Journal of Financial Planning: November 2025

Dr. Fred de Jong (1971) is an associate professor of sustainable finance and tax at the HAN University of Applied Sciences in The Netherlands, academic director of the Master Integrated Advice SME program, and a self-employed researcher/consultant with specific expertise in financial advice markets, which resulted in a Ph.D. in 2010.

Marcel van Kooten, LL.M., MFP, CFP®, is a senior lecturer finance and tax at the HAN University of Applied Sciences in The Netherlands, senior lecturer in the Master Integrated Advice SME program, and a self-employed tax, financial, and pension adviser.

Robert G.J. van Beek, CFP®, (1973) is founder and director of About Life & Finance, and partner at Bond Capital Partners. He (co)authored more than 25 books. Robert is a former member of the National Board of Directors for the Financial Planning Association® (FPA®) and is a member of the Editorial Board of the Journal of Financial Therapy.

Siem de Ruijter (1977) holds a bachelor’s degree in accountancy and taxation and a master’s degree in business economics. He is a lecturer at UC Leuven-Limburg in Belgium, where he teaches investing, entrepreneurship, and digital accounting tools. Prior to this, he worked as an investment relationship manager at Bacob Bank and as a consultant in accountancy and tax. He is coauthor of the books Sustainable Investing (Lannoo) and Investment Fundamentals (Van In).

NOTE: Click the image below for a PDF version.

JOIN IN THE DISCUSSION: Discuss this article with fellow FPA Members through FPA's Knowledge Circles.

FEEDBACK: If you have any questions or comments on this article, please contact the editor HERE.

The international goals for a sustainable economy, set by the United Nations (Sustainable Development Goals) and the Paris Climate Agreement, are still not within reach.1 The goals are extra challenging in an environment of more complexity, political headwinds, and uncertainty for entrepreneurs. Owners of small- and medium-sized enterprises (SMEs) play a vital role in achieving these ambitious goals because they account for 90 percent of all businesses worldwide. With the large financial consequences of the sustainability transition, especially for SMEs, responsible financial management is required. SMEs largely depend on their CPAs and other external financial advisers for this financial management. In this article, we argue there is a need to deepen the financial planning profession, aimed at advising SME entrepreneurs. Being able to achieve these objectives has various financial consequences in their business but also in their private life and in the short and long term. To properly guide this, financial planners should take a closer look at what we call financial business planning (FBP).

Financial Planning for Business

Financial planning is the process that considers a client’s personality, financial status, and socioeconomic and legal environments, and leads to the adoption of strategies and use of financial tools to achieve the client’s financial goals (Warschauer 2002). Financial planning is mainly about advising private clients (and business owners). There is already some relevant research that discusses the relationship between financial planning for individuals and financial planning for businesses. Alhabeeb (2015) introduced the term entrepreneurial finance. Masurel and Van Rijn (1993) talked about business planning. D’Amboise and Muldowney (1988) argue that the financial situation deserves extra attention for the success of small businesses. Important aspects of this are budget planning and cash management. Robinson (1982) concludes that outsiders, such as accountants and consultants, can play an important role in the planning of a business. Overton (2008) characterizes the financial planner as an “outside CFO” for individuals and family businesses. De Jong and Wagensveld (2023) mention that financial advisers can help and influence SMEs in becoming more sustainable and contribute to a more sustainable economy. The input of alternative points of view (Godos-Diez et al. 2018) and different interpretations offered by a financial adviser can stimulate SMEs. SMEs who consider external advice in their decision-making processes are more likely to acquire new knowledge on, for instance, environmental changes, according to Alexiev et al. (2010). The availability of sources of external advice for board members can improve the board’s resource provision role regarding corporate social responsibility (CSR).

Financial advice and financial planning can help businesses cope with external challenges and strategic decision making. We see a specific business opportunity for financial planners in advising SMEs.

