Journal of Financial Planning: April 2026

NOTE: Please be aware that the audio version, created with Amazon Polly, may contain mispronunciations.

Executive Summary

- Intercultural competence is transitioning from “optional” to “essential” in financial planning. Demographic shifts among asset holders, increasing globalization, and projected wealth transfers necessitate enhanced cross-cultural skills among practitioners. This paper examines cross-cultural differences and competency through the lens of Hofstede’s cultural dimensions theory and existing clinical research, aiming to identify and integrate key cultural differences while highlighting similarities within Western culture.

- Several relevant theories emerged in our research and serve as the foundation for this study. Hofstede’s theory consists of six dimensions, postulating that clients commonly fall within varying degrees of a dimension correlated with associated financial planning behaviors. Generational Cohort theory provided additional context for understanding the evolution of attitudes, values, and beliefs within cultural and generational frameworks. In our extensive literature review, we examined both cross-cultural similarities and techniques for bridging cultural differences.

- Our study indicates that merely acknowledging cultural differences is insufficient. Practitioners must identify and address their own implicit biases, ask clients about their cultural practices, and implement collaborative approaches to foster trust and build long-lasting relationships. We propose adapting the LEARN Model (Listen, Explore, Acknowledge, Respect, Nurture) and Zaretta Hammond’s Culture Tree for use in financial planning, creating a structured framework for cross-cultural communication and relationship development. This responsive approach enables clients to achieve financial goals that align with their cultural and personal values, while also allowing advisers to build a thriving practice.

Mo Buckner, M.B.A., is a Ph.D. student at Kansas State University, where she also earned a graduate certificate in financial therapy. Prior to this, she spent seven years in various roles in private wealth management. Her research interests include communication styles, culture and diversity, financial therapy, marriage and family structure, neurodiversity, socioeconomics, the Great Wealth Transfer, and how these variables will impact and reshape generations.

Matthew Brady, CFP®, RICP, is a senior wealth adviser at Mariner Wealth Advisors, LLC with 30 years of experience delivering comprehensive financial advice. He holds undergraduate degrees in history from Kansas State University and psychology from the University of Kansas and is currently completing a graduate certificate in financial therapy at Kansas State. His professional focus includes retirement planning, investment strategy, and the behavioral dimensions of client decision-making. Matt integrates research and practice to support client outcomes and advance the financial planning profession.

Jack McAulay is a recent graduate of Kansas State University’s CFP® Board-registered personal financial planning master’s program. He currently serves as an active-duty officer in the United States Army. Jack earned his undergraduate degree from East Carolina University, where he also received his military commission in 2020. Following his military service, he plans to leverage his leadership experience and graduate-level training to pursue his CFP® designation and provide comprehensive financial planning to a diverse clientele at Center Street Capital Advisors in Cary, North Carolina.

Marja Sweet, CFP®, is a partner at Oak Leaf Wealth Management and 307 Financial Services, serving clients around the country including Rhode Island and Wyoming where she focuses on financial planning for retirees. She holds a master’s degree in personal financial planning with graduate certificates in financial therapy and advanced planning from Kansas State University.

Meghaan R. Lurtz, Ph.D., is a professor of practice at Kansas State University.

NOTE: Click on the table below for a PDF version.

JOIN THE DISCUSSION: Discuss this article with fellow FPA Members through FPA's Knowledge Circles.

FEEDBACK: If you have any questions or comments on this article, please contact the editor HERE.

A recent eMoney survey found that 22 percent of American consumers were dissatisfied with their financial guidance, citing complexity and lack of personalization (Buhrmann 2023). Three factors that influence these categories are wealth transfer, globalization, and culture. The Great Wealth Transfer, which is projected to reach over $100 trillion by 2048, entails demographic shifts that mark a profound transition in U.S. wealth ownership (Horton 2024). This transition will likely bring new cultures and generations into financial planning offices.

Financial advisers aim to develop cross-cultural competencies to meet their clients’ increasingly diverse needs (Grubman and Jaffe 2016). This is important as cultural misalignment can lead to mistrust, poor communication, and disengagement from planning services (Perkins 2019). To address this pressing need, this paper draws on Hofstede’s (2024) six cultural dimensions and explores how values, communication, and trust shape the adviser–client relationship. By intentionally incorporating cultural nuance into their practice, financial planners can offer more inclusive and practical guidance to their diverse, evolving American and global client bases.

