Journal of Financial Planning: March 2026

NOTE: Please be aware that the audio version, created with Amazon Polly, may contain mispronunciations.

Executive Summary

- Major banks are now utilizing artificial intelligence (AI) platforms, and more consumers are using them, making technology’s effect on financial outcomes a key concern for advisers.

- Utilizing the 2024 National Financial Capability Study, the analysis showed that the relationship between mobile technology and financial wellness differed significantly based on client attitudes toward AI. For clients who were open to AI, the relationship was positive, while for clients who were skeptical of AI, the relationship was negative.

- Analysis revealed technology benefits concentrate among lower-income populations. Those who showed AI interest (interested in receiving financial advice from AI) and used mobile fintech had the strongest associations among lower-income households. This suggests that technology could help close, not widen, financial gaps.

- Results showed mobile banking serves as a gateway to AI acceptance. Advisers can use this sequential pattern by encouraging clients to adopt mobile banking first, as increasing familiarity with digital tools can enhance receptivity to AI-based financial applications.

- These findings can guide financial advisers to decide which digital tools to recommend to clients with lower incomes by looking at their attitudes toward AI first. Clients with lower incomes who were open to AI had the best chance of getting better results.

Lena Gan, Ph.D., CFP®, CIMA, has over 20 years of experience in the financial services industry. She holds a Ph.D. in personal financial planning from Kansas State University and was a 2023 research fellow at the National Endowment for Financial Education (NEFE). Her research focuses on technology’s impact on financial planning outcomes and client behavior.

Dr. Karleah Harris is an associate professor at the University of Arkansas at Pine Bluff. She received her Ph.D. in educational psychology at Purdue University. Her research focuses on financial inclusion, using inquiry-based science learning to study kindergarten students’ explanations, the types of discourse strategies teachers use during classroom science discourse, children with learning disabilities, culturally responsive teaching, horticultural therapy, grandparenting, food deserts, food insecurity, and gardening.

Sara Kay is a site reliability engineer and an M.S. candidate in business analytics at Carnegie Mellon University, expecting to graduate in May 2026. She specializes in data infrastructure, compliance automation, and building tools that eliminate manual processes. She has previously worked at PNC, Bank of America, and Moody’s Analytics. Her research focuses on practical applications of AI in consumer analytics and survey methodologies to help uplift marginalized communities.

NOTE: Click on the images below for PDF versions.

Financial technology adoption is accelerating rapidly across consumer markets. Recent data reveals that over 37 percent of the U.S. population now engage with bank chatbots—with usage projected to reach 110.9 million by 2026—while all top 10 commercial banks deploy artificial intelligence (AI)-powered tools that consumers increasingly use for advice on credit cards, mortgages, and investment decisions (CFPB 2023; Roy et al. 2025).

The challenge grows more complex when clients layer multiple technologies together. Consumer complaints to the CFPB reveal that many clients get trapped in “doom loops” with financial chatbots, unable to reach human advisers when automated systems fail to address their needs (CFPB 2023). Meanwhile, acceptance of and satisfaction with financial technologies vary significantly by income and education levels (Gomber et al. 2017; Jung et al. 2018; Roy et al. 2025), suggesting that technology relationships are conditional rather than universal. This creates a critical blind spot: while research consistently demonstrates that financial knowledge, confidence, and behaviors are associated with financial outcomes (Xiao and Porto 2022; Xiao and Kim 2022; Xiao et al. 2022), the interaction between client technology use and these fundamental capabilities remains largely unknown. For practitioners, this means traditional financial planning strategies may fail when clients rely heavily on technologies that operate outside their oversight.

Using the 2024 National Financial Capability Study, we examine how AI interest and mobile fintech usage changed the established relationship between financial capability and financial wellness across different population segments. This research provides financial practitioners with the first systematic analysis of when client technology use enhances or undermines the capability–wellness relationship, offering actionable guidance for navigating AI implementation while addressing whether these tools help close or widen existing financial outcome gaps.