Global Planning for Business

SMEs are companies with zero to 249 employees. Worldwide, 90 percent of all companies are SMEs. They represent about 70 percent of worldwide employability and GDP and are vital contributors to economic growth and innovation (Gherghina et al. 2020).2 Like large corporates, SMEs face several challenges and operate in a business environment characterized by VUCA: volatility, uncertainty, complexity, and ambiguity. The VUCA world is about “rapidly changing environments, diverse employees’ needs, and almost unpredictable customer expectations” (Hamid 2019, 1). Scheinpflug and Stolzenberg (2017) state that the VUCA world leads to a dynamic, complex environment because of the mix of challenges. Verkuil (2024) mentions specific challenges for SMEs like internationalization, sustainability, and demographic change. There are more geopolitical tensions emerging from the situation in Ukraine, the subsequent energy crisis, and the tensions in the Middle East. Furthermore (hyper)inflation, coupled with the deeper and longer-term demand for sustainable innovation, climate change, rapid technological developments, and social change, present new challenges. With the rise of Industry 4.0 (the fourth industrial revolution), digitalization also has a huge impact on SMEs. Adopting new technologies is necessary to remain competitive among businesses and in a constantly evolving market and the VUCA world (Kádárová et al. 2023). Bosse and Zink (2019) mention the growing impact of technological innovations that allow products and services to be offered faster, more individually, more customer-oriented, and at lower prices.

The challenges mentioned will affect SMEs for an unforeseen period and will have the biggest effect on less-resilient firms. New financial regulations such as the Corporate Sustainability Reporting Directive (CSRD) in the European Union assume an integrated way of thinking and reporting by imposing requirements on companies to report not only on financial results, but also on the social and ecological impact that the company makes through its business operations and the chain in which the company is active.

The CSRD aims to enable investors to distinguish between companies in terms of sustainability performance. Many disclosure requirements are mandatory, regardless of the materiality assessment, precisely because investors need this information to determine how sustainable their investment portfolio is. De Jong and Wagensveld (2023) expect this will also directly affect SMEs because they must demonstrate to what extent they are becoming more sustainable to attract financing. The degree of sustainability is also becoming a greater factor for SMEs’ insurability. The question is whether non-sustainable companies will still be insurable in the future, regardless of the liability risk that companies run if they greenwash or do not meet sustainability criteria.

To deal with these circumstances, SMEs must invest time and money in new technologies and sustainable solutions but also stay financially healthy at a company level as well as in their personal life. However, they often face limited resources, the complexity of regulatory requirements, technological barriers, and the need for effective risk management (Bello et al. 2024). Oyewole et al. (2024) state that sustainable finance is essential for enhancing the competitiveness of SMEs in the global marketplace. By integrating ESG considerations into financial decisions, SMEs can improve access to capital, enhance market competitiveness, manage risks, seize opportunities, and drive innovation and growth.

Financial Planners as Trusted Advisers for SMEs

The scale and complexity of these challenges create (financial) uncertainty for SMEs. Williamson (1975) established that the existence of financial advisers as intermediaries becomes more significant as uncertainty and complexity increases. Cummins and Doherty (2006) point to the role of the intermediary in simplifying the complexity of products and information and transferring this to the customer. Financial planners are ideally suited to reduce this uncertainty and guide SMEs toward a financially healthy future in a responsible manner for society and the environment. Almost all SME entrepreneurs already use different types of financial advisers, such as an accountant, auditor, bookkeeper, tax adviser, credit or loan adviser, or insurance broker. When advising on annual accounts and tax returns, the focus is more on the past than the future of the company. And advisers often work in a fragmented, non-holistic way: the tax adviser focuses on tax returns, the auditor looks at the reporting, the accountant works on the annual accounts, the insurance broker sells insurance policies, and, when financing is needed, the bank focuses on the possibilities of financing the SME, ratios, cash flows, etc.

Sometimes the owner of the SME hires a financial planner to get guidance for their own personal situation. It gets more complicated when projects need to be financed using money by the owner; things need to be revised and optimized on the level of ownership when SME companies are being sold or succession to the next generation comes into play. A lot of energy and time (and money) is then spent on optimizing the process from a legal, valuation, and more economic perspective. When more money is involved, sometimes you see that so-called family offices are built to advise the family members behind the family-owned SME. Their focus and expertise are often found in the domains of estate planning, wealth planning, and investments.