Literature Review

The Generations

Generational Cohort theory posits that people born within the same period tend to share core values and worldviews (Pokharel and Maharjan 2024). Yet culture complicates sweeping generalizations. In many Western cultures, adulthood is often associated with financial independence. Conversely, non-Western cultures typically see financial interdependence as a sign of strength and responsibility (Rubin et al. 2024). Despite members of a generational cohort experiencing the same events, their different cultural backgrounds may lead to unique financial roles and goals.

The Role of Cultural Competency in Professional Communication

Cultural competence is essential to financial planning and interpersonal professions. While basic needs like food and shelter are universal necessities, financial values—such as views on materialism and altruism—vary across cultures (Guo et al. 2013). These values can persist across generations, even after immigration (Costa-Font et al. 2018). Relying on Western models risks missing key client perspectives and motivations. Prioritizing cultural awareness ensures that financial guidance aligns with the diverse values of financial planning clients (Tanaka-Matsumi 2022).

Cultural Influences on Financial Behavior and Communication

Financial behaviors and decision-making are also shaped by culture, necessitating knowledge of different cultural communication styles to avoid misunderstandings. Clients from collectivist backgrounds, such as Asian cultures, often involve their extended family in financial conversations (Ladha et al. 2018). Additionally, religious traditions can influence economic priorities. For example, Catholic-majority nations tend to protect debtors’ rights, whereas Protestant-majority countries emphasize creditor protections (Stulz and Williamson 2003).

Communication style adds another layer to client–adviser exchanges. In low-context cultures, such as the United States, meaning is conveyed directly through explicit language. However, in high-context cultures, including many Middle Eastern countries, much is communicated indirectly through nonverbal communication such as body language and cultural cues (Ladha et al. 2018). Advisers unfamiliar with these norms may miss important signals or be perceived as blunt. These risks are magnified in high-power distance cultures, where authority figures—like financial planners—are rarely questioned, leading to misinterpretations of consent or agreement (Verma et al. 2016). Thus, these differences highlight the need for advisers who tailor strategies to cultural nuances.

Beyond Awareness: Building ‘Competemility’

Cultural competemility—a concept originally developed in healthcare that integrates cultural competence (the acquisition of cultural knowledge and skills) with cultural humility (an ongoing commitment to self-evaluation and openness)—emphasizes learning about clients’ cultural backgrounds and maintaining conscious awareness of one’s limited perspective (Stubbe 2020). Additionally, it involves acknowledging the possibility of unconscious biases, remaining open to correction, and fostering curiosity about clients’ lived experiences. Atewologun et al. (2018) found that unconscious bias training raises awareness and can reduce implicit bias, although there is limited evidence for behavioral change. Thus, competemility encourages practitioners to ask respectful, open-ended questions about cultural values and practices, recognize that expertise lies within the client context, and cocreate personalized strategies reflecting shared understandings, which may aid in fostering behavioral shifts. This can enhance trust, communication, and engagement by reinforcing the client’s sense of dignity and agency.

Theory: Hofstede’s Cultural Dimensions

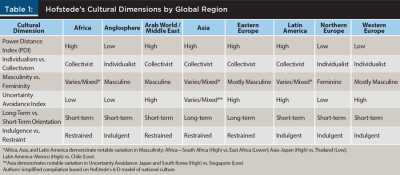

Hofstede’s cultural dimensions theory, widely used in international business, is employed to understand cultural differences across countries (Wale 2023). Hofstede’s theory has six dimensions: power distance index (PDI), individualism versus collectivism (IDV), masculinity versus femininity (MAS), uncertainty avoidance index (UAI), long-term versus short-term orientation (LTO), and indulgence versus restraint (IVR). In the context of financial planning, Hofstede’s theory suggests that within these dimensions, cultural values shape individuals’ financial decisions and how clients interact with financial professionals (Nickerson 2023). As such, we have utilized The Culture Factor Group’s (n.d) Country Comparison Tool to identify countries within these six dimensions. Table 1 consolidates the data provided by the comparison tool to deliver an overview of Hofstede’s cultural dimensions by global region.

