advisers having more than 15 years of experience. They were primarily fee-based advisers, while the remaining advisers had a broader mix of fee-based and commission-based clients. All advisers held their series 6 and 7 securities licenses and four had their CERTIFIED FINANCIAL PLANNER® (CFP®) designation.

Design

This was a qualitative, exploratory, single case study design conducted in a semi-structured interview format. All participants gave informed consent prior to being interviewed. All interviews were conducted by two researchers, interviews averaged one hour in length, and were conducted over a period of two months during the spring of 2024. The questions listed above were asked of all participants, with additional follow-up questions to clarify responses where necessary. After the interview was completed, emails were sent to all participants inviting them to provide clarifications or additional responses over email.

Analysis

Once the interviews were completed, the interviews were transcribed and sent back to the participants to ensure accuracy of the transcription. After transcription and participant checks, the researchers inductively coded the transcriptions and identified an initial list of themes. Using the start list of themes, the interviewers went through a second round of coding to identify observations or quotes that supported the themes. After a thorough analysis of each interview, five major themes emerged across all interviews, resulting in data saturation.

Findings

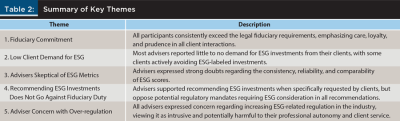

Table 2 outlines the five main themes that emerged from the inductive coding analysis process mentioned above.

Theme 1

The most prominent theme that emerged across all interviews was that advisers take their fiduciary role seriously, often exceeding the legal requirements expected of a fiduciary. As stated previously, the three pillars to the fiduciary duty are the duty of loyalty, duty of prudence, and duty of care. This legal responsibility simply means a fiduciary should only make decisions in the best interest of the client. This legal requirement applies primarily to CERTIFIED FINANCIAL PLANNER® professionals and any management of a fee-based (versus commission-based) client account. However, when participants were asked whether they believed they owed a fiduciary responsibility to all clients, regardless of the legal requirement, the responses were a resounding “yes.” One participant stated, “I don’t see how you can’t be a fiduciary to all your clients.” Another participant mentioned that when it comes to their clients, regardless of their situation, “do the right thing, own it, keep others first.”

Another adviser mentioned that a fiduciary not only looks out for the interests of their clients, but creates a personal connection with each client, stating, “you want to protect the clients’ assets, you want to protect the clients from themselves, but you also want to protect the clients for future generations . . . it’s a very personal connection.”

Theme 2

The second theme that emerged from the interviews was that there seems to be little to no demand for ESG-specific investments from individual investors. Most advisers mentioned an attitude of indifference or ignorance from their clients regarding ESG investments. As one adviser stated, “It’s not part of their vernacular. It’s not important to them. It’s not on their radar.” Another adviser states, “I bet the term ESG has been said in this conference room outside of this meeting probably 10 times in four years.”

On the other hand, two advisers specifically mentioned a noticeable hesitance from their clients to invest in any investment product labeled as ESG. As one adviser mentions, “I’ve had multiple clients say I want nothing sponsored by BlackRock because of how they approach things” (in regard to BlackRock divesting from energy companies in 2023–2024). Most notably, an adviser from Oregon, which is a staunchly pro-ESG state as noted previously, made the strongest statement on this subject, noting that “possibly somewhere between 30–40 percent, maybe even up to 50 percent [of my client base] have said I want nothing to do with the ESG.”

Theme 3

The next theme revolves around each adviser’s perception of ESG investment products. Without question, every adviser interviewed mentioned a high level of skepticism toward ESG metrics (including the reliability and accuracy of such measurements), ESG-branded products, and developing regulations around ESG. This theme centers on the measurements and metrics that result in an ESG score for a specific company, fund, or ETF. For example, as of 2024, the Walt Disney Company had an ESG score of 15 (out of 40+, with a higher score indicating a higher ESG risk) according to Morningstar Sustainalytics, a score of 68 (out of 100) according to AltIndex, and an Impact score of 57 (out of 100) according to Ethos Impact Inc. When advisers were asked about the source and reliability of these ESG or impact scores, the responses were similar. One adviser simply states that “none of the ESG metrics agree,” while another adviser questions the underlying measurement, asking, “How are you going to (measure it)? What’s the measurement? Who measures it?”

Many of the responses in this area circled back to the advisers’ fiduciary responsibility to maximize returns in accordance with the clients’ risk tolerance, and choose investments that have reliable, proven track records. When it comes down to managing a portfolio, one adviser states, “you can’t manage something if you can’t measure something, and you’re telling me we’re 15 years into something [ESG] that we can’t define, and yet we’re going to use that as a criteria to make a financial decision on.” As another adviser explained, “It’s all a bunch of theoretical things that I can’t measure. But it makes you feel good. Things that make you feel good don’t really correlate to reality.”