Literature Review

Financial advisers face an unprecedented challenge: how do you help clients achieve financial wellness when they’re increasingly using AI tools and mobile apps that operate outside your guidance? Research consistently shows that financial capability, including knowledge, confidence, and behaviors, is associated with better financial outcomes like higher savings rates, improved retirement readiness, and reduced financial stress (Lusardi and Mitchell 2014; Xiao and Kim 2022). However, this relationship now operates in a digital environment where client technology use may fundamentally change how financial skills translate into actual wellness.

Financial Wellness and Capability

Financial wellness represents the ultimate goal for practitioners and their clients. Huston’s (2015) Financial Health Model conceptualizes wellness as a continuous production process requiring awareness, education, habituation, and ongoing examination and adjustment. This process-oriented definition aligns with empirical research on subjective financial wellness, which emphasizes perceptions of security, satisfaction, and resilience rather than objective metrics alone (Anvari-Clark and Ansong 2022; Cook et al. 2025; Gerrans et al. 2014). For instance, Gerrans et al. (2014) found that financial literacy was positively associated with financial behavior and satisfaction, with notable gender differences influencing how financial status and knowledge impacted overall financial wellness and quality of life. This process-oriented view helps explain why technology tools must match where clients are in their financial health journey rather than offering one-size-fits-all solutions.

Financial capability serves as the foundation for achieving wellness. Xiao and Kim (2022) define it as the individual ability to apply appropriate financial knowledge and engage in desirable financial behaviors for achieving financial wellness. This framework encompasses four interconnected components: objective financial knowledge (factual understanding of financial concepts), subjective financial knowledge (perceived financial competence), financial confidence (belief in decision-making abilities), and desirable financial behaviors (tangible actions like budgeting and saving). For practitioners, this framework suggests that enhancing client outcomes requires developing all four capability dimensions, not just knowledge transfer through traditional financial education. Empirical research consistently demonstrates that higher financial capability is related to improved wellness outcomes, with studies showing that financial capability’s effects on financial stress are substantially larger than negative effects of financial difficulties (Xiao and Kim 2022; Lusardi and Mitchell 2014).

Technology’s Role in Financial Planning

Client technology adoption follows predictable patterns that affect financial planning outcomes. Research shows that technology acceptance depends on whether users find tools useful and easy to use, with significant differences across age, income, and education levels (Davis 1989; Venkatesh and Davis 2000). In financial contexts, these patterns create both opportunities and challenges for advisers. Brenner and Meyll (2020) demonstrate that technology can either substitute for or complement human financial advice depending on user characteristics and implementation approaches. Similarly, Jung et al. (2018) found that robo-adviser effectiveness varies significantly based on user demographics and technology engagement patterns, supporting the conditional rather than universal nature of technology benefits. AI interest and mobile fintech adoption can also vary significantly by socioeconomic demographics with younger, higher-educated, and often paradoxically lower-income users showing stronger adoption patterns (Addy et al. 2024; Carlin et al. 2017), suggesting these technologies may affect the capability–wellness relationship differently across demographic groups rather than universally enhancing outcomes.

Two specific technologies illustrate these dynamics. Mobile fintech usage captures active engagement with digital financial tools, while AI advice interest reflects openness to algorithmic decision support. Research reveals that mobile fintech engagement serves as a gateway technology facilitating AI adoption (Roy et al. 2025), with this sequential relationship suggesting synergistic rather than independent effects on financial outcomes. However, technology effects are not universal. Meta-analytic evidence confirms these differential adoption patterns, with comprehensive reviews showing that fintech acceptance models vary significantly across demographic groups (Shaikh et al. 2020; Tam and Oliveira 2017). Cross-country research demonstrates that fintech adoption particularly benefits lower-income populations in terms of financial inclusion outcomes (Frost 2020), though efficiency gains from fintech implementation may not uniformly translate to user benefits across all income segments (Philippon 2016). These studies suggest that some clients benefit from digital tools while others experience reduced financial capability development when they rely too heavily on automation.

While research establishes both the capability–wellness relationship and different technology adoption patterns (defined as ways of how people use technology), no studies have examined whether technology factors changed this fundamental relationship or whether technology’s impact varies across socioeconomic groups. This research gap limits practitioners’ ability to provide technology-informed guidance on when to encourage versus limit client technology adoption.