The following sections elaborate on each of Hofstede’s dimensions in greater detail, further illustrating how these cultural tendencies shape financial decision-making.

The PDI reflects the degree to which an individual accepts unequal power distribution. In low PDI cultures (like Denmark), democratic relationships, value transparency, and autonomy are key to decision-making (Nickerson 2023). In contrast, high PDI cultures, such as those in Malaysia, often defer to authority, seeking guidance rather than collaboration (Nickerson 2023).

IDV describes the extent to which individuals are integrated into groups (Nickerson 2023). Individualistic societies (like the United States) emphasize personal achievement and individual rights, while collectivist societies emphasize group goals and interdependence (Nickerson 2023). Advisers can expect to see varying levels of prioritization for family or community financial goals, such as supporting aging parents or funding group-owned property rather than individual wealth accumulation.

According to Nickerson (2023), MAS relates to emotional roles between genders. Their research also indicates that masculine cultures—such as Japan (Mitrović 2017)—value competitiveness, assertiveness, and material success. Feminine cultures—like the Netherlands (Singh et al. 2023)—prioritize relationships, modesty, and quality of life. Masculine versus feminine differences are also evident in risk-taking and investment styles.

Furthermore, UAI reflects how strongly members of a culture feel threatened by ambiguous or unknown situations (Nickerson 2023). High UAI cultures (such as Greece) prefer predictability and security through guaranteed products, like insurance or financial plans with clear milestones. In contrast, low UAI cultures (Jamaica) are more comfortable with ambiguity, making them more receptive to alternative assets or entrepreneurial endeavors.

LTO refers to the degree to which a society prioritizes long-term devotion to traditional and forward-thinking values (Nickerson 2023). Long-term oriented cultures (such as South Korea) are more likely to value saving, investing early, and planning for retirement. Short-term oriented cultures (Nigeria) may focus on immediate needs or gratification, rather than future financial needs or planning. Moreover, IVR examines attitudes toward gratification and impulse control (Nickerson 2023). Indulgent cultures (such as Mexico) may prioritize spending on enjoyable experiences and luxuries, often at the expense of long-term financial goals. Restrained cultures (such as those in Egypt) typically display stronger saving habits and greater delay of gratification.

By understanding these dimensions and their impact on financial behavior, advisers can develop culturally responsive approaches that honor clients’ deeply held values while helping them achieve their financial goals. Integrating cultural awareness into financial planning transforms the adviser–client relationship into a meaningful partnership that respects the whole person behind the plan.

Intervention Tools

Culture Tree

The Culture Tree, created by Zaretta Hammond through her work in culturally responsive teaching in education, is a lens to view culture and cultural meaning within three levels (Colorado Department of Education 2020.). Surface is the first level and focuses on our senses and concrete elements such as music, food, and attire. The second level, paradoxically named Shallow, encompasses the subtle yet powerful cultural elements such as nonverbal cues, social expectations, and implicit behavioral norms (Colorado Department of Education 2020). Deep is the third and final level. Embedded in this level are implicit worldviews and subconscious beliefs that shape human experience. It reflects the cultural underpinning ethics, spirituality, well-being, and the pursuit of social cohesion (Colorado Department of Education 2020).

LEARN Model

The LEARN model, initially developed for healthcare, provides a five-step framework for building trust and rapport across cultural lines (Ohlan et al. 2022). However, we’ve adapted certain components and integrated the model with the Culture Tree framework to better align with financial services research and serve diverse clientele.

Step 1: Listen with Depth for implicit worldviews and subconscious beliefs that shape human experience in line with the Culture Tree.

- Practice active listening by creating space for genuine understanding while being aware of how your worldview affects what you hear.

Tip: Start with questions that give insight into clients’ upbringing and foundational financial beliefs, and be mindful of how these views impact your conversation in the present. - Check your assumptions about what clients/families “should” value or prioritize. Recognize when discomfort with certain groups may impede your listening abilities and replace that discomfort with curiosity.

Tip: Take a moment to digest what the client is sharing and if you feel their values, actions, or beliefs are in conflict with your own. Pause and reflect before responding.

Step 2: Explore Shallow depths by examining aspects of culture that can guide our daily life and routines such as how one views elders, personal space, and eye contact, or even concepts of time.