Nkwinika and Akinola (2023) address the importance of good financial management by SMEs to cope with the challenges described previously. They describe four financial limitations most SMEs have: lack of financial assets, limited access to financing and credit, struggle with cash flow, and inadequate risk management. World Economic Forum (2022) also sees financial limitations for SMEs and less access to formal financing (long-term loans). SMEs frequently view access to finance as one of the major obstacles keeping them from operating effectively in both developed and developing nations. SMEs tend to be more financially fragile, have smaller cash buffers, weaker supply chain capabilities, and lower uptake of digital tools and technologies.

Bhattacharyya and Kumar (2022) find a positive relationship between the expenditure of SMEs on corporate social responsibility (CSR). They conclude that CSR expenditure by SMEs is perceived positively by major clients and hence contributes to improved future sales value. Also, CSR spending is viewed favorably by suppliers of debt capital. In the absence of a universal federal CSR law, U.S. companies are engaging in voluntary CSR practices due to stakeholder expectations. The findings that CSR expenditure leads to improved sales and better access to finance may not (yet?) directly apply to U.S.-based SMEs since they were not part of the research.

To deal with the challenging environment and to contribute to a more sustainable economy, SMEs could profit from the expertise of financial planners. We see a new field of financial advice for SMEs arising from financial business planning.

Financial Business Planning as a Seperate Profession

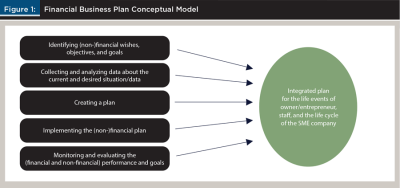

Our conceptual model of financial business planning (FBP) includes identifying financial/non-financial wishes and objectives, collecting and analyzing the current and desired situation/data, developing an integral business plan, implementing a financial/non-financial integral plan, and monitoring and evaluating financial/non-financial performance to ensure that a life cycle strategy (business cycles: start up, scale up [investments], growth financing [cash flow], acquisition financing, business termination) achieves the objectives of a company. “Non-financial” can be seen as the client’s values.

FBP can also create sustainable business models for advisers. De Jong and Oerlemans (2018) have described a sustainable business model for the adviser in the private market, acting as the financial director. This director continuously deals with all financial issues of a household, including insurance, credits, taxes, investments, and budget management. You could think of this as a “private CFO.” The financial business planner is an adviser who can manage and advise on all financial issues (private and business) of an entrepreneur, their company, and their employees. The financial business planner can best be compared to a health center that houses multiple disciplines and where a general financial practitioner (from their own specialty) can refer to other specialists. Financial management for SMEs is a coordinated approach to issues within a company relating to taxation, risks, financing, accountancy, strategy, HRM, asset accumulation, pensions, and (personal or private) financial planning, with an explicit connection to the financial position of the entrepreneur and staff. This coordinated approach requires specific knowledge and skills to realize dreams and to prevent nightmares as much as possible.

De Jong and Van Kooten (2019) note that the financial advice market for SMEs is a compartmentalized market with insufficient coherence. The range of financial advice on offer does not match the financial challenges within SMEs. This advice gap needs to be filled, and for this reason financial advice to SMEs must be presented as a separate profession. A separate profession requires multidisciplinary training of knowledge and especially skills, certification, and possibly (self-)regulation. But it starts with a clear vision of the financial advice market on its role in the transition to a sustainable economy. FBP is necessary to be able to solve fragmentation and pillars of advice. Business decisions will influence personal choices, and that also has an impact on the employees and vice versa. FBP is a process in which an entrepreneur or an organization makes an integrated plan to achieve their financial and non-financial ambitions/goals. This includes identifying financial and non-financial ambitions/goals, assessing the current (financial) situation, developing a strategy (opportunities and challenges) to achieve these goals, and monitoring progress and any adjustments to the integrated plan. Financial (business) planning is intended to achieve optimal (cash) flow over the entire life cycle (company and SME) based on a dashboard. The result is a financial business plan (FB-plan) that functions as a dashboard on which all important aspects of the company and personal financial strategies come together clearly. This plan unites separate forms of advice from various professionals into one and offers strategic guidance for the entrepreneur, the company, and the employees.