Informed by prior literature, we test the following hypotheses:

H1: Financial capability will be positively associated with financial wellness, establishing the foundational relationship for subsequent moderation analyses.

H2: Interest in getting financial advice from AI will change the relationship between financial capability and financial wellness.

H3: Mobile fintech usage will change the relationship between financial capability and financial wellness.

H4: Interest in getting financial advice from AI and mobile fintech usage will interact synergistically, with their combination showing different associations than when examined individually in the relationship between financial capability and financial wellness.

H5: The combined technology effects (interaction of AI interest and mobile fintech use) will vary across socioeconomic groups, with stronger patterns among lower socioeconomic populations.

Methodology

Sample

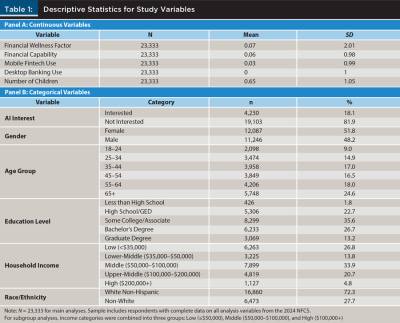

The data came from the 2024 National Financial Capability Study (NFCS), a nationally representative survey of American financial capability conducted every three years by the FINRA Investor Education Foundation since 2009. The NFCS uses quota sampling by age, gender, income, ethnicity, and education to ensure the sample represents the U.S. population. The initial dataset contained 25,539 respondents. After removing cases with missing data on key variables, the final sample included 23,333 respondents (91.4 percent retention rate). Population weights were applied following FINRA’s established methodology.

Measures

Financial wellness. Financial wellness served as the outcome variable, measured using four indicators consistent with subjective financial wellness research (Anvari-Clark and Ansong 2022; Huston 2015; Prawitz and Cohart 2016; Joo 2008): financial satisfaction (1–10 scale), ease of paying bills (1–3 scale), money left over at month end (1–5 scale), and confidence in accessing $2,000 for emergencies (1–4 scale). These four measures were combined into a single financial wellness score using confirmatory factor analysis, which showed excellent model fit and explained 86 percent of the variance in responses and was in line with capturing individuals’ perceptions of their financial wellness. The factor scores were then used in all subsequent analyses.

Financial capability. Following Xiao and Kim’s (2022) validated framework, financial capability was measured using four components: objective financial knowledge (six knowledge questions), subjective financial knowledge (perceived competence, 1–7 scale), financial self-efficacy (belief in decision-making abilities, 1–7 scale), and desirable financial behaviors (six actions like budgeting and saving). The financial self-efficacy component follows Lown’s (2011) approach to measuring confidence in financial decision-making abilities. Each component was first converted to a standardized scale (M = 0, SD = 1), then the four standardized scores were summed to create the financial capability index. Survey weights were applied consistently throughout all analyses using FINRA’s established weighting methodology.

Interest in AI financial advice. This study capitalized on a novel question introduced for the first time in the 2024 NFCS: “Would you be interested in getting financial advice from AI (artificial intelligence)?” This represents the first large-scale, nationally representative measurement of consumer AI advice interest. Responses were coded as 1 = Yes and 0 = No.

Mobile fintech usage. Mobile fintech use was measured using four behaviors: mobile banking frequency, mobile payment usage, mobile money transfers, and financial app utilization, consistent with technology adoption research in financial contexts (Davis 1989; Venkatesh and Davis 2000). Each used a 3-point scale (never, sometimes, frequently). The four measures were averaged and standardized for analysis.

Control variables. Demographic controls included age, gender, race/ethnicity, education, household income, employment status, marital status, and number of dependent children. Previous research has found these factors significantly influence both financial capability and technology adoption (Addy et al. 2024; Carlin et al. 2017; Demirgüç-Kunt et al. 2018). Desktop banking usage was included to separate mobile-specific effects from general online banking behavior.

