Journal of Financial Planning: February 2018

Randy Gardner, J.D., LL.M., CPA, CFP®, is coauthor of the forthcoming 101 Tax Saving Ideas, eleventh edition, and founder of Goals Gap Planning LLC (goalsgapplanning.com), a fee-only personal financial planning firm.

Leslie Daff, J.D., is a state bar certified specialist in estate planning, trust, and probate law and the founder of Estate Plan Inc.

On December 22, 2017, President Trump signed into law the Tax Cuts and Jobs Act. The act is complex and impacts numerous tax specializations, including individual, corporate, and international planning. This column focuses on what individual taxpayers can do to save money in 2018. Unless indicated otherwise, the act provisions discussed here take effect in 2018 and expire after 2025.

Lower Tax Rates, Lost Exemptions, and Increased Standard Deductions

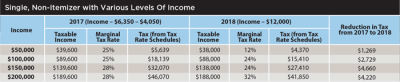

Planning for 2018 starts with a review of your clients’ 2017 tax returns. In 2018, the applicable tax rates for a given level of income are generally (although not always) the same or lower than they were in 2017. The $4,050 exemption deductions for the taxpayer, the taxpayer’s spouse, children, and other dependents, disappear in 2018; and the standard deduction almost doubles from $6,350 to $12,000 for single filers ($12,700 to $24,000 for married individuals filing a joint return).

Although the projected 90 percent of single and married taxpayers who will claim the standard deduction will likely pay lower taxes and complete simpler tax returns, their planning opportunities are limited to self-employment, fringe benefit, and credit strategies. For example, a taxpayer with a $200,000 home subject to a $160,000 mortgage will likely claim the standard deduction rather than itemizing, decreasing the tax incentives of home ownership.

Itemized Deductions

Itemized deductions are significantly different under the act:

The floor for deductible medical expenses is reduced to 7.5 percent (from 10 percent) for 2017, 2018, and 2019. It makes sense to schedule discretionary medical procedures in 2018 and 2019 if doing so will lead to a medical expense deduction.

State and local income, sales, and real and personal property taxes are limited to $10,000.

Although existing mortgages are grandfathered in subject to the prior $1 million cap, interest expense on acquisition indebtedness for up to two homes is capped at $750,000 total for loans incurred after December 15, 2017 through 2025. Interest on home equity loans is not deductible after 2017 through 2025.

The percentage limitation for charitable contributions of cash is increased from 50 percent to 60 percent of adjusted gross income, and the deduction for payments connected to the purchase of tickets and preferential seating at athletic events is repealed.

The deduction for casualty and theft losses is allowed only for presidentially declared disaster areas.

Miscellaneous itemized deductions, such as tax preparation fees, investment expenses, and unreimbursed employee expenses are disallowed after 2017. Individuals with significant unreimbursed employee expenses, including mileage, Internet/phone charges, and education costs should request an excludable working condition fringe benefit arrangement or accountable plan from their employers.

The phaseout of itemized deductions at higher income levels disappears after 2017.

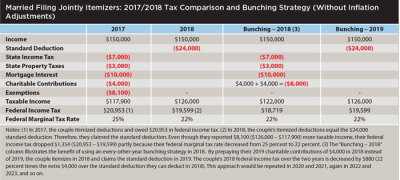

For single and married clients with itemized deductions close to the standard deduction amounts, the type of “bunching” strategy used with discretionary deductible expenses, such as charitable contributions, medical expenses, and state and local taxes below the $10,000 level, will become an important planning technique.

Alternative Minimum Tax and State and Local Tax Deductions

High-income taxpayers, particularly those in high-tax states like California, New York, and New Jersey are going to lose significant amounts of deductions because of the $10,000 cap on state and local taxes, but they will have some relief because of the lower tax rates and changes made to the alternative minimum tax (AMT).

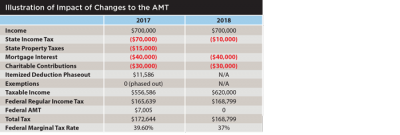

In 2017, the AMT exemption amount is $54,300 for unmarried individuals ($84,500 for married individuals filing a joint return). This exemption is phased out at a 25 percent rate when alternative minimum taxable income (AMTI) exceeds $120,700 ($160,900 for married individuals filing a joint return). In 2018, the exemptions significantly increase to $70,300 for unmarried individuals ($109,400 for married individuals filing a joint return). More importantly, the phaseout thresholds are increased to $1 million for married individuals filing a joint return and $500,000 for other individual taxpayers. Because they lost $75,000 ($70,000 + $15,000 – $10,000) of state and local tax deductions, the couple pays $3,160 ($168,799 – $165,639) more regular tax in 2018, but $3,845 ($172,644 – $168,799) less total tax because they avoid the alternative minimum tax (see the table above).