- Ask curious, respectful questions about cultural backgrounds, especially with clients and families with whom you don’t naturally connect with.

Tip: Aim the conversation toward the root of their lived experiences, family belief systems, and, ultimately, their concerns and fears. Understanding the fear behind certain actions or beliefs can reveal our commonalities. - Examine your relationship patterns and investigate the “why” behind judgments about client and prospect behaviors. Are you gravitating toward certain clients over others?

Tip: Reflect on whether something that was done or said has ignited an uncomfortable feeling within you and begin to identify the origins. - Educate yourself further about a client’s culture.

Tip: Explore books, podcasts, documentaries, or attend social events related to a client’s culture to deepen your understanding. - Push beyond your comfort zone to understand experiences different from your own.

Tip: Seek feedback from colleagues to gain insight into blind spots and potential biases.

Step 3: Acknowledge your cultural lens and growth.

- Own any biases about which cultural expressions you see as assets versus deficits.

Tip: Consider taking an “Implicit Association Test” to grasp your patterns and judgment tendencies. - Admit any preferences for certain attire, communication styles, or family structures.

- Recognize how your beliefs may give some families advantages over others, and how this could interfere with the planning engagement or the long-term nature of a client relationship.

Step 4: Respect by implementing equity-minded action and culturally responsive recommendations.

- Honor diverse family values even when they differ from your own understanding.

Tip: Find ways to communicate that you’re listening and honoring clients’ preferences. - Offer multiple pathways that don’t solely encourage or reflect your cultural preferences.

- Ensure equitable access to opportunities, resources, and information. Be open to different approaches and assets rather than expecting assimilation to your norms.

Step 5: Nurture ongoing growth with cultural awareness and sensitivity.

- Stay engaged, remain adaptive, and continue evolving in examining your foundational beliefs and how these impact clients, and focus on inclusivity.

Tip: Commit to approaching interactions from a place of empathy, curiosity, and openness as often as possible. Embrace lifelong learning, as it has benefits for you and your clients. - Reflect back to your client your understanding of their cultural norms and beliefs in a way that demonstrates you honor and respect their differences.

Tip: This could include maintaining certain rituals (e.g., offering tea), respecting physical boundaries (handshakes over hugs), modeling specific plan scenarios, or other ways to show you’ve been listening.

LEARN Model with Culture Tree Integration

The LEARN model serves as a communication blueprint for how advisers can engage in conversations with their culturally diverse clientele. Meanwhile, the Culture Tree helps provide a deeper understanding of the different elements of one’s culture and serves as the diagnostic framework for why people think and behave the way they do. Thus, the LEARN model, combined with Culture Tree implementation and Hofstede’s cultural dimensions, create a practical tool for advisers to enhance cross-cultural communication and foster trust, thereby strengthening long-term partnerships across diverse client bases. Ultimately, integrating both models provides improved context and clarity, enabling financial professionals to understand clients and their needs holistically.

Case Illustrations and Hofstede’s Cultural Dimensions Theory

Balancing Legacy and Longevity

Raj immigrated to the United States from India in the early 1970s, followed by his wife Meena and their two children. He built a career in real estate development and management, while Meena worked in accounting and bookkeeping. Throughout their professional lives, they made a concerted effort to utilize their substantial accumulated wealth to support their family and others in the United States and India, becoming known for their generosity within their community. This pattern reflected deeply held cultural values around kinship, community responsibility, and collective success.

As Meena entered her 80s, she was diagnosed with a degenerative brain disorder that progressively limited her independence, requiring intensive care. The associated expenses—home health aides, medical specialists, and specialized accommodations—placed substantial strain on the family’s finances. While their portfolio previously supported a generous lifestyle and secure future, the costs of long-term care shifted the financial equation.

The couple’s adult children advocated for financial realignment. They urged Raj to limit discretionary gifts and focus resources on his and Meena’s well-being and long-term needs. Raj was hesitant. For him, generosity was an expression of identity and moral commitment.

In this context, the financial planner’s role became multifaceted: providing technical guidance while navigating the cultural and emotional dimensions of family decision-making. Recommendations centered on reframing the conversation around legacy, caring for Meena, and preserving Raj’s financial independence as ways to honor their personal values.