Analytical strategy. Analysis proceeded through sequential model building following established interaction testing protocols (Aiken and West 1991; Hayes 2017). Stage one tested direct effects (H1), stage two added two-way interactions (H2–H3), and stage three incorporated three-way interactions (H4). Model comparison used R², AIC, and BIC statistics to assess incremental explanatory power. Subgroup analyses (H5) examined interaction effects across income (low £$50,000, middle $50,000–$100,000, high $100,000+), education (high school or less, some college, college degree or above), and racial groups. All continuous variables were standardized prior to creating interaction terms to facilitate interpretation. Average marginal effects analysis was conducted to quantify how financial capability effectiveness varies across technology contexts, providing practical interpretation of complex three-way interactions. All analyses were conducted in Stata 18 using robust standard errors.

Results

Descriptive Statistics

The final analytical sample contained 23,333 respondents representative of the U.S. adult population. Overall, 18.1 percent of respondents expressed interest in receiving financial advice from AI. AI-interested individuals were more likely to be male (22.3 percent versus 13.4 percent for females), younger (with interest declining from 26.9 percent among 18–24-year-olds to 5.6 percent among those 65+), and from minority backgrounds (27.3 percent versus 13.7 percent for White non-Hispanic respondents). Notably, AI interest showed minimal variation across income and education levels, suggesting broad demographic appeal rather than concentration among high-income or highly educated populations. See table 1.

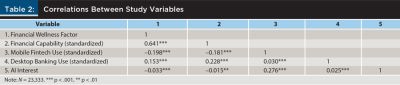

Correlation analysis. Counterintuitive patterns motivated our hypotheses testing. Mobile fintech use showed negative correlations with both financial wellness (r = –0.20) and financial capability (r = –0.18), suggesting potential overreliance where technology substitutes for rather than complements financial skills. However, mobile fintech use demonstrated a strong positive correlation with AI interest (r = 0.28), confirming that mobile engagement serves as a gateway to AI acceptance. Financial capability and financial wellness showed the expected strong positive correlation (r = 0.64), establishing the foundational relationship for subsequent analyses. See table 2.

Main Analyses

Financial capability and wellness association. Financial capability demonstrated a strong positive association with financial wellness (β = 1.318, p < .001), supporting H1. This relationship explained 41.1 percent of variance, confirming financial capability as having the strongest association with wellness outcomes.

Technology moderation effects. AI interest alone did not significantly change how financial capability relates to wellness (β = –0.039, p = .095), failing to support H2. However, clients who used mobile fintech more frequently showed a weaker relationship between capability and wellness (β = –0.034, p < .001), supporting H3. Higher mobile technology adoption was associated with lower benefits from financial capability, suggesting overreliance mechanisms.

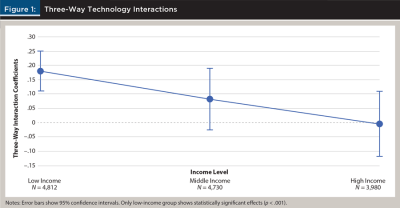

Three-way technology interactions. When we examined AI interest and mobile fintech use together, they created a significant combined relationship (β = 0.085, p = .002), supporting H4. This finding reveals how AI attitudes change the role of mobile technology. Among clients without AI interest, higher mobile use was associated with weaker financial capability benefits. However, among AI-interested clients, mobile use was associated with stronger capability benefits. This complete reversal provides clear guidance for practitioners—assess client AI attitudes before recommending mobile strategies. See figure 1.

Model comparison. Testing increasingly complex models confirmed that AI interest and mobile use must be examined together rather than separately. The combined model (R² = 0.420) demonstrated better fit than simpler models (DR² = 0.009, p < .01), indicating that technology recommendations should account for both factors simultaneously. See table 3.

Technology gateway effects. Logistic regression analysis revealed that mobile fintech use was positively related with AI advice interest. A one-standard-deviation increase in mobile fintech use was associated with a 10.4 percentage point higher probability of AI interest (AME = 0.104, SE = 0.002, p < .001). This sequential pattern has important practical implications for advisers. Clients who become comfortable with mobile banking are significantly more likely to accept AI-powered financial tools later. Financial advisers can use this progression strategically—start by helping hesitant clients adopt basic mobile banking features, then gradually introduce AI-enhanced budgeting or investment tools once they’re comfortable with mobile technology.