The FB-plan combines fiscal and financial optimization with key elements like personnel policy, sustainability, and long-term strategy. It provides a structured framework for aligning financial and non-financial goals, ensuring business growth and workforce satisfaction.

The FB-plan starts by defining actionable goals, such as pension accrual, tax optimization, and sustainability, alongside broader objectives like work-life balance and business succession, including Porter and Kramer’s (2011) shared value concept (more synergy between profitability and social value) and Lazear’s (1995) work on employment conditions emphasizes aligning business strategies with societal needs and workforce loyalty. These goals should include the values of the entrepreneur as well as the company itself and not focus on only number crunching.

Analyzing finances, cash flow, and workforce dynamics is critical. High turnover linked to inadequate benefits, for example, can be addressed with targeted improvements like enhanced employee packages, boosting retention and satisfaction.

Balancing financial objectives with employee-focused initiatives—such as tax-efficient investments and flexible pensions—creates growth opportunities and workforce loyalty. Scenario planning, as outlined in Schoemaker’s (1995) work, ensures adaptability for challenges like succession or market shifts. Advisers and digital tools play a key role in integrating these strategies effectively.

Developing an education (and master’s) program focused on SME financial and business planning can equip professionals to implement FB-plans. Drawing on behavioral finance (Thaler 2015) and practical applications like tax strategies, such programs ensure expertise. Research through financial planning institutes can further explore outcomes, such as how sustainability investments drive profitability.

Simplified tools and targeted education are essential for making FB-plans accessible, addressing challenges like complexity and cost. By integrating fragmented advice into cohesive strategies, entrepreneurs can achieve financial stability and operational flexibility. Education-backed advisers can bridge knowledge gaps, making the FB-plan a cornerstone for SME success and resilience in a changing landscape.

Figure 1 shows the conceptual model and different steps needed. CFP® professionals will recognize the CFP Board for the formulated steps of the financial planning process.

A Logical Next Step to Earlier Successful Concepts?

The financial business plan is a logical step for financial planners and SMEs, especially when they have experience working with the business model canvas (Osterwalder and Pigneur 2010). The business model canvas is a helpful instrument for mapping out on a strategic thinking level the company in all aspects. Another earlier example is, of course, the Rich Dad’s cash flow quadrant by Robert Kiyosaki (1998). The benefit from working with SME owners and entrepreneurs is that goalsetting most of the time is already top of mind. Goals are very common in business environments: turnover (yearly growth, quarterly realizations), profits, number of clients, etc. Building on the business model canvas, there is a new development to integrate sustainable development into the business model, the triple-layered business model canvas (Van Stratum 2024). This instrument adds an ecological and social layer upon the traditional business model canvas to analyze the potential social and ecological value of a company. For financial business planners, this is an interesting starting point for their holistic advice on sustainability to SMEs.

B Corps as Inspiration for Financial Business Planners

For financial planners to become financial business planners, the focus should not only be on reaching financial goals, but also on reaching sustainability goals. An interesting method to do that is the B Corp certification.

A Certified B Corporation, or B Corp, is a for-profit company that meets high standards of social and environmental performance, accountability, and transparency. Certified by the nonprofit B Lab, B Corps commit to balancing profit with purpose, considering the impact of their decisions on all stakeholders, including workers, customers, suppliers, community, and the environment. As of 2025, over 9,500 companies across 102 countries have achieved B Corp certification.3

In recent years, the financial planning and wealth management sector in the United Kingdom and the United States has seen a notable increase in firms attaining B Corp status. This trend reflects a growing commitment within the industry to integrate ethical practices and sustainability into financial services. B Corp certification has, to date, been primarily associated with sectors such as retail, technology, and manufacturing. Globally recognized companies that have obtained B Corp status—some perhaps unexpectedly—include Ben & Jerry’s, Patagonia, Coursera, Kickstarter, Danone, Tony’s Chocolonely, TOMS, and Dopper. In the United States, there are currently 2,989 certified B Corporations across different industries.