Individuals with capped state and local tax deductions should keep their eyes on efforts by their state legislatures to circumvent the federal cap. California, for example, has proposed restructuring “tax payments” as charitable contributions in order to keep the federal tax deductions for its taxpayers.

Family and Education Planning

Child and family credit. The act increases the child tax credit to $2,000 per qualifying child; $1,400 of this amount is refundable. The act also adds a $500 nonrefundable credit for qualifying dependents other than children. More importantly, the act increases the phaseout for the child tax credit to $400,000 from $110,000 for married taxpayers filing a joint return and to $200,000 from $75,000 for other taxpayers.

The “kiddie tax.” The tax on unearned income of children is completely overhauled by the act. Parents’ income and the unearned income of siblings no longer factor into the equation. Instead, earned income of a child is taxed according to an unmarried taxpayer’s rates. Taxable income attributable to net unearned income is taxed according to the unfavorable tax rates applicable to trusts and estates.

Education benefits. Although they were in jeopardy, education benefits—the student loan interest deduction, education credits, exclusion for savings bond interest, tuition waivers for graduate students, and the educational assistance fringe benefit—remain intact.

Section 529 plans. Qualified education expenses of a 529 account are expanded to include up to $10,000 per year for a child’s elementary and secondary education whether it is in a public, private, or religious environment.

ABLE accounts. Contributions to ABLE accounts are now eligible for the retirement saver’s credit, and a child’s 529 account can be rolled over to an ABLE account for the child.

Independent Contractors and Entrepreneurs

Despite the repeal of the deduction for entertainment expenses, the act contains strong incentives for individuals to go into business for themselves. Although these provisions are subject to limitations that are too complex to explore in detail here, the most obvious examples of these incentives are: the immediate deduction for major asset purchases; the 21 percent maximum corporate tax rate; and the 20 percent of business income deduction for sole proprietors, partners in partnerships, shareholders in S corporations, and trusts and estates.

Favored businesses include: real estate businesses and service businesses in the fields of health, law, accounting, financial services, performing arts, consulting, and many others which generally do not benefit from this type of favorable treatment. Employers and even employees may seek to change the status of workers to an independent contractor arrangement, rather than an employer/employee relationship.

Investment Considerations

The prior law treatment of capital gains and qualified dividends continues under the new law. The proposal to require the use of the first-in, first-out out method to calculate gains was not enacted, meaning individuals are still able to choose which years to recognize gains and losses.

As under prior law, in 2018, the thresholds shown in the table above need to be considered when planning.

Estate, Gift, and Generation-Skipping Tax Changes

The exemption amounts for the gift, estate, and generation-skipping taxes are doubled from $5.6 million to $11.2 million ($22.4 million for couples), and the income tax basis step up/down to fair market value at death continues under the act. These changes provide high net worth individuals a significant planning window to make gifts and set up irrevocable trusts.

Anticipating that the exemption amounts will revert in 2026 to 2017 levels (although the exemption amount has never decreased before), claiming the portable exemption will remain an important discussion topic for decedents with more than $3 million in assets.

Other Miscellaneous Changes

The number of changes and tweaks made to “old law” by the Tax Cut and Jobs Act is mind-boggling. The following three, however, are worth noting.

Alimony. Under prior law, alimony and separate maintenance payments were deductible by the payor and includible in income by the payee. For divorce and separation instruments executed or modified after December 31, 2018, alimony and separate maintenance payments are not deductible by the payor spouse, nor includible in the income of the payee spouse. These changes will profoundly affect the structure of divorce settlements.

Moving expenses. The deduction for moving expenses is suspended except for the in-kind moving and storage expenses for members of the Armed Forces (or their spouse or dependents) on active duty who move pursuant to a military order and incident to a permanent change of station.

Roth conversions. Individuals can no longer unwind a Roth conversion by re-characterizing it. However, in the year of contribution, an individual may continue to make a contribution to a Roth IRA and, before the due date for the individual’s income tax return for that year, recharacterize it as a contribution to a traditional IRA, and vice versa.

As clients complete their 2017 tax returns, financial planners should plan to set aside time with their clients to develop individualized strategies in response to the new tax law.