To achieve this goal, the planner used a two-pronged approach. First, recognizing Raj’s proficiency with numbers, the planner presented a detailed financial projection of how Meena’s healthcare costs would deplete their assets if giving continued at the same rate, asking questions like, “How can we ensure Meena’s care is funded while still reflecting your commitment to the community?” Second, to avoid appearing to side with the children or dismissing Raj’s values, the planner organized a family meeting with Raj, his children, and generational peers from the Indian community. During this meeting, the planner acknowledged Raj’s lifelong generosity, saying, “Raj, you’ve supported many, helping businesses grow and uplifting families in both countries. How can we balance this legacy with the care Meena needs?” Thus, Raj’s contributions were affirmed while the shift in priorities was reframed as a community-supported decision. This allowed portfolio and financial adjustments while long-term care, estate, and charitable-giving planning were introduced with more structured and future-oriented goals.

This case underscores the complex interplay between cultural norms, generational dynamics, and financial realities. In such situations, effective planning necessitates cultural sensitivity, emotional intelligence, and the ability to help clients adapt their values to new circumstances without abandoning them. Cultural values—such as the strong emphasis on collective responsibility and generosity—can shape spending priorities in ways that may initially appear at odds with traditional retirement planning frameworks but actually align with and complement them.

‘Competemility’ in Action

The prior case study highlights a successful application of “competemility.” The adviser offered:

- Technical Clarity with Respectful Framing

The planner leveraged Raj’s comfort with numbers by providing a clear financial projection, but instead of simply showing depletion risk, they asked: “How can we ensure Meena’s care is funded while still reflecting your commitment to the community?” This demonstrated technical competence while humbly framing Raj as the decision-maker and recognizing his personal values.

Focusing on technical rigor without cultural sensitivity. The planner could have provided Raj with hard numbers and depletion timelines but framed the conclusion bluntly: “If you keep giving at this rate, you won’t be able to afford Meena’s care.” While financially accurate, the lack of humility toward Raj’s values could feel dismissive and alienating, reducing his trust in the adviser.

- Affirmation of Legacy While Guiding Change

During the family meeting, the planner acknowledged Raj’s decades of generosity before suggesting adjustments. Recognizing and affirming his cultural and personal identity displayed humility. Guiding the conversation toward actionable steps revealed competence.

Minimizing Raj’s identity as a giver. In conversations with the family, the planner might have focused solely on healthcare needs and asset preservation, neglecting to affirm Raj’s lifelong role as a benefactor. Dismissing his contribution to his family and community risks making Raj feel that financial adjustments equate to moral failure or loss of dignity.

- Inclusion of Multiple Voices

By inviting both family and respected community peers, the planner avoided imposing a top-down financial solution. Instead, they facilitated a dialogue where Raj’s cultural values could be validated by his own reference group, showing humility in ceding authority while still steering to a more sustainable plan.

Excluding cultural and generational voices. To “keep things simple,” the planner could have met only with Raj’s children and not the broader community. This may appear efficient, but it sidelines the cultural structures that are important to Raj, potentially creating conflict between him and his children while undermining buy-in for the financial plan.

Implications for Practice

As our sociopolitical climate is ever-changing, nearly everyone is aware of diversity in beliefs. Cultural diversity lies within generational ties, religion, familial values, geographic origins, and humanity as a whole. Statman (2018) argues that advisers who emulate cultural literacy can build long-lasting relationships with clients. Therefore, understanding the inherent importance of shared values and finding common ground requires amelioration.

As family governance and wealth transfer become increasingly important, families across demographic groups are prioritizing the transmission and legacy of values, in addition to assets. Estate planning with a financial planner or professional is a natural and effective way to build this relationship. It allows practitioners to learn more about clients and creates an opportunity for an introduction to a client’s immediate and extended family. Identifying a client’s cultural dimension, cohort, or values is a beneficial approach to structuring estate planning conversations, which can build familiarity and trust throughout the entire family.

When cultures integrate, practitioners need to utilize the LEARN model and Culture Tree while recognizing the intricacy and bravery required for change. Clients benefit from a varied approach, and it would be advantageous to leverage these theories and tools in tandem with fintech resources such as financial planning software, thus creating a mutual baseline understanding of the client holistically (Berlin and Fowkes 1983). Furthermore, this approach helps mitigate cultural differences and creates a common, yet personalized, goal.

