Journal of Financial Planning: April 2026

Tony Rich, ChFC, is a financial adviser and Missouri Air National Guard member. He is an independent adviser serving small businesses, individuals, and families, with a focus on practical planning, tax awareness, and aligning financial decisions with long-term goals. This article was developed as capstone research for his Master of Science in financial planning at the University of Missouri.

Abed G. Rabbani, Ph.D., CFP®, is an associate professor of personal financial planning at the University of Missouri. His research focuses on financial risk tolerance, financial knowledge, and financial wellness. He is a research fellow of the National Association of Insurance Commissioners (NAIC).

NOTE: Click the images below for PDF versions.

JOIN IN THE DISCUSSION: Discuss this article with fellow FPA Members through FPA's Knowledge Circles.

FEEDBACK: If you have any questions or comments on this article, please contact the editor HERE.

Financial planning has never been more sophisticated, yet many clients still experience it in pieces. Investment recommendations are made without full visibility into tax consequences. Tax returns are prepared without context for long-term planning decisions. Estate documents are drafted, then quietly ignored.

Clients do not experience these gaps as technical shortcomings. They experience them as confusion, missed opportunities, and avoidable stress. When professionals operate in silos, clients are left to connect the dots themselves, often without realizing that better coordination was even possible.

The most meaningful improvements in client outcomes rarely come from new products or more complex strategies. They come from a better application: aligning tax, investment, retirement, and estate decisions so that each reinforces the other. One of the most effective ways to deliver that alignment is through deeper collaboration between financial advisers and CPAs.

Despite the natural overlap in their work, adviser–CPA relationships are still commonly built around informal referrals rather than intentional service models. Lunch meetings and handshake agreements may create goodwill, but they rarely produce consistent coordination or measurable improvements in the client’s experience. Going beyond referrals is about moving from advice to application, ensuring recommendations are implemented with full awareness of their tax and planning consequences.

This article presents a practical framework for advisers who want to deepen client service through structured, compliant collaboration with CPAs, without sacrificing independence or creating unnecessary complexity. Understanding why informal adviser–CPA relationships fail is the first step toward designing more durable collaboration models.

Why Informal Adviser–CPA Relationships Break Down

Most adviser–CPA relationships stall for reasons unrelated to competence. They break down because the relationship itself lacks structure. Industry benchmarking suggests multidisciplinary partnerships are becoming more common as firms seek to deliver more comprehensive client service (Charles Schwab & Co. 2023), yet many adviser–CPA relationships still rely on informal referrals that break down under the pressures of tax season and day-to-day practice demands. Prior research suggests informal professional referral arrangements often fail to produce sustained collaboration or accountability (Grierson 2015).

Several friction points show up repeatedly:

- Misaligned incentives. When compensation or recognition occurs only at the moment of referral, there is little reason for continued engagement.

- No shared workflow. Without a cadence for communication, collaboration becomes reactive rather than proactive.

- Unclear expectations. Each professional assumes the other is “handling it,” leaving gaps in responsibility.

- Seasonality pressure. CPA capacity is concentrated during tax season, precisely when coordination matters most.

- Compliance uncertainty. Even good intentions can create risk if compensation and information sharing are not clearly documented and disclosed.

Another subtle challenge is professional identity. Advisers and CPAs are trained to “own” distinct domains, which can unintentionally discourage collaboration. Advisers may hesitate to involve CPAs early, while CPAs may avoid proactive planning that falls outside traditional tax compliance. Without an explicit collaboration model, both default to staying in their lanes, reinforcing silos over time.

The result is a relationship that feels friendly but is fragile, and a client experience that remains fragmented. Structured collaboration does not eliminate professional boundaries; it defines them. By clarifying when and how coordination occurs, advisers and CPAs can protect their respective roles while still delivering a more cohesive client experience. Addressing these breakdowns requires more than better intentions; it requires selecting a collaboration structure that fits the practice and the client.

Four Models of Adviser–CPA Collaboration

Adviser–CPA collaboration exists on a spectrum, from low integration to deep operational alignment (table 1). Not every practice needs or should pursue full integration. Many successful partnerships evolve deliberately over time as trust builds, workflows mature, and client needs become more complex.