Theme 4

From this point, we continued to ask questions related to a situation where a client may specifically request ESG products to be included in their portfolio. While the scenario was more hypothetical based on previous themes and responses, each adviser was asked what the process would look like and if providing a recommendation on an ESG investment would align with their fiduciary duty. Across all interviews, the consensus was that making an ESG recommendation would not be counter to their fiduciary duty, especially if the adviser felt like the client was well-informed and educated on such an investment, but being mandated to consider or offer ESG products from a regulatory body would cross the line.

As one adviser states, in their fiduciary capacity, “if the client wants [ESG], then they should have it.” However, every adviser expressed concern at the attempt to incorporate ESG into the definition of fiduciary, with one stating that “for someone else to put the pressure on us to only offer ESG . . . that’s really crossing the line,” or another saying, “mandating ESG is against my fiduciary duty.” One participant mentioned the fundamental role of an adviser should not include politically charged topics such as ESG, stating that “investing is our lane. We’re going to invest your money. If we switch to the ESG lane, that’s activism. And I don’t think that’s our job.” Lastly, another adviser mentioned the inclusion of ESG into the definition of fiduciary is counterintuitive, saying “it (ESG) being dictated is a problem. I mean, if you’re a fiduciary and you’re being dictated to, it’s kind of hard to be a fiduciary at that point. They counteract each other.”

Theme 5

The last theme is a continuation of theme 4, where all advisers expressed concern about the increasing or over-regulation in the industry. When asked about the current state of ESG regulation and investor sentiment in this area, one adviser stated, “I think there’s a blowback. People are tired of it. People are tired of the heavy hand of Washington pushing their thought values on everybody, you know . . . Don’t tell me what I need to do.” On the question of the role of regulatory bodies such as the SEC and Department of Labor, the responses were resolute: “The SEC has zero business regulating ESG metrics,” and “The Department of Labor shouldn’t be giving guidance on fiduciary duty.”

Discussion

The most significant finding of this study is the demand, or lack thereof, for ESG products by retail investors. This was surprising because, as stated previously, multiple studies have found a sizable increase in investor demand for ESG products. However, the results of this study suggest that claim may not be true in all parts of the United States. Across six different states on both sides of the political divide, this study found little to no demand for ESG products from retail investors. There may be a number of explanations for this discrepancy.

First, retail investors, especially those with a smaller amount of assets, may not be as apprised of ESG matters as institutional investors. Their investment time horizons may be shorter given that their goals are saving for specific events (college, weddings, etc.) and, therefore, their focus on pecuniary benefits may override other considerations. Additionally, in at least half of the states, anything ESG or climate-related is viewed with a wary eye. Those attitudes might be carrying over into investment decisions. Lastly, it may be that actual demand for ESG products has been overstated in an attempt to market these products. Whatever the case, future research could address investor demand for ESG products by investigating generational differences, regional differences, and political differences.

Interestingly, financial advisers were also highly skeptical of ESG products, metrics, and regulations. This theme was highly consistent across all interviews. The dissemination of ESG metrics in annual reports has been largely unregulated in the United States until recently. As stated before, a number of companies have taken advantage of this and engaged in greenwashing efforts. Financial advisers were very attuned to this reality. Even though their proprietary software provided ESG scores, they often discounted them or did not include them in their recommendation process, unless they were specifically asked to do so. This hesitancy might be the result of a number of factors.

First, the deepening political divide on ESG related matters might be causing skepticism. Advisers are experts in capital markets and their proper functioning. Government interference is often seen as heavy-handed and disruptive to market forces. Even though regulators have been late in offering guidance, the apparent demand for ESG, as espoused by many, seemed artificial to these advisers and, possibly, disruptive to proper market forces. Second, the lack of long-term data correlating ESG scores to stock returns might be causing advisers to discount them until there is further proof of superior returns because of a company’s focus on ESG matters. Third, most of the advisers mentioned the increasingly heavy hand of regulations regarding ESG. When these matters are forced, advisers feel like their roles as experts are drawn into question. This undermines their profession. Finally, this skepticism could be the result of an adviser’s personal views on the veracity of the science behind climate change. Whatever the source, skepticism on the veracity of ESG metrics was pronounced, which calls into question the decision usefulness of these metrics. Though United States regulators have started offering guidance on ESG metrics, it will be interesting to see whether advisers view them as useful in the investment recommendation process.