The United Kingdom has emerged as a global leader in the B Corp movement. London alone hosts over 1,000 B Corps, making it the city with the highest concentration of certified companies worldwide. The United Kingdom is now home to more than 500 certified B Corporations operating within the financial services sector. This figure is particularly notable when considered in the context of the total number of B Corps in the United Kingdom, which stands at just over 3,300.

CERTIFIED FINANCIAL PLANNERS® are particularly well-suited to integrating B Corp principles into their practice. Their training emphasizes a holistic approach to financial planning, considering clients’ values and long-term goals. This aligns with the B Corp focus on stakeholder impact and sustainability (Paelman et al. 2021). In contrast, CPAs often concentrate on accounting and auditing, with less emphasis on integrating social and environmental considerations into business planning. The B Corp certification represents more than a quality label; it is a cultural, social, and environmental commitment with some doubts about the economic benefits (Patel and Dahlin 2022). For firms engaged in wealth management and financial planning, it offers a meaningful opportunity to differentiate themselves in an industry traditionally characterized by conservatism yet increasingly undergoing structural and ideological transformation. For financial business planners, a B Corp certification can help in multiplying the value of financial advice.

Of relevance is the recent news from George Kinder, widely regarded as the founder of the life planning movement, to relocate from Massachusetts to the United Kingdom.4 Among the factors influencing his decision—besides acquiring a special innovation visa—is the dynamic and growing ecosystem of B Corp-certified organizations in the United Kingdom, which he intends to engage with further. By aligning with B Corp principles, financial planners can position themselves as progressive actors—agents of change in a context where financial decisions are increasingly intertwined with ethical values and societal impact. The rise of B Corp-certified financial firms reflects a broader movement within the industry to prioritize ethical practices and sustainability. As more clients seek advisers who align with their values, the trend toward B Corp certification among financial planners and wealth managers is likely to continue growing. It is a clear signal that in both curriculums of CFP® professionals and CPAs, there is a gap that can be filled by business planning focusing on SMEs’ business, how it is done, what can be improved, optimizing processes, etc., in a similar way that a B Corp does.

Sustainability Considerations for Financial Planners

For financial planners, the sustainability challenges of SMEs can create a business opportunity, but only if financial planners take sustainability considerations into account when they advise SMEs.

Sustainable investing. Research from Friede et al. (2015) indicates that companies excelling in sustainability often achieve better financial results. Sustainable investments can thus be both ethically responsible and financially rewarding. There is often a misunderstanding that the returns from sustainable investing are lower, but this is not evident from these studies. Studies show that the returns from sustainable investments are equal to or, in some cases, higher than those from non-sustainable investments.

Risk management. Incorporating ESG practices can significantly reduce risks for SMEs by lowering reputational damage and ensuring compliance with current and future regulations. Additionally, by proactively addressing ESG issues, SMEs are better prepared for future legislation and can avoid costly fines, lawsuits, or disruptions related to non-compliance. Ultimately, adopting ESG principles not only mitigates risks but also positions companies for long-term sustainability and competitive advantage.

Reputation and customer loyalty. Consumers and business partners increasingly value sustainability. Sustainable companies can enhance their reputation and build stronger customer loyalty, which has a positive effect on their revenue. Companies that embrace ethical practices are less likely to face negative publicity or consumer backlash, which can harm their brand.

Futureproofing. Sustainable companies can benefit from the growing market for sustainable products and services. It can drive innovation and open new growth opportunities, strengthen competitive positions, and enable entry into new markets.

Employee pensions. Employees are becoming increasingly aware of sustainability and are therefore asking questions about it. Employees may wonder where the money in their pension plans is being invested. They often do not want the money to be invested in certain sectors, such as tobacco or gambling. Sustainable investments therefore exclude these sectors, which is known as a negative approach. Due to the MiFID5 Regulation Framework in Europe, investment advice offered to clients requires the adviser to offer and discuss the possibility of ESG investments as another option besides the traditional investment and portfolio approach as part of the investment decision process. In a positive approach, the most sustainable companies are actively sought out. Well-known strategies that a fund may use in this context include ESG integration, best-in-class, and impact investing. An SME should therefore engage in discussions with the manager of its pension plans and inquire whether the fund applies sustainability strategies such as exclusion and ESG integration to make the pension plan more sustainable. U.S.-based clients with these kind of wishes or exclusions have for many decades typically expressed them in writing in the investment policy statement. This new but different approach in Europe is the total opposite of what is happening in the United States right now and is challenging for fiduciaries who, acting on behalf of their clients, will be forced to act in opposite directions by the different laws.