Income group differences. Subgroup analyses revealed striking patterns supporting H5. Low-income households (£$50,000) was associated with stronger technology synergies (β = 0.181, p < .001), while middle ($50,000–$100,000) and high-income ($100,000+) groups demonstrated a weaker or non-significant relationship (β = 0.082, p = .141; β = –0.004, p = .950). This concentration of benefits among lower-income populations suggests strategic technology deployment could help close rather than widen financial outcome gaps.

Robustness checks confirmed finding stability across alternative specifications, bootstrap procedures, and outlier treatments, indicating relationships were consistent rather than dependent on specific analytical choices.

Discussion

Using data from the 2024 NFCS, we examined how client AI attitudes and mobile technology use affect the relationship between financial capability and wellness. Results confirmed that financial capability is associated with higher wellness outcomes, consistent with extensive research showing that financial knowledge, confidence, and behaviors improve client outcomes (Lusardi and Mitchell 2014; Xiao and Kim 2022). However, technology effects proved more complex than expected, challenging assumptions that digital tools universally help clients.

Our most important finding shows how client attitudes toward AI fundamentally change the role of mobile technology: the relationship between mobile technology and financial wellness differed significantly based on whether clients were open to or skeptical of AI. Among clients who weren’t interested in AI advice, higher mobile app use was associated with weaker financial capability benefits. However, among clients open to AI advice, mobile use was associated with stronger capability–wellness relationships. This complete reversal shows that client attitudes actively shape how technologies relate to financial outcomes, not just whether clients adopt new tools (Venkatesh and Davis 2000).

The finding that mobile technology use alone was associated with weaker financial outcomes suggests potential overreliance, where heavy app use is associated with weaker personal financial skill development. This weakening pattern may reflect automation bias, where individuals defer financial decisions to technology without engaging in the critical thinking necessary for skill development (Goddard et al. 2012). When clients passively rely on apps to track spending or make recommendations, they miss opportunities to build financial intuition and problem-solving skills that come from actively managing their finances. Additionally, cognitive offloading—using external tools as substitutes rather than supplements for mental effort—may explain why heavy mobile users without AI interest show weaker capability benefits (Risko and Gilbert 2016). For these clients, technology becomes a crutch that replaces rather than enhances their financial decision-making processes. This counterintuitive result aligns with research showing technology effects vary across different groups (Khan et al. 2025) and challenges assumptions that digital tools always help. In contrast, AI interest alone showed no effect, suggesting that attitudes must combine with actual technology use to influence outcomes.

We also confirmed that mobile technology serves as a stepping stone to AI acceptance. Each increase in mobile use was associated with higher AI interest by 10.4 percentage points, explaining why mobile proficiency and AI receptiveness work together rather than independently.

However, these technology interactions didn’t affect all clients equally. When we examined different income groups, we found striking patterns that have important implications for financial advisers working with diverse populations. The combined pattern of AI interest and mobile use explains an additional 0.9 percent of variance in financial wellness. While this percentage sounds small, it answers a critical question for advisers: Does mobile technology help or hurt the client? This distinction matters when deciding which digital tools to recommend. Among lower-income clients, this pattern had a stronger relationship (3 percent additional variance), making it especially important for advisers working with financially vulnerable clients. With over 100 million Americans now using mobile banking, understanding these patterns has broad practical implications. Low-income households showed the strongest association with technology benefits, while middle and high-income groups demonstrated weaker or no patterns. This income gradient suggests that rather than primarily helping already-advantaged clients, thoughtful technology implementation may actually help close existing financial gaps. This finding contradicts concerns that AI adoption would mainly benefit wealthy clients and instead suggests technology could serve as an equalizing force when deployed appropriately.

In sum, results from our study show that technology’s role in financial planning goes beyond simple substitution or complementarity. Technology effects depend critically on client attitudes, usage patterns, and income levels, with digital tools amplifying capability benefits when clients approach them strategically rather than passively. The concentration of benefits among traditionally underserved populations suggests targeted technology deployment could help level the playing field in financial services.