Rather than viewing these models as “good” or “bad,” it is more helpful to think in terms of fit. Each model balances flexibility, accountability, and client impact differently. The right choice depends on your practice stage, service philosophy, and tolerance for operational and compliance complexity.

Model 1: One-Time Referral Fee

Low Integration—“Handshake”

This is the most familiar structure in the profession. A CPA introduces a client, and the adviser provides a one-time payment once the client engages. The relationship is often informal and transactional.

Revenue structure. Event-driven. Compensation occurs once, typically tied to onboarding or first-year revenue.

How this shows up in practice. Day-to-day operations change very little. Communication is episodic, often limited to a brief handoff. Although each professional continues operating independently, and coordination is incidental rather than expected, there is still an opportunity for meaningful role-sharing that benefits the client. The CPA may provide tax-efficient insights to guide the adviser’s recommendations, while the adviser’s planning framework may highlight future tax considerations for the CPA to monitor.

What the client sees. Separate meetings, repeated explanations, and responsibility for relaying information between the adviser and CPA.

Where it works. This model works well when flexibility is the priority, particularly for early-stage advisers testing professional chemistry without long-term commitment. It allows advisers to partner with many CPAs simultaneously without exclusivity or dependency.

Where it breaks (slowly). The weakness is quiet erosion. Once the referral payment is made, the CPA’s incentive to remain engaged diminishes. Coordination fades, and clients assume collaboration that is no longer occurring. Planning decisions remain disconnected, offering little improvement in the application of advice.

Model 2: Ongoing Revenue Share

Moderate Integration—“Contract”

In this model, compensation is tied to the longevity of the client relationship rather than a single transaction. When properly documented and disclosed, an ongoing revenue share creates a structural reason for continued engagement and shared accountability.

Some partnerships enhance this model by offering a visible client benefit, such as the adviser covering the cost of the client’s tax return. When implemented thoughtfully and compliantly, this reframes the relationship around service quality rather than referral volume.

Revenue structure. Firm-to-firm, contractual, and recurring.

How this shows up in practice. This structure naturally supports deeper role-sharing between the CPA and adviser. Behaviors begin to change. Advisers are more likely to involve CPAs earlier in planning decisions. CPAs have a reason to flag tax opportunities proactively rather than reactively. Communication becomes more predictable and less dependent on “catching up during tax season.” Because both professionals benefit from the durability of the client relationship, they are incentivized to coordinate regularly, share data, align tax strategies with investment decisions, and ensure that planning actions remain tax‑efficient over time. Rather than operating in parallel, the CPA and adviser function as collaborative partners whose combined expertise helps maintain a consistent, high‑quality advisory experience throughout the client’s financial life.

What the client sees. More consistent messaging, fewer follow-up meetings, and less need to coordinate details across professionals.

Where it works. This model often fits growth-stage firms best. It introduces structure while preserving independence and allows advisers to collaborate with multiple CPAs. When executed well, it improves continuity of care without requiring full operational integration.

Where it breaks (slowly). Misalignment of expectations is the most common failure. If one party expects deep planning collaboration while the other expects passive referrals, frustration builds. Without a shared cadence or consistent client messaging, the relationship can regress toward transactional behavior despite ongoing compensation.

Model 3: Licensing Integration (CPA as IAR)

High Integration—“Teammates”

Licensing integration represents a meaningful shift. In this model, the CPA becomes appropriately registered (for example, as an investment adviser representative under the adviser’s RIA) and participates directly in advisory activities. The relationship moves from coordination to collaboration under a shared fiduciary framework.

Revenue structure. Joint client codes or direct compensation splits through the RIA, subject to supervisory and regulatory requirements.

How this shows up in practice. In a licensing integration model where the CPA becomes an investment adviser representative, role‑sharing becomes more seamless and interdependent. Client meetings change. Advisers and CPAs sit on the same side of the table. This shared registration structure allows both professionals to collaborate directly on planning recommendations. Planning decisions are evaluated through both tax and investment lenses simultaneously. Clients experience a unified team rather than adjacent professionals. The result is an integrated advisory experience in which the CPA’s tax expertise and the adviser’s planning and investment oversight function as complementary parts of a cohesive service model.

What the client sees. Joint or integrated meetings where tax and planning decisions are addressed together with minimal repetition.