Conclusion

Sustainability is a major challenge for SMEs, especially in a rapidly changing and complex environment. The role of financial advisers can be significant in reaching sustainability goals. Combining the values of financial planning and business advice, a new approach to financial advice for SMEs is introduced here: financial business planning. This vision could lead to a new type of financial adviser who combines the principles of financial planning with sustainable business consulting. To integrate these fields, the best of both worlds’ approach, further research is necessary. Our research leads to new questions like how to integrate financial planning education with business consultancy, which specific knowledge and competencies a financial business adviser must have, what SMEs expect in detail from a financial business planner, and how a financial business plan should look like exactly. Also, research should be done into the demand for a separate financial business planning profession. In this article, the case for financial business planning as an enrichment for the financial planning society is made, with the outlines of a new conceptual model of advice for SMEs. With this article, the authors want to inspire financial planners and advisers to act more on their social responsibility and especially encourage them to help SMEs with their complex challenges so financial planners and advisers can really become pioneers and agents of change for sustainability.

Endnotes

- See https://news.un.org/en/story/2023/07/1138777.

- World Economic Forum. 2022, November. Future Readiness of SMEs and Midsized Companies, a Year On. Insight Report.

- See www.bcorporation.net.

- See www.wealthbriefing.com/html/article.php/%22life-planning%22-thought-leader-swaps-massachusetts-for-uk#:~:text=Prominent%20financial%20planning%20figure%20George,Kinder%20an%20Innovator%20Founder%20Visa.

- See https://eur-lex.europa.eu/eli/dir/2014/65/oj/eng.

References

Alexiev, A. S., J. J. P. Jansen, F. A. J. van den Bosch, and H. W. Volberda. 2010. “Top Management Team Advise-Seeking and Exploring Innovation: The Moderating Role of TMT Heterogeneity.” Journal of Management Studies 47 (7): 1343–1364.

Alhabeeb, M. J. 2015. Entrepreneurial Finance. Hoboken, New Jersey: John Wiley & Sons.

Bello, H. O., C. Idemudia, and T. V. Iyelolu. 2024. “Navigating Financial Compliance in Small and Medium-Sized Enterprises (SMEs): Overcoming Challenges and Implementing Effective Solutions.” World Journal of Advanced Research and Reviews 23 (01): 42–55.

Bhattacharyya, A., and A. Kumar. 2022. “Corporate Social Responsibility and SME Value Creation.” Australasian Accounting, Business and Finance Journal 16 (6): 45–69.

Bosse, C. K., and K. J. Zink. 2019. Arbeit 4.0 im Mittelstand. Chancen und Herausforderungen desdigitalen Wandels für KMU. Springer Gabler.

Cummins, J. D., and N. A. Doherty. 2006. “The Economics of Insurance Intermediaries.” Journal of Risk & Insurance 73 (3): 359–396.

D’Amboise, G., and M. Muldowney. 1988. “Management Theory for Small Business: Attempts and Requirements.” Academy of Management Review 13: 226–240.

De Jong, F., and K. Wagensveld. 2023. “Sustainable Financial Advice for SMEs.” Journal of Circular Economy and Sustainability 4: 777–789.

De Jong, F., and A. Oerlemans. 2018. “De Financieel Regisseur als Oplossing voor de Maatschappelijke Uitdaging van Financiële Zelfredzaamheid.” Het Verzekeringsarchief 95 (2): 92–101.

De Jong, F., and M. Van Kooten. 2019. “Financieel Gezond MKB Vereist een Integrale en Multidisciplinaire Adviesbenadering.” Het Verzekeringsarchief 96 (3).

