Journal of Financial Planning: April 2018

Randy Gardner, J.D., LLM, CPA, CFP®, is the founder of Goals Gap Planning LLC, in Laguna Beach, California.

Julie A. Welch, CPA, PFS, CFP®, is a shareholder with Meara Welch Browne, P.C. in Leawood, Kansas. She is the co-author (with Randy Gardner) of the recently updated 101 Tax Saving Ideas, 11th Edition. To obtain a copy, email Julie HERE.

The tax cuts and Jobs Act (the Act) repeals the above-the-line deduction for alimony and separate maintenance payments and makes such payments nontaxable to recipients. The change applies to divorce or separation instruments executed after Dec. 31, 2018. The revisions also apply to instruments executed before the effective date, if they are modified after Dec. 31, 2018 and expressly provide that new law will apply to the modification.

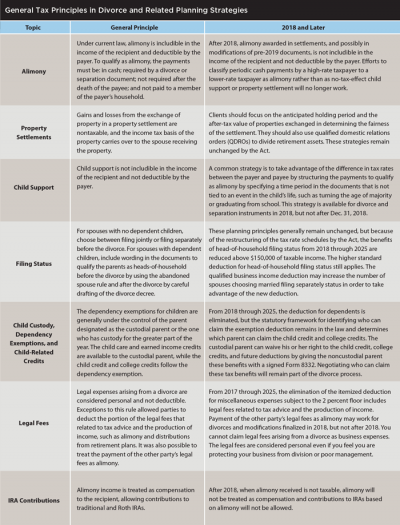

The Act revisions impacting divorce planning go beyond the alimony changes. A summary of the general tax principles in divorce and related planning strategies is set out in the table at the end of this article.

As a result of these changes, 2018 is an important planning year for clients in the midst of a divorce, contemplating a divorce, or needing to modify documents from a prior divorce. Whether it is better for a client to fall under old law or new law needs to be evaluated before the end of the year. What is beneficial to one spouse in a divorce may not be beneficial for the other. Thus, for one client, you may be recommending old-law treatment, while with another client you may be recommending new-law treatment. Advising both spouses when they are going through a divorce always raises conflict-of-interest issues, but in 2018 it may be even more important to obtain signed disclosures and waivers before you offer advice to both sides.

There are three common alimony strategies to consider this year:

Reclassification of Child Support as Alimony

If soon-to-be ex-spouses are in different income tax rate brackets before Dec. 31, 2018, it may be beneficial to structure the divorce decree such that all or a portion of payments for child support, a property settlement, and the spouse’s legal fees are treated as alimony.

Example. The client is in the 40 percent marginal federal and state income tax rate bracket and is willing to pay up to $24,000 of annual child support. The client’s spouse is in the 18 percent federal and state income tax rate bracket and wants at least $28,800 of annual child support. Both can stay close to their goals and perhaps reach a compromise by treating the payments as alimony. The spouse should be indifferent between receiving $28,800 in child support and $35,122 ($28,800/(1 – 0.18)) in alimony. Because the client can deduct alimony payments but not child support, the client should be indifferent between paying $24,000 in child support and $40,000 ($24,000 /(1 – 0.40)) in alimony.

Reclassifying the payments from child support to alimony at an amount somewhere between $35,122 and $40,000, such as $36,000, accomplishes both of their goals. At $36,000, for example, the client will be out of pocket $21,600 ($36,000 x (1 – 0.40)), and the client’s spouse will receive $29,520 after payment of taxes.

Reclassification of the Imbalance in the Property Settlement as Alimony

After adding up the equity in the home, the balances in the retirement accounts, and the value of other properties and dividing the total between the two spouses, there is often a difference that must be paid by one spouse to the other to equalize the settlement. Property settlements are typically not deductible by the payer and not includible in the income of the payee.

However, if this imbalance is paid by the higher-rate client to the lower-rate client and treated as alimony, both spouses may benefit. Assume the couple in the earlier example arrived at a property settlement that required the higher-tax-bracket spouse to write a $20,000 check to the lower-tax-bracket spouse. If the payment is treated as alimony, the higher-rate spouse might write a check for $24,390 ($20,000/(1 – 0.18)), giving the lower-rate spouse $20,000 after tax. The higher-rate spouse is out of pocket $14,634 ($24,390 x (1 – 0.40)), significantly less than $20,000.

Reclassification of the Payment of the Ex-Spouse’s Legal Fees as Alimony

Assume the higher-rate spouse is responsible for paying the lower-rate spouse’s $15,000 legal fees. Treating the payment as alimony allows the higher-rate spouse to write a check for $18,293 ($15,000/(1 – 0.18)) to the lower-rate spouse. After tax, the higher tax bracket spouse is out of pocket $10,976 ($18,293 x (1 – 0.40).

Note that the reclassifications shown in these three examples are usually spread over at least three years and must be structured properly to receive the desired alimony treatment. The divorce or separation instrument language should be reviewed by the clients’ family law attorneys to ensure federal and state law requirements are satisfied.

From these examples, you can see part of the reason the Congressional Budget Office estimates that the elimination of the alimony inclusion and deduction will produce $6.9 billion of additional revenue for the government over the next 10 years. The additional revenue is also attributable to the “alimony gap.” The Internal Revenue Service says 361,000 taxpayers claimed they paid a total of $9.6 billion in alimony in 2015, although only 178,000 taxpayers reported receiving spousal support.

The numerous Act provisions affecting divorce will have a ripple effect. States will have to adjust their child support and alimony tables and procedures. Fewer spouses will be willing to pay alimony, preferring instead to deal with income inequality through nontaxable property settlements. Battles for custody and the child-related credits will likely become more emotional.

Financial planners will play an increasingly important role helping clients resolve the conflicts associated with divorce, work through the short-term pain, and stay focused on the long-term financial implications of the marital split.