Where it works. This model is best suited for long-standing relationships with strong cultural alignment and a shared client base with meaningful complexity, such as business owners, retirees, or families with ongoing tax-sensitive planning needs.

Where it breaks (slowly). Licensing integration introduces gravity. Supervisory obligations increase. Documentation expectations rise. Without clear role definitions, responsibilities can blur, creating confusion for clients and compliance risk for the firm. Advisers must be prepared to supervise; CPAs must be willing to operate within a fiduciary environment that may feel unfamiliar at first.

Model 4: Joint Venture or Shared Ownership

Very High Integration—“Partners”

At the far end of the spectrum is shared ownership or a formal joint venture. Advisers and CPAs share equity in a unified entity, embedding collaboration into governance, culture, and long-term strategy. Rather than coordinating across firms, both professionals build systems together—sharing expenses, revenue, and accountability—to create a single organization centered on client service.

Revenue structure. Shared enterprise economics, such as profits, expenses, and long-term enterprise value.

How this shows up in practice. Client service is fully integrated. Both professionals share governance responsibilities and financial outcomes, they codevelop integrated client processes, coordinate planning and tax strategies from the outset, and participate jointly in key client decisions. Technology, staffing, and workflows are aligned around delivering coordinated advice. Clients experience a cohesive planning team rather than two separate professionals. The CPA and financial adviser are no longer collaborating across firm boundaries; they are cocreating service models, workflows, and strategic priorities within the same enterprise.

What the client sees. Fewer, more comprehensive meetings and coordinated decisions that require little to no client-managed follow-up.

Where it works. This model offers the strongest alignment of incentives and the most durable collaboration. It is best suited for principals committed to building a long-term enterprise together, with shared vision and compatible service standards.

Where it breaks (slowly). Joint ventures magnify everything, good and bad. Without clearly defined decision rights, valuation methods, and exit provisions, disagreements can become expensive and emotionally charged. Cultural misalignment or mismatched expectations around workload, growth, or risk tolerance can strain even well-intentioned partnerships.

Importantly, these models are not static. Many successful adviser–CPA relationships move intentionally along this spectrum over time. What begins as a handshake arrangement may evolve into a contractual revenue share as trust builds and shared clients increase. In some cases, years of effective collaboration naturally lead to licensing integration or even shared ownership.

Progression should be deliberate, not automatic. Each step increases coordination but also introduces additional operational and compliance responsibilities. Advisers should view movement along the spectrum as a business decision, not a reward for longevity. The guiding question is not whether deeper integration is possible, but whether it meaningfully improves client outcomes and can be supported sustainably.

Choosing the Right Model for Your Practice Stage

A common mistake is assuming deeper integration is always better. In reality, the right model depends on where your practice is today and where you want it to go.

- Early-stage advisers often benefit from low-commitment arrangements that allow flexibility and experimentation.

- Growth-stage firms frequently find contractual revenue-sharing models provide the best balance of structure and independence.

- Mature practices may pursue deeper integration as client complexity, enterprise value, and succession planning become central concerns.

Across all stages, success depends less on structure and more on clarity, clear expectations, clear disclosure, and clear communication.

What Clients Gain from Structured Collaboration

Clients rarely care how professionals are compensated or organized. They care about outcomes, ease, depth of care, and total cost. Prior industry analysis suggests that deeper integration between tax and planning services can improve client engagement and retention (Freeman 2020).

Better tax-aware decisions throughout the year. Tax strategy is not a once-a-year event. Roth conversions, charitable giving, capital gains realization, retirement distributions, and business planning decisions all benefit from timing and coordination. When advisers and CPAs communicate before decisions are finalized, clients avoid irreversible mistakes and capture opportunities that would otherwise be missed (Mills et al. 1998).

Fewer surprises at filing time. Many tax-season issues stem from missing context, not complex tax law. A simple mid-year alignment on income, realized gains, and deductions can prevent last-minute scrambling and unexpected liabilities.

A more confident client experience. Clients do not want to serve as messengers between professionals. When advisers and CPAs share a consistent narrative, what happened, why it happened, and what comes next, clients feel supported rather than reactive.

A simple example illustrates the difference: a client plans a Roth conversion after a strong market year. When the adviser and CPA coordinate, the conversion amount is adjusted to stay within a target bracket, withholding is aligned, and underpayment penalties are avoided. The strategy itself is not exotic. Coordination is what makes it effective. Table 2 summarizes the primary benefits of structured adviser–CPA collaboration across key stakeholders.