While advisers remained highly skeptical of ESG, they did not believe recommending an ESG product conflicted with their fiduciary duty. Over and over, advisers spoke poignantly about the seriousness with which they approach their fiduciary duty, even when they were not legally required to act in such a manner. We expected to hear that the deep skepticism toward ESG metrics and products would cause advisers to steer their clients away from such products because it lacked loyalty or prudence. However, this was not the case. Their care for their clients, desire to fulfill their wishes, and ability to listen and counsel their clients was truly impressive. They embodied what it means to have someone else’s best interest in mind.

Additionally, these advisers felt a strong duty to fully inform their clients regarding ESG matters in order to help them make a good decision. For the few clients who desired ESG products, the advisers took time to understand the client’s goals, how their values informed their investment ideals, unearthed any misinformation the client had regarding ESG, and walked them through a plan for identifying appropriate products. Because many of the advisers lacked robust information on suitable ESG products (due to lack of client demand), they often helped their clients identify other advisers who were more knowledgeable about these products. Educating their clients on effective investing strategies was important to all advisers.

While the financial advising profession includes individuals whose unethical practices have prompted a wave of new regulations, it was clear these advisers exemplified a higher standard. They took their roles very seriously, thought deeply about their fiduciary responsibilities, worked hard to be true ambassadors of the profession, and felt the weight of acting in the client’s best interests. Their approach to ESG products and investing was thoughtful, well-articulated, and rational.

Limitations and Future Research

Given this study used a qualitative design with limited participants, generalizability is difficult. Therefore, future research could broaden the sample size, with specific attention given to interviewing advisers who have less experience in the profession. Younger advisers, as they build a book of business, have differing incentives that may alter their recommendations and enactment of fiduciary duties. Further, interviewing advisers who are incentivized to sell ESG products would also add veracity to the results. Additionally, future research could seek to understand how newly regulated ESG metrics are perceived or are being used by advisers in the recommendation process. This study calls into question the usefulness of ESG metrics in the investing process. Future research might attempt to understand why the metrics are not being used, under what circumstances they would be used, and what importance they might be given. Future studies such as these would improve the generalizability of findings and contribute to the development of more nuanced frameworks for understanding fiduciary responsibility in an ever-changing investment environment.

Conclusion

While the prevalence of ESG investing continues to find its way to the front page, the landscape of ESG investing continues to be fraught with pitfalls, opaqueness, and misinformation. This makes the role of a financial adviser much more difficult. Identifying quality information and using it in the recommendation process can be challenging. More importantly, fulfilling the fiduciary duty is easier said than done. This study investigated the ever-changing terrain of financial advisers and their approach to ESG investing as it relates to their fiduciary duty.

This study found evidence that the demand for ESG products from retail investors is very minimal. Additionally, advisers hold a strong skepticism toward ESG products and metrics because of perceived greenwashing. Finally, advisers do not believe that recommending ESG products, in spite of their skepticism about quality metrics, conflicts with their fiduciary duty. Most notably, advisers approach their fiduciary responsibilities as almost a sacred duty. They enact this duty in all client scenarios, regardless of whether they are legally required to do so, primarily out of care and concern for their clients.

The fiduciary duty is a bedrock feature of the financial advising profession. Navigating its changing definition and complexities is a challenge that requires great skill and judgment. ESG investing has added a layer of complexity to this demanding exercise. In spite of this, the advisers interviewed rose to the occasion by putting the client’s best interest at the center of their recommendations. Though skeptical of ESG metrics and claims, they seek to educate their clients, provide products and strategies that match their values, and ensure the long-term success of their portfolios. Their nuanced and thoughtful approaches epitomized the duty of loyalty and prudence.

Citation

Burton, Haley, and Josh Sauerwein. 2025. “Navigating Fiduciary Duty in the Era of ESG Investing: Insights from Financial Advisers.” Journal of Financial Planning 38 (10): 78–90.

Endnotes

- Spence v. American Airlines, Inc. 4:23-cv-0552 N.D. Tex. 157 (2025). https://climatecasechart.com/case/spence-v-american-airlines-inc/.

- Spence, 4:23-cv-0552 N.D. Tex. at 157.

References

Boston Private. 2021. ESG Trends. Boston, MA: BostonPrivate.

Capital Group. 2022. ESG Global Study 2022. Los Angeles, CA: The Capital Group Companies, Inc.

