Journal of Financial Planning: July 2025

Michael B. Schoffman, CFP®, CDFA, CRPC, is a senior adviser with Schechter Investment Advisors (www.schechterwealth.com) with an extensive background in portfolio design and management and financial planning, working with high-net-worth executives, entrepreneurs, and retirees in several business markets such as real estate, aviation, and entertainment.

NOTE: Click on the image below for a PDF version.

JOIN THE DISCUSSION: Discuss this article with fellow FPA Members through FPA's Knowledge Circles.

FEEDBACK: If you have any questions or comments on this article, please contact the editor HERE.

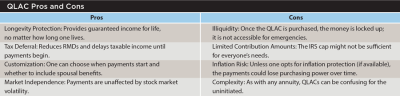

What are QLACs and why do they exist? The simple answer is longevity risk. Longevity risk is the chance that one lives longer than life expectancy in retirement and possibly outliving one’s retirement savings. While living to a ripe old age is a wonderful goal, funding an extended retirement can be a financial challenge. Using a qualified longevity annuity contract (QLAC) may be helpful to some investors.

Quick background: In 2014, the U.S. Treasury Department introduced QLACs as a specific type of deferred income annuity that can be purchased within certain types of retirement accounts, such as 401(k)s, 403(b)s, SEP IRAs, or IRAs. The goal was to help retirees manage longevity risk by providing a guaranteed income stream later in life. In short, QLACs exist to give peace of mind to retirees that they will not completely run out of money during their golden years.

Very specific rules for QLACs came from the 2019 SECURE Act legislation. The original maximum amount that could be invested into a QLAC was the lesser of $125,000 or 25 percent of the retirement account value. Two important changes took place in 2022 with the SECURE 2.0 Act. First, the limit of 25 percent has been removed and the upward limit is $210,000 in 2025. Second, there is a “return of premium” option on all QLACs, which allows a beneficiary to receive the purchase amount less any payouts. This option does affect the calculation of the payout from the contract.

What is especially notable about QLACs is that they allow clients to defer required minimum distributions (RMDs) from the portion of their retirement savings that they use to buy the contract. This can be a tax-efficient strategy with lower RMDs initially, thus reducing taxable ordinary income. Depending on other sources of retirement income, this could affect how much an individual pays for their Medicare Part B premium.

How Do QLACs Work?

A QLAC is purchased with funds from a qualified retirement account. The IRS has set limits on how much can be contributed to a QLAC. As mentioned, up to $210,000 of the tax deferred retirement account balance can be contributed. Married couples can each put $210,000 into a QLAC. The maximum amount does get indexed for inflation annually.

Unlike immediate annuities, where income starts flowing shortly after the purchase, a QLAC’s income payments are deferred to a future date. The annuitant gets to choose when the payments start, but they must begin no later than age 85. During the deferral period, the money invested in the contract is no longer subject to market risk, although control over how to invest it is lost. The insurance company is now taking the risk, and the contract at the time of purchase determines how the invested money will be paid back when the income stream starts.

Once the deferral period ends, the QLAC starts paying out a guaranteed income stream. This can provide a financial lifeline in later years when other sources of income might be running low. The payments, which are then taxable as ordinary income, are calculated based on factors like the amount invested, age when payments start, and the options selected (such as whether the payments will continue to a surviving spouse).

When a QLAC Might Make Sense

QLACs are not a one-size-fits-all solution, but they can be a valuable tool for some people. Here are five groups who might benefit:

- Those concerned about outliving their savings. If there is worry about outliving their retirement savings, a QLAC can provide a safety net. The guaranteed income stream ensures there will be a steady cash flow later in life, no matter how long one lives.

- People looking to reduce RMDs. If a client is nearing the age when required minimum distributions kick in (currently age 73 for most people) and the extra income isn’t needed right away, a QLAC could help. By using a portion of the retirement savings to purchase a QLAC, one can reduce the balance subject to RMDs and potentially lower one’s tax bill.

- Retirees without a pension. Clients who are heading into retirement without a pension might be relying heavily on Social Security and other personal savings. A QLAC can act as a private pension, providing predictable income later in life. This could be especially good for those who are not worried about leaving any money behind but want the guarantee they will not be left high and dry.

- Individuals who value financial certainty. Some people like to know exactly what their financial future will look like. For clients who prefer certainty over market risk, a QLAC’s guaranteed payments can offer peace of mind.

- Married couples planning for longevity. A QLAC can be structured to provide income for both spouses. If planning for the possibility that one or both spouses will live into their 80s, 90s, or beyond, this can be a smart way to ensure income lasts throughout both lifetimes.

Other Planning Considerations

Since QLACs provide lifetime income, they can be a way to hedge against other sources of income that might not be guaranteed in the future, like rental income or Social Security benefits, which could be cut as soon as 2033 unless Congress makes changes to the current system.

Individuals can also donate part or all the QLAC payment to charity via a qualified charitable distribution (QCD) if so inclined. If lifetime gifting is important then this could be a benefit.

QLACs can also be used to pay ongoing premiums for life insurance or other policies. Having a lifetime annuity payout to pay the premium means the policy stays in force and a potential tax-free death benefit for the beneficiary. Inherited IRA assets are not as tax efficient with the elimination of the stretch IRA.

Practical Example: How a QLAC Might Work in Real Life

You have a 65-year-old retiree client with $1 million in a traditional IRA. You decide to allocate $200,000 to a QLAC, with payments set to begin at age 80. Over the 15-year deferral period, the QLAC grows at a guaranteed rate. At age 80, the QLAC starts paying approximately $44,000 per year for the rest of the client’s life (single-life annuity). The amount of income the client can expect from the QLAC depends on annuity contract specifics.

There are several options for payouts, such as single life, joint life, or period certain. Some things to consider include:

- Payments are highest with a single-life annuity since the income stops with the death of the annuitant.

- Joint-life annuities pay until the death of the second annuitant.

- Period certain annuities guarantee a payout for a set period, like 10 or 20 years, even if the annuitants die before that period is over.

- If an investor wants to hedge against dying prematurely, then a cash refund option would ensure that their beneficiary would get the premium amount paid less the total of all income payments prior to death.

- Choosing the cash refund option would lower the monthly/yearly payout amount.

One could also consider laddering multiple QLAC contracts and purchasing one QLAC each year for several years. This approach is similar to dollar-cost averaging, which considers that annuity costs can fluctuate along with interest rates. Current interest rates are making today’s contract payouts more attractive than a few years ago.

There are several highly rated insurance companies that offer QLACs, and before choosing to buy one, you should do your due diligence on the carrier, their financial strength, and the offered payouts.

Final Thoughts

If considering a QLAC, it is important to evaluate whether it aligns with the client’s overall retirement plan. Here are some questions to consider and discuss with your clients:

- How much of the retirement savings should be allocated to a QLAC?

- When should payments start?

- What are the fees and costs associated with the QLAC?

- Are there inflation-adjusted payment options?

- How will this impact an estate plan?

Qualified longevity annuity contracts are designed to address one of the biggest fears retirees face—running out of money in their later years. QLACs are not right for everyone; however, they can be a useful tool for someone wanting to balance longevity protection with tax efficiency.

Read Next: “Navigating the Waters of IRMAA: A Comprehensive Guide for Financial Planners,” Al Kushner, January 2025