Making Collaboration Work Without Creating Compliance Risk

Delivering these benefits consistently requires more than good coordination; it requires clear guardrails around compensation, communication, and data sharing. Effective collaboration does not require elaborate technology or complicated agreements, but it does require discipline. Compensation arrangements must be documented and disclosed, client authorization is essential when sharing tax return information, and roles must be clearly defined so collaboration enhances accountability rather than blurring it.

A practical starting point includes:

- A written agreement reviewed through appropriate compliance channels

- Plain-language client disclosures explaining the relationship and any related compensation

- Explicit client consent for information sharing

- A simple annual workflow defining who sends what and when

Advisers should also be thoughtful about how collaboration is explained to clients. Transparency builds trust, but oversharing operational details can create confusion. Clients primarily need to understand how professionals coordinate and what that coordination means for their plan. For example, an adviser may explain, “We coordinate directly with your CPA to share relevant planning and tax information, so your financial decisions are implemented efficiently. In some cases, our firm compensates the CPA for their time spent collaborating on your planning. Each professional remains responsible for their own work, and all coordination is intended to support your overall plan.”

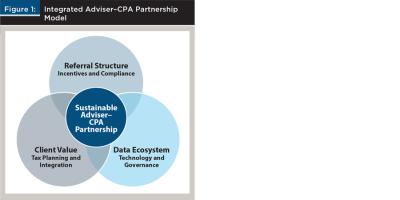

When collaboration is positioned consistently, as a way to reduce surprises and improve execution, clients are more likely to view it as a natural extension of good planning rather than an unusual arrangement. Figure 1 illustrates how sustainable adviser–CPA partnerships depend on the alignment of client value, referral structure, and data governance.

A 12-Month Implementation Roadmap

Advisers looking to move beyond referrals should start small and build momentum through a pilot program and an integrated model (figure 1).

Months 0–3: Identify the Right CPA Partners

Select three to five CPAs who already serve your ideal clients. Screen for culture, responsiveness, and willingness to collaborate. The best partnerships are built on compatible standards, not prestige.

Months 3–6: Pilot with One to Three Shared Clients

Establish two touchpoints: a pre-tax-season planning conversation and a post-filing debrief. Keep the workflow simple and consistent. Measure outcomes like reduced friction, fewer surprises, and clearer client communication.

Months 6–12: Systematize, Refine, and Decide

Document what worked. Refine the cadence. Decide whether to expand, maintain, or discontinue the arrangement. Progress should be measured not by referral volume, but by improved client experience and more coordinated execution.

Conclusion: From Transactions to Stewardship

Moving beyond referrals is not about growth for growth’s sake. It is about moving from advice to application—ensuring recommendations are implemented with full awareness of their tax and planning consequences.

When advisers and CPAs collaborate intentionally, clients experience fewer surprises, better outcomes, and greater confidence. Professionals benefit as well, but as a byproduct of improved service rather than its objective.

The future of financial planning belongs to firms that reduce friction and deliver coordination without sacrificing accountability. Adviser–CPA collaboration, when built on clarity and stewardship rather than transactions, is one of the most natural ways to do exactly that.

References

Charles Schwab & Co. 2023. Schwab RIA Benchmarking Study: The Rise of Multidisciplinary Partnerships in Wealth Management. Schwab Advisor Services. https://advisorservices.schwab.com/insights-hub/benchmarking.

Freeman, Debbie. 2020, August 3. “Offering InHouse Tax Preparation to Supplement Revenue and Enhance Client Retention.” Kitces.com. www.kitces.com/blog/debbie-freeman-peak-financial-advisors-tax-preparation-client-retention-rates/.

Grierson, A. J. C. 2015. “The Role of Referrals in New Client Capture within the Field of Independent Financial Advice.” Doctoral dissertation, University of Hertfordshire. University of Hertfordshire Research Archive. https://uhra.herts.ac.uk/id/eprint/16224/.

Mills, Lillian F., Merle M. Erickson, and Edward L. Maydew. 1998. “Investments in Tax Planning.” Journal of the American Taxation Association 20 (1): 1–20.