Implications

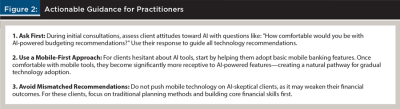

Because client attitudes toward AI fundamentally determine whether technology enhances or undermines financial outcomes, practitioners should assess technology preferences before recommending digital tools. Results showed that mobile fintech usage is associated with a weaker capability–wellness relationship among AI-skeptical clients but strengthens it among those interested in AI financial advice. Financial advisers can evaluate client openness to AI through simple questions during initial consultations, such as asking about current app usage or comfort with automated financial features. For AI-receptive clients, advisers should encourage strategic adoption of mobile banking apps, budgeting tools like Mint or YNAB, and robo-adviser platforms that complement their financial planning process.

Technology benefits concentrate among lower-income populations, suggesting targeted implementation strategies can help close financial outcome gaps. Advisers working with clients earning under $50,000 should prioritize mobile-first approaches, recommending free financial apps and demonstrating how to access AI-powered budgeting assistance through their existing bank platforms. For higher-income clients, technology serves a supplementary role to traditional planning methods. Practitioners should focus on integrating AI tools for data analysis and portfolio monitoring rather than basic financial management.

Sequential technology adoption, defined as step-by-step technology use, is associated with providing opportunities for gradual client engagement. Mobile banking serves as a gateway to AI acceptance, with each increase in mobile usage associated with over 10 percentage points higher AI interest. Advisers can leverage this pathway by first helping clients become comfortable with mobile banking features before introducing more advanced AI-powered planning tools. This staged approach allows clients to build technology confidence progressively. Figure 2 summarizes these recommendations into an actionable framework that advisers can use during client consultations.

Financial advisers should monitor clients for signs of technology overreliance that may be associated with weaker fundamental financial skills. Warning signs include clients who defer all financial decisions to apps, lose track of spending patterns despite using budgeting software, or become anxious when technology is unavailable. When these patterns emerge, practitioners should refocus on building core financial behaviors and limit technology recommendations until clients demonstrate solid foundational capabilities.

Limitations

This study is subject to several limitations. First, the single binary measure of AI interest likely oversimplifies complex attitudes involving trust, privacy concerns, and specific use preferences. Additionally, the NFCS groups race/ethnicity into only two categories (White versus Non-White), limiting our ability to explore how technology relates to outcomes in different racial and ethnic communities. Second, the NFCS lacked variables capturing mobile fintech engagement quality, usage contexts, or detailed technology attitudes beyond AI interest. Third, cross-sectional data limits causal interpretation, as temporal ordering between technology adoption and wellness outcomes cannot be established. Fourth, methodological improvements are essential, including development of multidimensional AI acceptance measures incorporating trust and privacy dimensions.

Future research should employ longitudinal designs to establish causal relationships and track how technology-capability interactions evolve over time. The complex interaction patterns observed warrant investigation into underlying mechanisms that may reflect automation bias, overconfidence, or substitution of AI advice for beneficial self-directed learning. Methodological improvements are essential, particularly refining measurement of AI attitudes beyond the single binary measure used here. Multidimensional scales capturing trust in AI, privacy concerns, perceived usefulness, and comfort with algorithmic decision-making would provide more nuanced understanding of how specific attitudinal components will change the patterns of technology benefits. Developing validated psychometric instruments for AI financial advice acceptance would strengthen both research and practice. Studies should routinely examine differential effects across demographic groups and investigate how factors such as financial stress, social support, and economic shocks might change these technology interactions. Research should also examine technology-capability interactions across specific racial and ethnic groups beyond binary classifications, as different communities may demonstrate distinct patterns in AI adoption, mobile technology use, and their combined effects on financial outcomes. Existing financial capability theories may require modification to account for technology-mediated pathways, particularly given the pronounced effects among lower-income populations. Primary data collection offering detailed technology usage patterns and user motivations would strengthen understanding of these complex relationships.

Summary

This study examined how AI interest and mobile fintech usage affect the relationship between financial capability and financial wellness using 2024 NFCS data. Results showed that financial capability remains the strongest predictor of financial wellness, but the benefits of technology use depend on client attitudes. Mobile fintech use was associated with weakened outcomes for AI-skeptical clients, but associations were stronger for AI-receptive clients. Most significantly, technology benefits concentrated among lower-income populations, suggesting that strategic technology deployment could help close financial outcome gaps. These findings provide financial advisers with the first systematic guidance on when client technology use enhances versus undermines the capability–wellness relationship, offering practical frameworks for technology-informed client counseling.