Carmichael, Donna, Kazbi Soonawalla, and Judith C. Stroehle. 2023. “Sustainability Assurance as Greenwashing.” Stanford Social Innovation Review Winter 2023: 34–39. https://doi.org/10.48558/300B-AB57.

Christensen, Dane M., George Serafeim, and Anywhere Sikochi. 2022. “Why Is Corporate Virtue in the Eye of the Beholder? The Case of ESG Ratings.” The Accounting Review 97 (1): 147–175. https://doi.org/10.2308/TAR-2019-0506.

Cyr, J.S. 2023. “ESG Investments in Defined Contribution Plans.” Journal of Pension Benefits 30 (2): 11–14.

Fama, Eugene F., and Kenneth R. French. 2007. “Disagreement, Tastes, and Asset Prices.” Journal of Financial Economics 83 (3): 667–689. https://doi.org/10.1016/j.jfineco.2006.01.003.

Garst, Jilde, Karen Maas, and Jeroen Suijs. 2022. “Materiality Assessment Is an Art, Not a Science: Selecting ESG Topics for Sustainability Reports.” California Management Review 65 (1): 64–90. https://doi.org/10.1177/00081256221120692.

Heeb, F., Julian F. Kolbel, Falko Paetzold, and Stefan Zeisberger. 2023. “Do Investors Care About Impact?” The Review of Financial Studies 36 (5): 1737–1787. https://doi.org/10.1093/rfs/hhac066.

Hopkins, Jamie P., and Ana T. Limón. 2022. “The Investments of the Future Focus on Impact.” Journal of Financial Planning 35 (6): 68–71.

Kerber, Ross. 2023. “U.S. Republicans Challenge More Fund Managers on ESG.” Reuters. www.reuters.com/business/sustainable-business/us-republicans-widen-challenge-fund-managers-esg-2023-03-31/.

Kotsantonis, Sakis, and George Serafeim. 2019. “Four Things No One Will Tell You About ESG Data.” Journal of Applied Corporate Finance 31 (2): 50–58. https://doi.org/10.1111/jacf.12346.

Kraten, Michael. 2023. “Finding the Right ESG Framework: Which Standard Setters Should You Choose?” The CPA Journal 93 (7/8): 13–15.

Makridis, Christos, and M. Simaan. 2023, November 9 . “We Studied 235 Stocks—And Found That ESG Metrics Don’t Just Make a Portfolio Less Profitable, but Also Less Likely to Acheive Its Stated ESG Aims.” Fortune. https://fortune.com/2023/11/09/stocks-esg-metrics-portfolio-profitable-stated-esg-aims-makridis-simaan/.

Malone, Leslie, Emily Holland, and Casey Houston. 2024. “ESG Battlegrounds: How the States Are Shaping the Regulatory Landscape in the U.S.” Harvard Law School Forum on Corporate Governance. https://corpgov.law.harvard.edu/2023/03/11/esg-battlegrounds-how-the-states-are-shaping-the-regulatory-landscape-in-the-u-s/.

Rompotis, Gerasimos G. 2023. “Do ESG ETFs ‘Greenwash’? Evidence from the U.S. Market.” Journal of Impact and ESG Investing 3 (4): 49–63. DOI:10.3905/jesg.2023.1.070.

Rubin, Gayle. 2015. “Advisers and the Fiduciary Duty Debate.” Business and Society Review 120 (4): 519–548. https://doi.org/10.1111/basr.12073.

Schazenbach, Max M., and Robert H. Sitkoff. 2020. “ESG Investing: Theory, Evidence, and Fiduciary Principles.” Journal of Financial Planning 33 (10): 42–50. www.financialplanningassociation.org/article/journal/OCT20-esg-investing-theory-evidence-and-fiduciary-principles.

Securities and Exchange Commission. 2024. “SEC Adopts Rules to Enhance and Standardize Climate-Related Disclosures for Investors.” Press release. www.sec.gov/news/press-release/2024-31.

Sustainable Investment Forum. 2022. Report on U.S. Sustainable Investing Trends. Washington, DC: Sustainable Investment Forum.

Tucker III, James J., and Steve Jones. 2020. “Environmental, Social, and Governance Investing: Investor Demand, the Great Wealth Transfer, and Strategies for ESG Investing.” Journal of Financial Service Professionals 74 (3): 56–75.

U.S. Department of Labor. 2021, October 14. “Prudence and Loyalty in Selecting Plan Investments and Exercising Shareholder Rights.” Proposed rule. Federal register 86, no. 196: 57272–57303. www.federalregister.gov/documents/2021/10/14/2021-22263/prudence-and-loyalty-in-selecting-plan-investments-and-exercising-shareholder-rights