Discussion

Financial planners can learn from the medical field’s work on the importance of cross-cultural competency. However, these medical studies often have small sample sizes, making it challenging to apply conclusions universally across diverse cultural contexts and socioeconomic environments. These limitations in medical studies underscore the need for more comprehensive methodological research in both the medical and financial services fields, accounting for cultural nuances in financial planning behaviors.

Research on cross-cultural competencies in financial planning is limited. This paper contributes to addressing this gap by identifying transferable principles between medical and financial planning contexts. Financial professionals who effectively communicate across generational and cultural boundaries, utilizing the LEARN model and Culture Tree, demonstrate: (1) awareness of their own cultural biases, (2) respect for diverse value systems, and (3) attentive listening skills that capture clients’ underlying messages. Whether an individual works in medicine, education, or financial planning, acknowledging a client’s adaptability, nourishing the relationship through consistent communication, finding similarities, and appreciating differences creates the foundation for a successful professional relationship. By finding common ground in these fields, we provide valuable evidence-based insight and tools to assist advisers and financial planners.

Conclusion

This paper examines cross-cultural differences and competency through the lens of Hofstede’s cultural dimensions and generational cohort theory, aiming to bridge the research gap, reduce polarity, and provide practitioners with evidence-based strategies to better serve the evolving demographics of their clients. Each generation and family has unique challenges and overlapping similarities. Regardless of the client or dimension, deeply held cultural values can serve as common ground.

Increasing globalization and client demographics are the catalysts for cultural competence becoming a necessity. The LEARN model and Culture Tree can help cultivate an authentic, communicative relationship. Furthermore, utilizing Hofstede’s cultural dimensions theory as a lens to understand clients’ values and decision-making, as well as those of the practitioner, can be a helpful guide to navigating differences and finding shared interests. By integrating professional acumen and intercultural understanding, professionals can create respectful and honest relationships where all parties feel understood and valued. This responsive approach enables clients to achieve financial goals that align with their cultural and personal values, while allowing advisers to enhance their expertise and build a thriving practice.

Citation

Buckner, Mo, Matthew S. Brady, Jack M. McAulay, Marja Sweet, and Meghaan R. Lurtz. 2026. “The Unseen Adviser: How Cultural Dimensions Silently Shape Client Financial Goals and Behaviors.” Journal of Financial Planning 39 (4): 58–68.

References

Atewologun, D., T. Cornish, and F. Tresh. 2018, March. “Unconscious Bias Training: An Assessment of the Evidence for Effectiveness.” Equality and Human Rights Commission. www.equalityhumanrights.com/sites/default/files/research-report-113-unconcious-bais-training-an-assessment-of-the-evidence-for-effectiveness-pdf.pdf.

Berlin, E. A., and W. C. Fowkes. 1983, December. “A Teaching Framework for Cross-Cultural Healthcare—Application in Family Practice.” The Western Journal of Medicine. https://pmc.ncbi.nlm.nih.gov/articles/PMC1011028/.

Buhrmann, J. 2023, December 13. “What Clients Want from Their Financial Advisor.” eMoney Advisor. https://emoneyadvisor.com/blog/what-do-clients-want-from-their-financial-advisor/.

Colorado Department of Education. 2020. “Overview of Culturally Responsive Practices: The Culture Tree.” https://sitesed.cde.state.co.us/mod/book/view.php?id=8030&chapterid=8125.

Costa-Font, J., P. Giuliano, and B. Ozcan. 2018. “The Cultural Origin of Saving Behavior.” PLOS One 13 (9). https://doi.org/10.1371/journal.pone.0202290.

Grubman, J., and D. T. Jaffe. 2016, November 1. “Becoming a Culturally Intelligent Financial Planner.” Journal of Financial Planning 29 (11): 31–33. www.financialplanningassociation.org/article/journal/NOV16-becoming-culturally-intelligent-financial-planner.

Guo, L., D. Stone, S. Bryant, B. Wier, A. Nikitkov, C. Ren, et al. 2013. “Are Consumers’ Financial Needs and Values Common Across Cultures? Evidence from Six Countries.” International Journal of Consumer Studies 37 (6): 675–688. https://doi.org/10.1111/ijcs.12047.