Citation

Gan, Lena, Karleah Harris, and Sara Kay. 2026. “Closing the Advice Gap: Technology Interactions in the Financial Capability–Wellness Relationship.” Journal of Financial Planning 39 (3): 70–82.

References

Addy, W. A., A. O. Ajayi-Nifise, B. G. Bello, S. T. Tula, O. Odeyemi, and T. Falaiye. 2024. “Transforming Financial Planning with AI-Driven Analysis: A Review and Application Insights.” World Journal of Advanced Engineering Technology and Sciences 11 (1): 240–57.

Aiken, Leona S., and Stephen G. West. 1991. Multiple Regression: Testing and Interpreting Interactions. Thousand Oaks, CA: Sage.

Anvari-Clark, Jannette, and Daniel Ansong. 2022. “Predicting Financial Well-Being Using the Financial Capability Perspective: The Roles of Financial Shocks, Income Volatility, Financial Products, and Savings Behaviors.” Journal of Family and Economic Issues 43 (4): 730–43. https://doi.org/10.1007/s10834-022-09849-w.

Brenner, Lorenz, and Tobias Meyll. 2020. “Robo-Advisors: A Substitute for Human Financial Advice?” Journal of Behavioral and Experimental Finance 25: 100275. https://doi.org/10.1016/j.jbef.2020.100275.

Carlin, Bruce I., Arna Olafsson, and Michaela Pagel. 2017. “Fintech Adoption across Generations: Financial Fitness in the Information Age.” NBER Working Paper No. 23798. National Bureau of Economic Research. https://doi.org/10.3386/w23798.

Consumer Financial Protection Bureau. 2023, June 6. “Chatbots in Consumer Finance.” www.consumerfinance.gov/data-research/research-reports/chatbots-in-consumer-finance/chatbots-in-consumer-finance/.

Cook, Judith A., Patrick J. Steigman, Jessica A. Jonikas, George Brice III, Shannon Johnson, Crystal Cortez, and Margaret Swarbrick. 2025. “Building Financial Wellness: Randomized Controlled Trial of a Financial Education and Support Intervention.” Psychiatric Services 76 (3): 256–62. https://pubmed.ncbi.nlm.nih.gov/39529498/.

Davis, Fred D. 1989. “Perceived Usefulness, Perceived Ease of Use, and User Acceptance of Information Technology.” MIS Quarterly 13 (3): 319–40. https://doi.org/10.2307/249008.

Demirgüç-Kunt, Asli, Leora Klapper, Dorothe Singer, Saniya Ansar, and Jake Hess. 2018. The Global Findex Database 2017: Measuring Financial Inclusion and the Fintech Revolution. Washington, DC: World Bank Publications.

Frost, Jon. 2020. “The Economic Forces Driving Fintech Adoption across Countries.” BIS Working Papers No. 838. Bank for International Settlements. https://doi.org/10.2139/ssrn.3515326.

Gerrans, Paul, Craig Speelman, and Guillermo Campitelli. 2014. “The Relationship between Personal Financial Wellness and Financial Wellbeing: A Structural Equation Modelling Approach.” Journal of Family and Economic Issues 35 (2): 145–60. https://doi.org/10.1007/s10834-013-9358-z.

Goddard, Kate, Abdul Roudsari, and Jeremy C. Wyatt. 2012. “Automation Bias: A Systematic Review of Frequency, Effect Mediators, and Mitigators.” Journal of the American Medical Informatics Association 19 (1): 121–27. https://doi.org/10.1136/amiajnl-2011-000089.

Gomber, Peter, Jascha-Alexander Koch, and Michael Siering. 2017. “Digital Finance and FinTech: Current Research and Future Research Directions.” Journal of Business Economics 87 (5): 537–80. https://doi.org/10.1007/s11573-017-0852-x.

Hayes, Andrew F. 2017. Introduction to Mediation, Moderation, and Conditional Process Analysis: A Regression-Based Approach. 2nd ed. New York: Guilford Press.

Huston, Sandra J. 2015. “Using a Financial Health Model to Provide Context for Financial Literacy Education Research: A Commentary.” Journal of Financial Counseling and Planning 26 (1): 102–4. https://doi.org/10.1891/1052-3073.26.1.102.