Friede, G., T. Busch, and A. Bassen. 2015. “ESG and Financial Performance: Aggregated Evidence from More than 2000 Empirical Studies.” Journal of Sustainable Finance & Investment 5 (4): 210–233.

Gherghina, S. C., M. A. Botezatu, A. Hosszu, and L. N. Simionescu. 2020. “Small and Medium-Sized Enterprises (SMEs): The Engine of Economic Growth through Investments and Innovation.” Sustainability 12 (347).

Godos-Díez, J., L. C. García, D. Alonso-Martinez, and R. Fernandez-Gago. 2018. “Factors Influencing Board of Directors’ Decision-Making Process as Determinants of CSR Engagement.” Review of Managerial Science 12: 229–253.

Hamid, S. 2019. “The Strategic Position of Human Resource Management for Creating Sustainable Competitive Advantage in the VUCA World.” Journal of Human Resources Management and Labor Studies 7 (2): 1–4.

Kádárová, J., L. Lachvajderová, and D. Sukopová. 2023. “Impact of Digitalization on SME Performance of the EU27: Panel Data Analysis.” Sustainability 15 (9973).

Kiyosaki, R. 1998. Rich Dad’s Cashflow Quadrant, Guide to Financial Freedom. Plata Publishing.

Lazear, E. P. 1995. Personnel Economics. MIT Press.

Masurel, E., and I. A. W. van Rijn. 1993. “Ondernemingsplanning Door Het MKB in de Zakelijke Dienstverlening.” MAB (maart): 108–115.

Nkwinika, E., and S. Akinola. 2023. “The Importance of Financial Management in Small and Medium-Sized Enterprises (SMEs): An Analysis of Challenges and Best Practices.” Technology Audit and Production Reserves 5 (4): 12–20.

Osterwalder, A., and Y. Pigneur. 2010. Business Model Generation: A Handbook for Visionaries, Game Changers, and Challengers. Wiley.

Overton, R. H. 2008. “Theories of the Financial Planning Profession.” Journal of Personal Finance 7 (1).

Oyewole, A. T., O. B. Adeoye, W. A. Addy, C. C. Okoye, and O. C. Ofodile. 2024. “Enhancing Global Competitiveness of U.S. SMEs through Sustainable Finance: A Review and Future Directions.” International Journal of Management & Entrepreneurship Research 6 (3): 634–647.

Paelman, V., P. Van Cauwenberge, and H. Van Bauwhede. 2021. “The Impact of B Corp Certification on Growth.” Sustainability 13 (13): 7191.

Patel, P., and K. Dahlin. 2022. “The Impact of B Corp Certification on Financial Stability: Evidence from a Multi-Country Sample.” Business Ethics, the Environment & Responsibility 31 (1): 177–191.

Porter, M., and M. Kramer. 2011. “Creating Shared Value.” Harvard Business Review 89 (1/2): 62–77.

Robinson Jr., R. B. 1982. “The Importance of ‘Outsiders’ in Small Firms Strategic Planning.” Academy of Management Review 25: 80–93.

Scheinpflug, R., and K. Stolzenberg. 2017. Neue Komplexität in Personalarbeit und Führung. Herausforderungen und Lösungsansätze. Springer Gabler.

Schoemaker, P. J. H. 1995. “Scenario Planning; A Tool for Strategic Thinking.” Sloan Management Review 36: 25–40

Thaler, R. H. 2015. Misbehaving: The Making of Behavioral Economics. Norton & Company, Incorporated, w. w.

Van Stratum, S. 2024. The Triple Layered Business Model Canvas in Practice. Floot.

Verkuil, A. H. 2024. Start-up Cultures in Times of Global Crises, Sustainable Business Development. Springer Cham

Warschauer, T. 2002. “The Role of Universities in the Development of the Personal Financial Planning Profession.” Financial Services Review 11: 201–216.

Williamson, O. E. 1975. Markets and Hierarchies, Analysis and Antitrust Implications: A Study in the Economics of Internal Organization. New York: Free Press.

World Economic Forum. 2022, November. Future Readiness of SMEs and Midsized Companies, a Year On. Insight Report.