Hofstede, G. 2024, March 25. Geert Hofstede. https://geerthofstede.com/.

Horton, C. 2024, December 5. “U.S. High-Net-Worth and Ultra-High-Net-Worth Markets 2024: The Great Wealth Transfer: Capturing Money in Motion.” Cerulli Associates. www.cerulli.com/reports/us-high-net-worth-and-ultra-high-net-worth-markets-2024.

Ladha, T., M. Zubairi, A. Hunter, T. Audcent, and J. Johnstone. 2018, February 15. “Cross-Cultural Communication: Tools for Working with Families and Children.” Pediatrics & Child Health 23 (1): 66–69. https://pubmed.ncbi.nlm.nih.gov/29479280/.

Mitrović, M. 2017, August. “Cultural Dimensions of Japan & East-Asian Cluster in Tourism.” International Journal of Computational Engineering Research 7 (8): 27–35. www.ijceronline.com/papers/Vol7_issue8/E07082735.pdf.

Nickerson, C. 2023, October 24. “Hofstede’s Cultural Dimensions Theory & Examples.” Simply Psychology. www.simplypsychology.org/hofstedes-cultural-dimensions-theory.html.

Ohlan, S., P. Singhal, R. Dagar, M. Goyal, and S. Goyal. 2022. “A LEARN Model Approach in Healthcare for Improvising the Doctor–Patient Relationship.” International Journal of Community Medicine and Public Health 9 (4): 1921–1926. https://doi.org/10.18203/2394-6040.ijcmph20220875.

Perkins, M. 2019, May 28. “When Culture Is Ignored, Advisor–Client Relationships Can Fail.” Financial Planning. www.financial-planning.com/news/financial-planning-experts-on-cultural-competency-diversity-and-inclusivity.

Pokharel, J., and I. Maharjan. 2024. “Financial Behavior of Generation Z and Millennials.” Journal of Emerging Management Studies 1 (2): 148–170.https://doi.org/10.3126/jems.v1i2.71522.

Rubin, J. D., K. Chen, and A. Tung. 2024, June 10. “Generation Z’s Challenges to Financial Independence: Adolescents’ and Early Emerging Adults’ Perspectives on Their Financial Futures.” Journal of Adolescent Research. https://doi.org/10.1177/07435584241256572.

Singh, J., F. J. Valdez Perez, J. Szadkowska, and T. Heus. 2023, February 18. “Cultural Diversity at a Top Tier Bank in the Netherlands.” The Model to Practice Dialogues MTPDTM. https://mtpdculture.org/cases/cultural-diversity-at-a-top-tier-bank-in-the-netherlands.

Statman, M. 2018, August. “Culture Matters to Clients, and it Should Matter to Planners.” Journal of Financial Planning 31 (8): 32–34. www.financialplanningassociation.org/article/journal/AUG18-culture-matters-clients-and-it-should-matter-planners.

Stubbe, D. E. 2020. “Practicing Cultural Competence and Cultural Humility in the Care of Diverse Patients.” Focus 18 (1): 49–51. https://doi.org/10.1176/appi.focus.20190041.

Stulz, R. M., and R. Williamson. 2003, December. “Culture, Openness, and Finance.” Journal of Financial Economics 70 (3): 313–349. https://doi.org/10.1016/s0304-405x(03)00173-9.

Tanaka-Matsumi, J. 2022, August 12. “Counseling Across Cultures: A Half-Century Assessment.” Journal of Cross-Cultural Psychology 53 (7–8): 957–975. https://doi.org/10.1177/00220221221111810.

The Culture Factor Group. (n.d.). “Country Comparison Tool.” www.theculturefactor.com/country-comparison-tool.

Verma, A., A. Griffin, J. Dacre, and A. Elder. 2016, June 10. “Exploring Cultural and Linguistic Influences on Clinical Communication Skills: A Qualitative Study of International Medical Graduates.” BMC Medical Education 16. https://doi.org/10.1186/s12909-016-0680-7.

Wale, H. 2023, October 19. “Hofstede’s Cultural Dimensions Theory.” Corporate Finance Institute. https://corporatefinanceinstitute.com/resources/management/hofstedes-cultural-dimensions-theory/.