Joo, So-Hyun. 2008. “Personal Financial Wellness.” In Handbook of Consumer Finance Research. Edited by Jing Jian Xiao. New York: Springer: 21–33.

Jung, Dominik, Valentin Dorner, Markus Weinmann, and Hasan Pusmaz. 2018. “Designing a Robo-Advisor for Risk-Averse, Low-Budget Consumers.” Electronic Markets 28 (3): 367–80. https://doi.org/10.1007/s12525-018-0307-9.

Khan, Nasir Ullah, Fazal Zeb, Amjad Kamal, Naeem Azeem, and Atta Ullah Shah. 2025. “The Role of Socioeconomic Status in FinTech Adoption and Financial Access Examining the Mediating Effect of Socioeconomic Disparities.” Social Science Review Archives 3 (1): 1363–71. https://doi.org/10.70670/sra.v3i1.437.

Lown, Jean M. 2011. “Development and Validation of a Financial Self-Efficacy Scale.” Journal of Financial Counseling and Planning 22 (2): 54–63. https://files.eric.ed.gov/fulltext/EJ952966.pdf.

Lusardi, Annamaria, and Olivia S. Mitchell. 2014. “The Economic Importance of Financial Literacy: Theory and Evidence.” Journal of Economic Literature 52 (1): 5–44. https://doi.org/10.1257/jel.52.1.5.

Philippon, Thomas. 2016. “The Fintech Opportunity.” NBER Working Paper No. w22476. National Bureau of Economic Research. https://doi.org/10.3386/w22476.

Prawitz, Aimee D., and Jing Cohart. 2016. “Financial Management Competency, Financial Resources, Locus of Control, and Financial Wellness.” Journal of Financial Counseling and Planning 27 (2): 142–58. https://doi.org/10.1891/1052-3073.27.2.142.

Risko, Evan F., and Sam J. Gilbert. 2016. “Cognitive Offloading.” Trends in Cognitive Sciences 20 (9): 676–88. https://doi.org/10.1016/j.tics.2016.07.002.

Roy, Prasenjit, Biswajit Ghose, Premendra Kumar Singh, Pankaj Kumar Tyagi, and Asokan Vasudevan. 2025. “Artificial Intelligence and Finance: A Bibliometric Review on the Trends, Influences, and Research Directions.” F1000Research 14: 122. https://doi.org/10.12688/f1000research.160959.1.

Shaikh, Aijaz A., Richard Glavee-Geo, Heikki Karjaluoto, and Robert E. Hinson. 2023. “Mobile Money as a Driver of Digital Financial Inclusion.” Technological Forecasting and Social Change 186: 122158. https://doi.org/10.1016/j.techfore.2022.122158.

Tam, Chuong, and Tiago Oliveira. 2017. “Understanding Mobile Banking Individual Performance: The DeLone & McLean Model and the Moderating Effects of Individual Culture.” Internet Research 27 (3): 538–62. https://doi.org/10.1108/IntR-05-2016-0117.

Venkatesh, Viswanath, and Fred D. Davis. 2000. “A Theoretical Extension of the Technology Acceptance Model: Four Longitudinal Field Studies.” Management Science 46 (2): 186–204. https://doi.org/10.1287/mnsc.46.2.186.11926.

Xiao, Jing Jian, Jin Huang, Kaushal Goyal, and Sanjay Kumar. 2022. “Financial Capability: A Systematic Conceptual Review, Extension and Synthesis.” International Journal of Bank Marketing 40 (7): 1680–717. https://doi.org/10.1108/IJBM-05-2022-0185.

Xiao, Jing Jian, and Ki Tae Kim. 2022. “The Able Worry More? Debt Delinquency, Financial Capability, and Financial Stress.” Journal of Family and Economic Issues 43 (1): 138–52. https://doi.org/10.1007/s10834-021-09767-3.

Xiao, Jing Jian, and Nilton Porto. 2022. “Financial Capability and Wellbeing of Vulnerable Consumers.” Journal of Consumer Affairs 56 (2): 1004–18. https://doi.org/10.1111/joca.12418.